Total spending grew 0.9% in June.

Powell then also noted how the strength in the labour market underscores why the Fed thinks it could take time to bring inflation down.

JN: Labour cash earnings (y/y%), Dec: 4.8 vs. 2.5 exp.

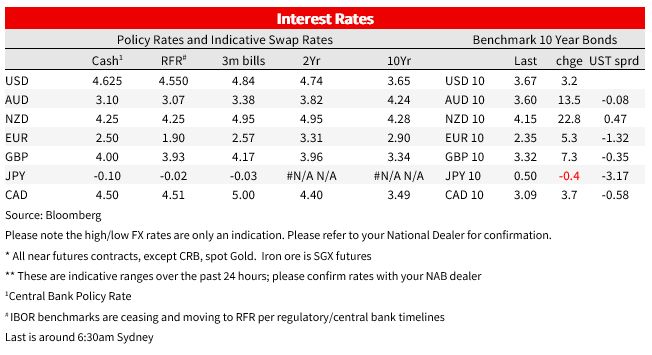

AU: RBA Cash Rate target (%), Feb: 3.35 vs. 3.35 exp.

GE: Industrial production (m/m%), Dec: -3.1 vs. -0.8 exp.

US: Trade balance ($b), Dec: -67.4 vs. -68.5 exp.

“What’s there to be happy about? The job’s not finished. Is the job finished? Kobe Bryant

It has been an overnight session of two halves. A quiet range trading initial half before Fed Chair Powell’s interview followed by some fireworks once he began speaking. At the start of the interview, Powell sounded dovish triggering a jump in equities and a decline in the USD and UST yields. However, Powell’s final remarks were more hawkish, noting that if strong labour data persists, the peak rate in the current tightening cycle may be higher. After an up and down trading pattern, US equities are heading into the close with modest gains led by tech stocks, the UST curve has a steeping bias, and the USD is a tad weaker across the board. JPY and AUD are the G10 outperformers.

In a candid and relax interview before the Economic Club of Washington, Fed Chair Powell initially triggered a jump in US equities sounding less hawkish as he noted how the disinflationary process had already begun, adding it still has a long way to go, particularly within the services sector. Later on, however, when asked about the labour markets, Powell noted that if the job situation remains very hot, “it may well be the case that we have to do more,”. The comments triggered a reversal on the initial move up in equities and move down in yields.

Powell then also noted how the strength in the labour market underscores why the Fed thinks it could take time to bring inflation down. The process of bringing inflation down to the 2% target is likely to take some time, it is likely to be bumpy and is not going to be smooth. In contrast to market pricing that sees rate cut from the second half of the year, Powell then remarked that “we think we’re going to have to do further [rate] increases, and we think we’ll have to hold policy at a restrictive level for some time.”

As we head into the NY close, after an up and down reaction to Powell’s comments, US equities are trading in the green with tech stocks leading the gains. The NASDAQ is up 1.48% as I type while the S&P 500 is 0.48%. The price action seems to suggest equity investors were bracing for a more hawkish message, but in the end, Powell essentially reiterated his post FOMC message from last week.

Earlier in the session, Minneapolis Fed President Kashkari said January’s strong labor-market report shows the US central bank would need to keep raising rates. “Right now I’m still at around 5.4%,” he told CNBC Tuesday. 5.4% is essentially the 5.25-5.50% band which is one extra hike above the FOMC median while the market currently prices a peak at 5.15%. Kashkari then added “no one should overreact to one (labour market) report…but the underlying strength of the services sector of the economy is still very robust and that’s where I think a lot of us are focusing our attention”. Speaking soon after NY close yesterday, Fed’s Bostic said the jobs data raises the possibility of a higher peak rate, but that his base case is still for two more hikes (so as per the median Fed 2023 dot).

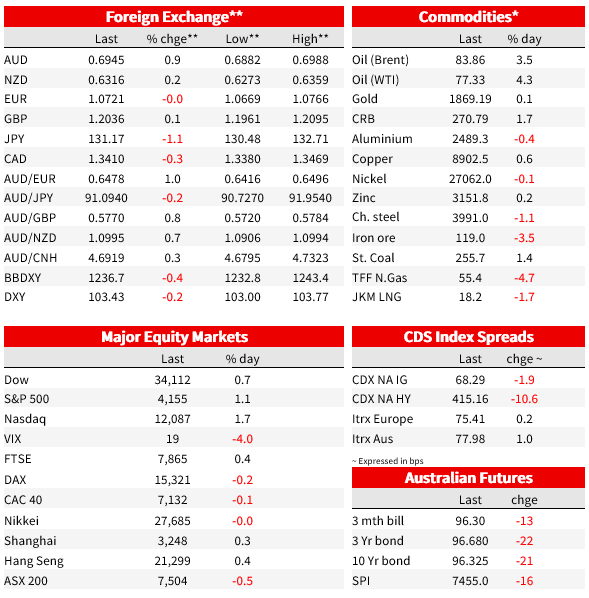

Post Powell’s speech, the UST curve has ended the day with a mild steeping bias, the 2y rate is 0.5bps lower relative to yesterday levels at 4.47% while the 10y rate is about 2bps higher now trading at 3.67%. Australian 10y futures are up 13.5bps over the past 24 hours, but the move largely reflect the RBA hike and hawkish message in the statement.

Yesterday, the RBA raised rates by 25bps to 3.35%, the nineth consecutive increase. The Statement was hawkish with the RBA Board expecting “…further increases in interest rates will be needed over the months ahead…”. The ‘plural’ in this wording suggests the RBA sees at least two more 25bp hikes over the months ahead, likely locking in a March rate hike, and then possibly another in April or May. Key data to watch before the next RBA meeting is WPI wages on 22 February and the National Accounts on 1 March.

Looking at the intraday chart USD indices are a tad lower relative to yesterday’s Sydney’s closing levels. DXY is down 0.1% over the past 24hours while BBDXY is -0.35%. The initially reaction to Powell’s commented weighed on the USD, but much of that move has now been reversed.

Within G10, JPY +1.12% and AUD +0.83 % are the notable outperformers. USD.JPY now trades at ¥131.25, down from yesterday’s high of ¥132.84. Yesterday JPY showed little reaction to the higher than expected Japan wages data, but may be after some processing markets have digested its significance. Japan wage data were much stronger than expected, up 4.8% y/y in January, boosted by winter bonuses. Multi-decade highs for inflation measures have become the norm for Japan, but the market was reluctant to read too much into the figures, with ex-bonus wage inflation at 1.9%, below the 3% mark the BoJ would be more comfortable with. In real terms wages ticked up to just 0.1% yoy, the first positive reading since March last year. Overall is good news for the labour market and a step in the right direction for the BoJ.

The AUD’s now trades at 0.6945 with the past 24 hours gains largely attributed to the RBA hike and its hawkish message. The Fed may have more work to do to bring inflation down, but the RBA still has a bigger job. RBA forecasts which are conditioned on a market/economist interest rate path of a peak of around 3.60%, reinforced the hawkish messaging. Inflation is only expected to decline to 4¾% over 2023, and be around 3% by mid-2025.

In economic news, the US trade deficit was slightly smaller than expected in -$67.4b in December, after the advanced reading for the goods side, but the annual deficit for 2022 still widened to a record $948b. And with US CPI high on the watchlist for investors, it is notable that Manheim reported that used vehicle prices rose for the second consecutive month in January, up 2.5% m/m, with price increases that were “not typical”.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.