Talks with the DUP offered some hope over the weekend of support for a Brexit deal but it’s yet to be brokered with Thursday’s EU Summit looming

Hammond says another deal won’t be put to the Commons unless there’s indicated support

US market now eyeing off a soft growth and policy tilt from the FOMC later in the week

US-China trade deal some weeks away; North Korean leader reverts to the use of inflammatory language, speaking of a “gangster-like” US

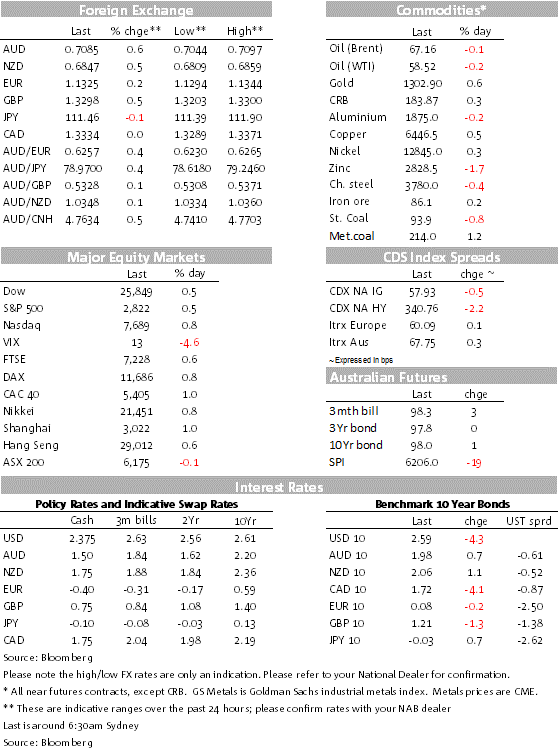

AUD ends the week at 0.7089 as stocks make some further gains

Weekend Sydney/Melbourne auction results suggesting Sydney and Melbourne clearances in the 50s with volumes well down on year earlier levels

Week ahead: Initially Brexit news flow, RBA Minutes tomorrow and two RBA speeches (not Lowe); NZ GDP, FOMC, AU employment all Thursday; EZ PMIs Friday

Local calendar quiet today

The market closed the week with equities closing out a good week, bonds though also gaining. The AUD closed the week close to 0.71, having tested 0.70 earlier in the week, seemingly with a soft edge that was worked off in the second part of the week. It’s been trading close to that level in early trade this morning. The Dow, S&P 500, and the Nasdaq closing between 0.4-0.8% higher, all capping off a good week, the Nasdaq faring the best up just under 4% for the week. The US 10 year Treasury ended down 4.3bps to 2.5871%, the lowest since early year volatility.

Sterling made some gains at the end of the week as UK Chancellor Hammond and leaders of the DUP held talks, Sterling closing 0.45% higher at 1.3299.

Mixed US data: still bruised manufacturing, but consumers feeling some relief

A limited flow of data Friday was mostly US-centric on Friday and it was mixed report on the US economy. For those looking for trade impacts, Industrial production in February underwhelmed with barely visible growth of 0.1% growth after January’s 0.4% decline (revised up from -0.6%). The NY Fed’s Manufacturing report for March was softer than expected at 3.7, down from 8.8, a consensus forecast of 10.0 and back to levels again not seen since mid-2017.

On the other side of the ledger, the preliminary March UoM Consumer Sentiment index printed at 97.8, above last month’s 93.8 and an expected 95.3. The January JOLTS Job Openings labour turnover report (the underbelly of the labour market) showed a step up in new jobs to 7.581m from 7.335m and the near flat 7.31m expectation, a strong suggestion of no slowing in labour demand in the early part of the year. (It of course precedes the Feb near flat payrolls number.)

While not absolute top tier readings, it’s a mixed story, hints that trade war issues may be continuing to blow back against US trade-exposed sectors. The market is very alert to the expectation of a soft US GDP Q1, affected by the government shutdown, the Atlanta Fed’s GDPNow currently estimated at 0.4% and the NY Fed’s Nowcast estimate at 1.4%.

All eyes ahead now to the FOMC Thursday morning our time with only the NAHB Housing Index and the Feb Durable Goods Orders report between now and then.

Brexit: No certainty of a third vote ahead of EU Summit Thursday

As the clock ticks and as the Brexit train wreck continues to unfold, it seems that further talks between the Government and their Northern Ireland coalition members might have been getting closer to a “deal” over the weekend, but they are not there yet. Speaking on the BBC overnight, UK Chancellor Hammond has been saying that the Government won’t bring a third vote to the Commons unless they think they have sufficient votes, getting that support is still a “work in progress”, according to Hammond. He thinks they are close to resolving the challenging Brexit situation.

Even if they get such a third vote passed on a Withdrawal Agreement, PM May will the ask for the EU for a short extension to get everything in place. If it doesn’t pass, there is already talk of a fourth vote, but the PM will have to ask the EU for a longer extension. Just how long the extension would be will then be decided by an EU meeting on March 21.

The market waits and watches and continues to price against the prospect of a crash out Brexit deal, believing that Parliament will take control before that happens. Hopes, however forlorn, of a last minute deal, might be enough for May to convince her European negotiators to at least seek a short term extension. Frankly, how long will it be before Parliament takes control? Another referendum? An election?

US-Sino trade deal (at least) weeks away

On the US-China trade front, a press report out of China pointed to substantial progress as having been made, following news earlier in the week that the two Presidents now not meeting in late March that was earlier being touted as a big event “signing ceremony”. In addition, news from the main players among the US trade negotiators team suggested that much more work needs to be done.

While there is presumably a strong US political imperative to get a deal done ahead of next year’s elections, and presumably China is keen to bed down this issue, and while we expect a deal to be proclaimed, we can only believe it once it’s seen.

It’s also becoming clearer again that that North Korea’s de-nuclearisation seems way off and certainly not near the initial post-Trump/Kim meeting hopes.

Local Auction Clearance Rates for this weekend show the preliminary Sydney rate at 63.1% – likely mid-higher 50s by Thursday’s update – and Melbourne’s at 53.7%, likely around if not below 50% when the Thursday update is out.

Coming up this week

Today is quiet start to the calendar wise with only the NZ PSI Services index and Japanese trade figures;

Locally the focus this week will be tomorrow’s RBA Minutes and two speeches from RBA officials, the second (Wednesday) from Michele Bullock speaking in Perth to the property industry

It’s a big Thursday with the FOMC first up, NZ GDP and then the AU Labour Force report for February;

For the FOMC, no change in the Fed funds expected by all 90 in the Bloomberg survey. The focus will be on the new set of Fed forecasts, likely revisions to their own forecasts of the Fed funds rate (downward, taking out one or both of the hikes expected last December), revisions to growth, inflation, and unemployment, estimates of the neutral Fed funds rate and more clarification on winding down the balance sheet. NAB expects no further rate hikes this year;

The shadow FOMC (a world-wide poll of 117 analysts) expects the dot plot distribution to be lowered to one hike this year from the two expected in December. 60% expect the Fed to announce details of a plan to stop its balance sheet reduction;

After the FOMC comes NZ’s December quarter GDP, NAB looking for growth to ease back to 2.4% from 2.6%; the median is at 2.5%;

Then it’s onward to the February AU Labour Force report, when NAB looks for no employment growth after last month’s 39.1K gain, hinted at by creeping softness in leading indicators of labour demand and a headwind to the official number this month from the exit of a sample rotation group with a high employment/population ratio. That factor also points to the risk of 5.1% unemployment rate print, rather than the market’s pick of an unchanged 5.0%; and

Also this week, the BoE meets and while no change is as close to a certainty as you can get.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.