Canada and US miss trade deadline, but agree to keep talking

Trade angst and EM fragility buoys the USD and hurts the AUD

Tech shares keep US equities afloat, but Europe and Asia close lower

UST curve steepens a little with 2y yields lower and 10s higher

Trump goes off on Twitter and threatens to make a deal without Canada

GBP opens under pressure amid leadership spill rumours and new Brexit tensions

Week ahead: Busy week with important data releases, but the big question is whether Trump will “double down” and impose new China tariffs

Domestic Focus: Retail Sales, RBA meeting and Q2 GDP

Offshore: NAFTA remains in focus; US-China tariffs end of consultation ; Fed speakers; US payrolls, ISMs; BoC meets, CA jobs; CH Caixin PMIs

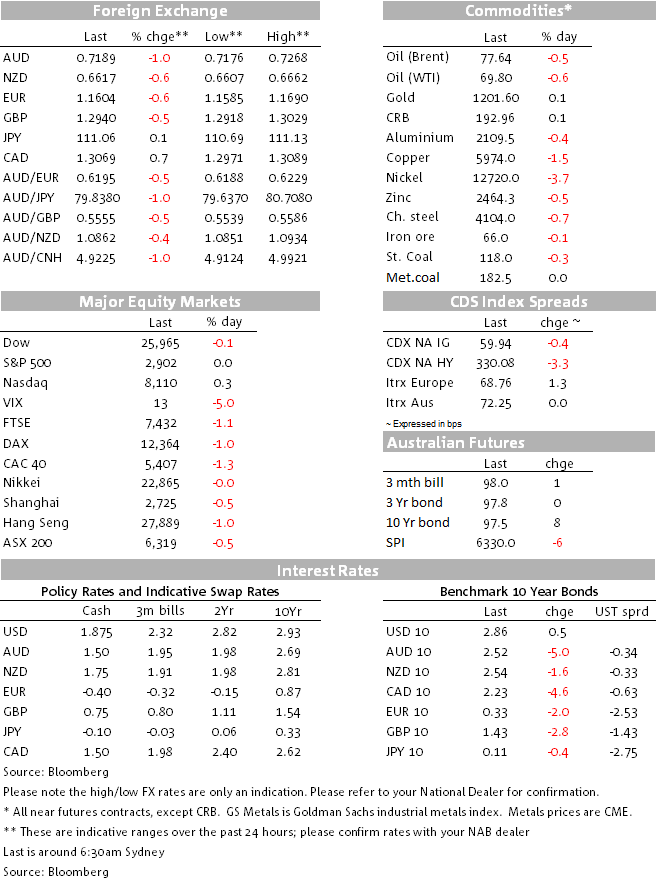

Markets ended the month of August with a sense of unease, as Canada and the US were unable to reach a deal for a NAFTA re-write. Both parties agreed to keep talking and negotiations will resume on Wednesday with a deal still expected, but unlikely to be reached until later in the month. Unhappy with the outcome, Trump took to Twitter on Saturday slamming Canada’s decades of abuse and again threatened to go back to pre-NAFTA if no deal is agreed. It remains to be seen if Trump can indeed cancel NAFTA without the US Congress support. In the meantime simmering in the background the consultation period over additional tariffs on $200bn of China imports ends this Thursday (September 6th) and if President Trump is unable to get his deals done, the concern is that he will “double down” on his protectionist strategy.

The big dollar was the main beneficiary from these concerns on Friday with fragility in EM equity markets also playing a supporting role. The MSCI EM index fell 0.20% on the day, ending the month of August down over 2%, its fifth consecutive monthly decline. In the end the USD closed the day broadly stronger with the AUD suffering the most within G10 pairs. Early our Saturday, news that Canada had failed to reach a deal with the US, dragged the AUD down just over 50pips to an intraday low of 0.7176, before a small recovery into the closed helped the pair end the month at 0.7192, its lowest monthly close since February 2016.

Currencies

The USD closed Friday with DXY up 0.35% and BBDX up 0.44%. AUD was the big G10 loser on the day, down 1% with EUR (1.1605), NZD ( 0.6620) and CAD ( 1.30) down around 0.60%. NOK managed to edge some gains against the USD (+0.26%) and CHF was essentially flat. AUD closed the month at 0.7189.

Despite a steady decline since reaching a high of just under 97 midway through August, the DXY index gained 0.62% in August and barring the safe haven JPY and CHF, the USD outperformed all other G10 currencies. SEK amid its political turmoil ahead of Sweden’s government elections next Sunday was the big underperformer (-4.33%) with AUD (-3.17%) and NZD (-2.87%) not far behind.

The pound was one of the top G10 performing currencies last week, up 0.89% and in part some of this performance was driven by positive Brexit News. GBP closed the week at 1.2963, but over the weekend PM May said she would not compromise on the UK government’s Chequers plan and in response EU’s chief Brexit negotiator Michel Barnier has said he is “strongly” opposed to key parts of Theresa May’s proposals for a future trade deal. Moreover the weekend press reported a potential leadership spill. GBP has opened lower today, down 50 pips to 1.2915 as we type and technically a move down to 1.2850 looks achievable near term.

Rates

On Friday the UST curve steepened a little bit with the 2y rate easing 2bps to 2.628% while the 10y tenor climbed 0.5bps to 2.86%. In the August UST yields were lower with the move led by the back end of the curve resulting in the 2y10y curve flattening 6bps to 23bps. Core Global yields followed 10y UST yields with similar declines.

Equities

Tech shares and the NASDAQ were the outperformers on Friday with the tech heavy index climbing 0.3% on the day, meanwhile the S&P and the Dow closed essentially flat. In Europe the Stxx 600 index fell 0.8% and in Asia the Shanghai Composite eased 0.46%.

Like Friday, US tech shares were the darlings in August with the NASDAQ up 5.71% while the S&P 500 gained 3%. August was a month to forget for Europe (EuroStoxx50 -3.76%) and Asia (Shanghai Comp -6.25%) but our S&P/ASX200 managed a small gain of 0.63%.

Commodities

Reports of increased US oil production weighed on WTI (-0.6%) and Brent (-0.5%) on Friday, but looking at the month as whole oil prices managed to record decent gains (Brent +4.27% and WTI +3.11%). Meanwhile trade induced woes has been the theme of the month for copper and LMEX with both over 1% lower on Friday and 6.4% and 3.8% respectively in August. Iron ore also had a bad month down 2.54% ( and -0.1% on Friday).

Economics

The Chicago PMI fell to a still-high 63.6 in Aug from 65.5 in Jul. That was a little above the 63 expected by consensus. The output and demand sub-indices increased a bit, and inventories improved, but employment weakened a little and businesses remained concerned about input price inflation with trade policy seen as one of the culprits.

The final August reading of the University of Michigan Consumer Confidence Index rose 0.9 to 96.2 vs a 0.2 expected increase. Still the index has been on a steady decline after peaking at 101.4 in March.

EZ CPI data for August missed by a tenth with Headline at 2.0% y/y (2.035% unrounded) and Core at 1.0% y/y (0.960% unrounded, so a low core print).

Baker Hughes count of active US oil rigs in the rose by 2 to 862. So despite concerns of pipelines restrictions, drilling in the US remains at elevated levels.

The US Energy Information Administration (EIA) reported US oil production jumped to 10.7m barrels a day in June, up from small pull back to 10.4m in May, keeping the uptrend in output.

S&P placed Argentina’s B+ long-term and B short-term ratings on CreditWatch negative. The Agency noted that the ratings on Argentina reflect its weak fiscal and external profiles, limited monetary flexibility despite greater fluctuation of the peso, and growing debt burden, which is predominantly denominated in foreign currency.

On Friday the US administration notified Congress of its intentions to sign a trade deal with Mexico in 90 days which could include Canada “if it is willing”. Under rules set by Congress, the President’s notification means the administration is now facing a 30-day deadline to provide a full text of the agreement.

Unhappy with the failure to reach an agreement on Friday, President Trump on Saturday expressed his feelings on Twitter saying “There is no political necessity to keep Canada in the new NAFTA deal. If we don’t make a fair deal for the U.S. after decades of abuse, Canada will be out,”. “Congress should not interfere w/these negotiations or I will simply terminate NAFTA entirely & we will be far better off.”

Coming up

The US is celebrating Labor day today suggesting it should be a quiet day ahead.

In Australia have a busy week of important domestic data releases with our economists expecting a reasonable Q2 GDP print of 0.7%, but the fragility of EM markets amid rising uncertainty over President Trump’s next move on trade policy means that the AUD looks vulnerable to the downside. Technically the AUD remains in a downward trend and support from the May and December 2016 daily lows do not look sturdy enough to stem the decline if we are to be hit by hostile trade news this week. Looking at the chart, a move sub the May 2016 low of 0.7145 opens an easy path for the AUD to have a look sub 70c and with the likelihood that the other big three AU Banks will sooner or later follow Westpac in lifting their variable mortgage rates, then the new week looks likely to be a tough one for the AUD.

It is also a busy week offshore with important data releases including US ISMs on Tuesday/Thursday and Payrolls on Friday, but the big question is whether Trump will “double down” and impose new China tariffs.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.