Total spending grew 0.9% in June.

The size of the Italian government’s budget deficit is causing concern in Europe.

https://soundcloud.com/user-291029717/italy-overspends-boris-spreads-division-naftas-midnight-deadline

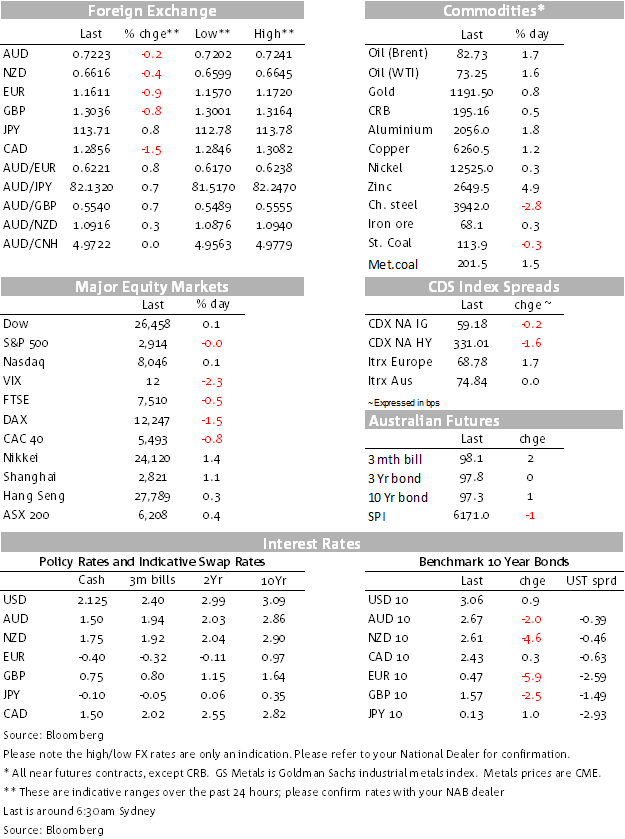

We start the start the week with the AUD trading around 0.7225, in its recently familiar range, the DXY losing some if its upward grip on Friday from somewhat underwhelming US consumer inflation report, but clawing back some territory late after European risk assets were dealt a blow from Italian budget woes. China’s PMIs released yesterday were mixed, the Manufacturing PMI below expectations.

The populist coalition government announced it was targeting a 2.4% fiscal deficit, much larger than the 1.6% being promoted recently by Finance Tria. Italian bond yields spiked higher, while European equities and the euro fell. The Milan stock exchange fell 3.72%, while European bank shares were down 2.8%, notable Italian bank names down by 6-9% on the day. The bout of risk aversion was reasonably contained to Europe though, with little contagion to US equities or US Treasury bonds (both ending little changed on the day). The US KBW Bank index closed down 0.9%.

Italian bond yields jumped after the Italian government announced a Budget deficit target of 2.4% fiscal deficit for each of the next three years. The two coalition partners, Five Star and the League, overruled Finance Minister Tria, and now seeking to push through campaign promises including a “citizens’ income” for the poor, tax cuts, and a rolling back of the retirement age for the state pension. Italian 10 year yields rose 27 bps, backing up to 3.147%, having been rallying in recent weeks on expectations of a less-stretched budget position.

The scene is now set for a clash with the EU, when Italy formally presents its budget to the European Commission (EC) in mid-October. EC Vice President Dombrovskis said on Friday that the budget “does not seem to be in line with the stability and growth pact.” The EU wants Italy to show fiscal restraint so the country’s debt-to-GDP ratio, which currently sits at over 130%, starts declining towards the EU’s target of 60%. Also, as my BNZ colleague Nick Smyth has pointed out this morning, Italy is rated BBB by all three major rating agencies (two notches above junk), but on negative outlook at Fitch and Moody’s. If Italy were downgraded to junk, it would drop out of the major global bond benchmarks used by global fund managers, and this could further pressure. Note also that the ECB’s QE is now being phased out.

After trading at around 1.1650 through most of the APAC session, the Euro dropped three quarters of a big figure in the first part of the European session, the AUD/EUR clambering back above 0.62 as a result of Italian budget news. Also weighing on the Euro was a weaker than expected Core CPI result for August for the Eurozone, coming in at 0.9% y/y, below market expectations of 1.1%. This series has been very choppy over recent months and it’s very hard to discern a clear trend. It’s been as low as 0.8% and as high as 1.1%, having averaged 1.0% last year and this year). ECB Governing Council member Lane downplayed the core CPI miss saying the ECB was “fairly sure” core inflation was on an upward path and that wage growth data had been “increasingly positive”.

The USD finished the week a little stronger but it was not home grown. Friday’s Personal Income and Spending report for August revealed income and spending growth broadly in line with expectations (real consumption grew 0.2% as expected), while the Core PCE deflator was flat in August (the market was expecting 0.1%), but annual growth remained at 2.0%, though it was a low 2.0%. No inflation danger bells ringing there.

New York Fed President John Williams (who has been on the hawkish side and now an on-going FOMC voter now at the helm of the NY Fed) offered some seemingly less-hawkish comments that while he expected inflation “to edge up a bit above 2 percent”, he doesn’t “see any signs of greater inflationary pressures on the horizon”. Williams said the Fed was “going to learn a lot along the way” as to whether the US economy could sustain a super low unemployment rate without generating meaningful inflation or financial imbalances, and policy would be need to be increasingly data-dependent.

As this note is written, the US and Canada are engaged in last minute talks over a revised NAFTA deal, with the self-imposed deadline midnight US time Sunday. The CAD had rallied Friday as US-Canada NAFTA talks continued and both sides seem tight-lipped on whether a deal will be nutted out. There remain several sticking points, including dairy and autos, important for both sides. Canada’s Ambassador to the US McNaughton has been saying in Ottawa that the talks are making progress but “not there yet”.

Released over the weekend, China’s official PMIs for September (and the Caixin Manufacturing PMI) revealed weaker than expected Manufacturing PMI at 50.8 from 51.3, a miss and the lowest since February and among the lowest for two years enlivening expectations of more macro policy support for the Chinese economy. The Export Orders component slipped from 49.4 to 48.0, playing to the thematic of US tariff impact. The Caixin measure also missed at 50.0, down from 50.6. Adding a measure of comfort, the Non-manufacturing PMI beat expectations at 54.9, up from 54.2 and 54.0 expected. The AUD is trading steadily this morning.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.