As concerns over Italy subside, for now, President Trump has upped the ante against the EU, Mexico and Canada, with tariffs from midnight on steel and aluminium.

Italy forms government; no immediate risk of pushing to exit Euro or leave EU; new Finance Minister proposed by League/Five Star Coalition

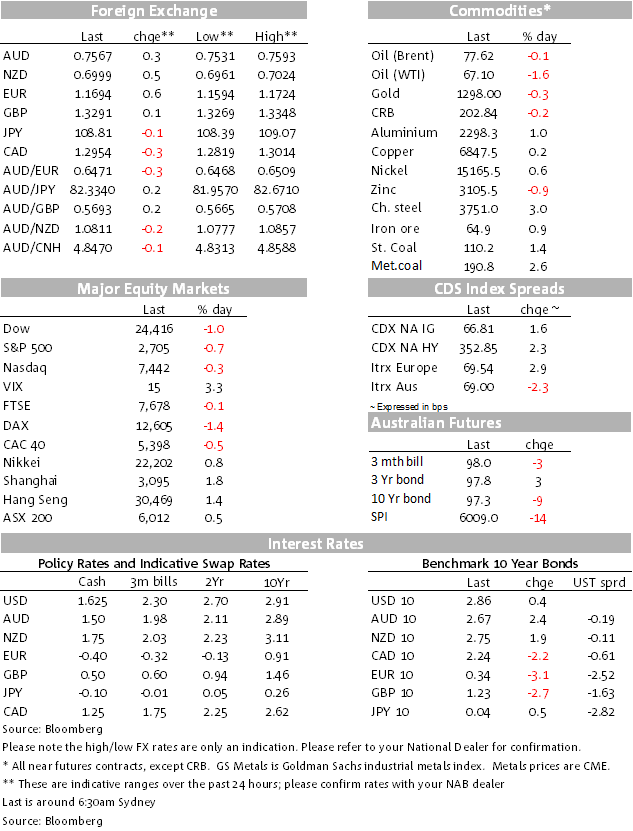

US Commerce Secretary Ross announces steel, aluminium tariffs back on for EU, Mexico and Canada

CAD largest loser overnight among majors; markets generally in somewhat defensive mood

US consumer spending better than expected in April; PCE core deflator not breaking away from moderate inflation mould; payrolls tonight

A new Italian coalition government between the Five Star and the League is now done, Prime Minister designate Conte proposing and announcing an alternative (less immediately contentious) candidate for Finance Minister, Giovanni Tria, head of the Economy Faculty at Rome’s Tor Vergata University. Tria’s previously stated views have called for a debate on the Euro in Italy and in the wider EU.

Both parties are intimating that there are no plans to leave the Euro or exit the EU, calming market nerves at least for now, and markets taking a positive read through from pro-Euro Italian polls released overnight. Italian yields pulled back further on all this news. Euro-exiting news has faded, at least for now, backed up by these pro-Euro polls. The two polls were taken on Wednesday night showing Italians overwhelmingly favour staying in the euro, the Piepoli poll showing 72% want to stay in the Euro (23% to leave) and a Euromedia poll showing 60% want to stay, 24% to leave. Note also that Euro-sceptic Savona is to be in the Cabinet as a minister for European Affairs. The market will need to keep an eye on the path ahead still with a fiscal expansion planned to address Italy’s economic under-performance.

The US data flow might have been a better tonic for the tone of investment markets (as developments in Italy have been) had it not been for trade tensions resurfacing. US Commerce Secretary Wilbur Ross announced that the 25% steel and 10% aluminium tariffs on the EU, Mexico and Canada would re-apply from July 1, today. Ross blamed not enough progress in dealing with the EU on trade issues and a lack of progress in re-writing NAFTA. Both the CAD and the MXN weakened on the news, US bonds yields are ever so marginally higher while US equities are in negative territory again after yesterday’s recovery.

While playing to their political constituency, this announcement drew some strong negative responses from within the Republican Party, Senate Finance Committee Orrin Hatch calling it a tax on Americans, another Republican drawing protectionism parallels with the Great Depression. The EU, Canada, and Mexico all responded strongly, the EU for example saying they could target products including Harley-Davidson and Levis.

The US data points were generally growth-friendly without letting the inflation genie out of the bottle. The April personal income and spending report revealed real consumer spending growth of 0.4% in the month after 0.5% in March, the Atlanta Fed upping its concurrent estimate of GDPNow to a meaty 4.7% for Q2, a nice rebound after this week’s downward revision to Q1 back to 2.2% from 2.3%. The core PCE deflator rose a rounded 0.2% in April, the rounded estimate ahead of the 0.1% expected, though it was a low 0.2% at 0.157% and essentially unchanged from the 0.155% for March, annual growth in line with expectations at 1.8%. EC core CPI though did pop surprisingly higher, up to 1.1% in May from 0.7% according to last night’s preliminary print, above the higher 1.0% tipped. Elsewhere on the activity side in the US, weekly jobless claims remained super low at 221K in the last week of May ahead of payrolls tonight, while the Chicago PMI for May came in at a strong 61.7, up from 57.6, also ahead of the national Manufacturing ISM out tonight.

Through all of this, the AUD has been trading through it post-Italy troubles range, pivoting around the mid 0.75s with no key market moving data today, but plenty next week including the RBA, Retail Sales, GDP (and pre-GDP partials). Base metals rose while Chinese iron ore and steel rebar futures rose yesterday. Coal prices are higher too, steaming coal above $US110/t. Brent was little changed, as was gold.

Coming up

NZ Consumer Confidence (8.00 AEST) and Terms of Trade Q1 (8.45)

AU AiG PMI Manufacturing at 8.30 (L: 58.3) and at 10.00 Corelogic house prices for May (L: -0.3%; expect a near repeat)

Kaplan speaks at 10.30, there’s the Caixin China Mfg PMI at 11.45 (L: 51.1; F: 51.2)

Tonight sees possibly revised EC PMIs for May, but the market will be focussed on payrolls and especially average hourly earnings (L: 0.1/2.6%; F: 0.2/2.6%). The ISM Manufacturing is expected to be 58.2, up from 57.3

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.