We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Italy’s travails continue and heightening oil prices are causing problems for Indonesia.

https://soundcloud.com/user-291029717/indonesia-and-italy-spoil-the-party

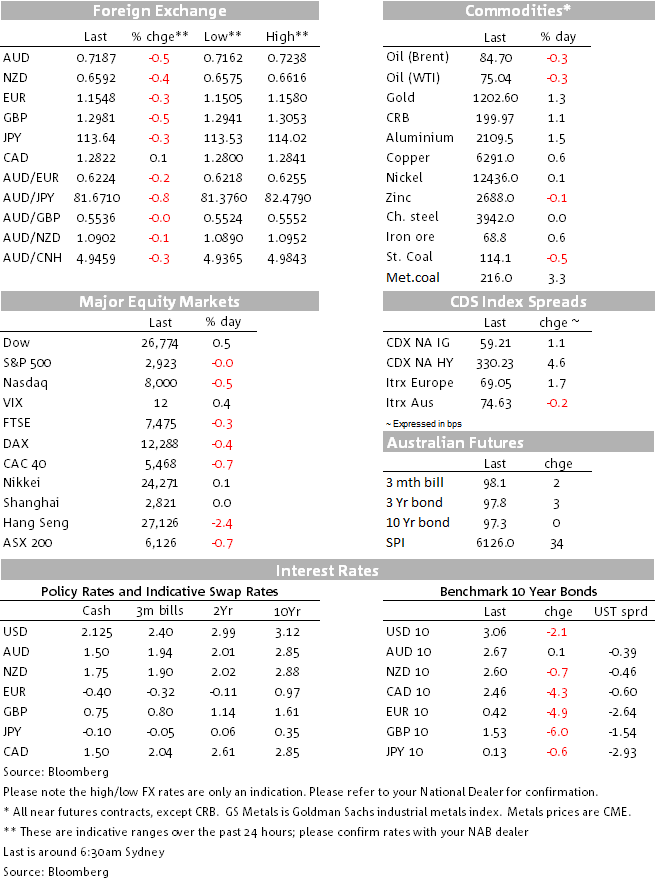

A fair bit of movement in FX markets in the last 24 hours, most of it from mid-afternoon AEST yesterday when both the AUD and EUR came under quite pronounced downward pressure, EUR/USD to a low of 1.1505 (it’s weakest since August 21st) and AUD/USD to 0.7162 (a two-week low). The Euro’s drop was entirely an Italian affair, while we’d place more of the blame for the drop in the Aussie at the door of Asian Emerging Markets.

Earlier pressure on the likes of the Indonesian Rupiah saw it rise above 15,000 for the first time since 1998, just post the Asia crisis and linked more to the latest spike in oil prices more so than the tsunami tragedy). The Korean Won was also significantly weaker, later joined by what proved to be a temporary spike in USD/CNH. The latter moved back above 6.90 for the first time since mid-August. The ADXY (EM Asia) currency index, to which AUD remains highly correlated, lost about 0.5% on the day.

The message is fairly clear; if we are not out of the woods regarding pressure on Emerging Markets – not just from the likely scaling up of US tariff actions on China but also rising US rates and potentially higher USD/EM Asia FX – the AUD is equally not out of the woods in terms of risk of returning to retest post-2014 cycle lows below 0.70.

On Italy, the Euro was under pressure as soon as the European market stepped in the door, with early selling pressure aggravated by reported comments from the head of Italy’s lower house of parliament, Claudio Borghi, that “I am very convinced that with its own currency Italy would solve the majority of its problems”. Shortly thereafter he made clear that the “There is no plan to leave the euro within this government regardless of my personal conviction”, sentiments echoed even more forcefully by several Italian cabinet ministers; but the damage had already been done.

In truth, ‘Italexit’ scaremongering is very much old news (there is limited public support for Italy exiting the Euro). The more significant issue is the risk – albeit not immediate – of Italy being downgraded to ‘junk’ status by at least two of the major ratings agencies and which would have profound implications for the ability of investors with minimum credit rating restrictions – including global sovereign bond market index trackers – from holding Italian government debt.

Moody’s and S&P review Italy’s sovereign rating before the end of October (after the budget has been submitted to the European Commission). All three major rating agencies rate Italy “BBB” (i.e. two notches above junk), and even if Moody’s were to downgrade Italy at the end of next month (its outlook is negative), it would likely be quite some time – and a willingness by the government to take some fiscal decisions which send their debt trajectory back north – before a downgrade to junk becomes a possibility.

In the more immediate future, there’s likely to be more negative headlines and volatility around the submission of the budget to the EC in mid-October, but we don’t expect Italian yields to skyrocket like they did earlier this year when the market started to question Italy’s membership of the euro. Consequently, there should be relatively limited spill-over to major risk asset markets. Our assumption is that by year-end, the budget situation will have been resolved to the ratings agencies satisfaction and that EUR/USD will be higher than it is today.

Elsewhere in FX, both the Yen and Swiss Francs showed a few of their traditional safe haven characteristics (JPY more so than CHF) while CAD continues to outpace other commodity-bloc currencies, still basking in the glory of Sunday night’s trade deal but more especially from Monday’s big ($2) advance in oil prices, most of which has stuck overnight.

The Dow Jones has just closed at a new record high of 26,774, up 0.5% on the day and 12% since the start of Q3 (so a near 50% annualised return in the last three months). The S&P500 (flat on the day) is still half a percent off its all-time high (from two weeks ago), while the NASDAQ is off half a percent, both of these indices weighed down somewhat by a 2% drop in Facebook’s share price.

This though doesn’t really deflect from the message that whatever is going on in most other parts of the worlds, there’s nothing to see here as far as sentiment toward US risk assets is concerned given that the bulk of corporate America’s revenue continues to be earned inside the United States. Helpful here though is the new NAFTA agreement (which looks very much like the old one, just with a much less catchy acronym (USMCA or United States Mexico Canada Agreement).

US treasury yields are lower at 10 years, down 2bps to 3.06%, a move almost entirely due to the contagion from lower German Bunds yields (-5bps to 0.42%) which in turn is a direct function of the latest back-up in Italian bond yields (10yr BTPs +15.4bps to 3.445%). Of note on the latter is that contagion to other Euro-peripheral bond markets has so far been minimal.

Oil gave back 25 cents or so of Monday’s strong gains, but other commodity prices are mostly higher, all bar zinc stronger in the base metals complex (including iron ore +0.6%) and metallurgical coal adding another $7 to bring its month to date gain to $16. Gold is also firmer, up just over 1%

No economic data of note overnight save that the latest Global Dairy Trade auction yielded a 1.9% drop in the main GDT index with the whole milk clearing price down another 1.2%.

Fed chair Jay Powell has been speaking but has not moved the dial on Fed rate hike pricing, reiterating the message that he backs ongoing gradual hikes for what he described as an ‘extraordinary’ economy. He says higher wage growth alone need not be inflationary (in which regard note Amazon’s announcement overnight of a lift to the minimum wage rates it will pay globally, though the overall impact on its bottom line is seen to be slight).

Nothing of note in our time zone today

In Europe, the UK services PMI tops the calendar, seen down to 54.0 from 543. We also get final EZ PMI readings and EZ retail sales. UK PM Theresa May addresses the Conservative party conference

Tonight in the US it’s the non-manufacturing ISM along with ADP Employment in front of Friday’s payrolls data. ISM is seen dipping to a still very strong 58 from 58.5

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.