Online retail sales growth slowed in May following a fairly strong April

Insight

And signs that the European economy might be levelling off rather than falling.

https://soundcloud.com/user-291029717/goodbye-to-a-no-deal-brexit-ever

The UK parliament has just voted – by 4 votes – to support the so-called Speldman amendment which rejects a ‘no deal’ Brexit in clearer terms than the Prime Minister’s own motion. Yet the Prime Minister’s own motion rejecting leaving without a deal has also passed (by 321 to 278). While in reality the passage of neither of these bills can definitely eliminate the risk of a so-called ‘hard Brexit’ (after all, any alternative will still require EU approval) it has further reduced the chances of it. Hence Sterling, which recouped its Tuesday night losses in anticipation of the Prime Minister’s motion not to leave the EU without a deal, has rallied further on the passage of these motions. .

The bigger test for Sterling comes not with today’s votes in parliament but tomorrow and thereafter, in particular once we see what type of extension to Article 50 parliament opts to support and which will then require sanction from the EU Council who hold a Summit next week. So Sterling is set to stay stuck in the washing machine for a while longer. Indeed, it is still not possibly to rule out the risk that we end up with a snap General Election, an event risk which were it to transpire has the potential to hurt Sterling by even more than the prospect of an imminent UK exit from the EU without any transition arrangement.

It is also not inconceivable that in the wake of the EU Summit, Theresa May decides to come back to parliament for a third time with her Withdrawal Agreement, given the increased prospect of ‘no Brexit’ following a possible 2nd referendum might at least galvanise the whole of the ERG band of Tory Brexiters and also some other ‘leavers’, to back her deal. GBP-positive were that to be the case – albeit pretty unlikely (e.g. it’s still hard to see the DUP supporting this without further concession on the Irish backstop from the EU and where it was the UK Attorney General’s advice on the changes announced by Theresa May on Monday night that scuppered the second attempt to get her Withdrawal Agreement approved).

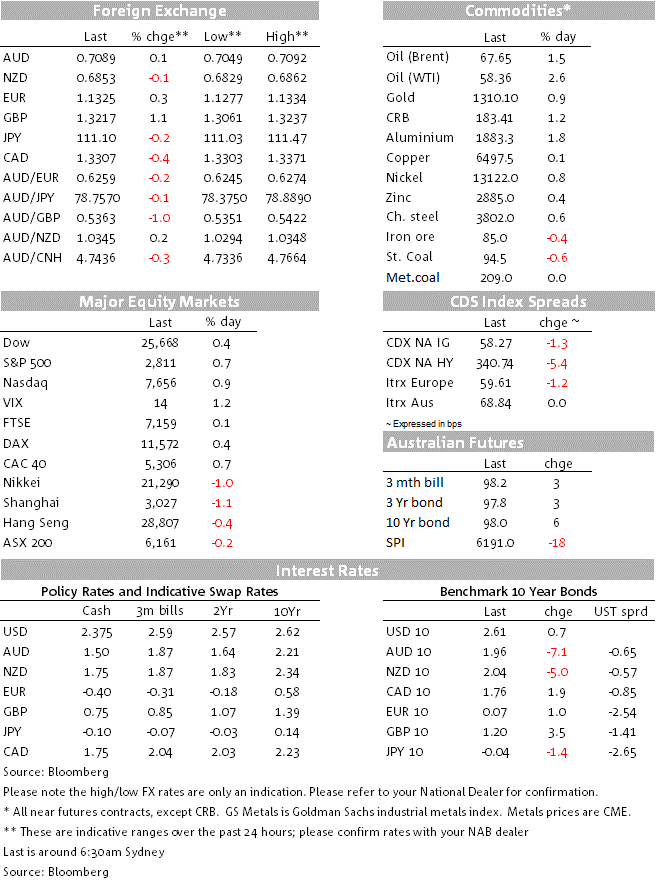

Ongoing UK political shenanigans have, as one market commentator has suggested, tended to suck the oxygen out of broader financial markets this week. This though hasn’t stopped US stock markets from more than recouping last week’s losses such that the S&P 500 has on an intra-day basis reached its highest level since October 10th last year, when we were just 5 days into the big Q4 sell-off. Amazon has been one of the counters leading the rally, up over 1%, through gains are fairly broad-based across sector. The further travails of Boeing – after president Trump ordered the grounding of all 737 Max planes in America against the advice of the FAA, has meant that the Dow (+0.6%) continues to underperform the S&P and NASDAQ (both ending +0.7%)

This risk-positive backdrop has meant that the US dollar has been under downward pressure even beyond the direct influence on USD indices from the big gains for Sterling – and which has in characteristic fashion also lent some support to the Euro. AUD for example is coming into the end of the New York day with small gains, so fully recouping the hit it suffered following yesterday’s poor Westpac Consumer Confidence survey readings.

The US data highlight was durable goods orders, which modestly exceed expectations in both headline (+0.4%) and core terms (+0.8% ex-defence and ex-aircraft) but which failed to provide much of a lift to either US bonds yields or the USD. 10 year Treasuries are 0.7bps higher at 2.61% and the 30-year bond +1.6bps at 3.01%, latter not helped by a fairly poorly received 30-year auction. US final demand PPI came in 1/10% less than expected in core terms (so yr/yr down to 2.5% from 2.6%) but with CPI data already released had no impact.

Trade news includes President Trump saying he’s in no rush to complete a China trade deal and that it doesn’t matter whether a deal is made before or after a Summit with President Xi. He has though re-iterated that there a ‘very good chance’ a deal will be made.

Meanwhile EU Trade Commissioner Cecilia Malmstrom has sounds an upbeat note about the prospect of receiving the green light from EU governments to start negotiations with the U.S. on cutting industrial tariffs. She adds though that the EU has no intention of making agriculture part of the market-opening talks with the U.S., where some officials have demanded that farm goods be included

AU: Westpac consumer confidence, Mar: 98.8 vs. 103.8 prev.

EC: Industrial production, Jan: 1.4 vs. 1 exp.

US: PPI (y/y%), Feb: 1.9 vs. 1.9 exp.

US: PPI ex food and energy (y/y%), Feb: 2.5 vs. 2.6 exp.

US: Durable goods orders (m/m%), Jan: 0.4 vs. -0.4 exp.

US: Capital goods orders – non-defence ex air (m/m%), Jan: 0.8 vs. 0.2 exp.

China activity readings for February (13:00 AEDT). Industrial production expected 5.6% YTD Y/Y from 6.2%; Retail Sales expected 8.2% from 9.0%; FAI 6.1% from 5.9%

Final German, French CPI; US New Home sales, weekly jobless claims, import and export prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.