NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

President Trump’s protectionist measures and OPEC’s increased oil production could be the two major market influences this morning.

https://soundcloud.com/user-291029717/more-oil-and-added-protection-creates-early-risk-off-mood

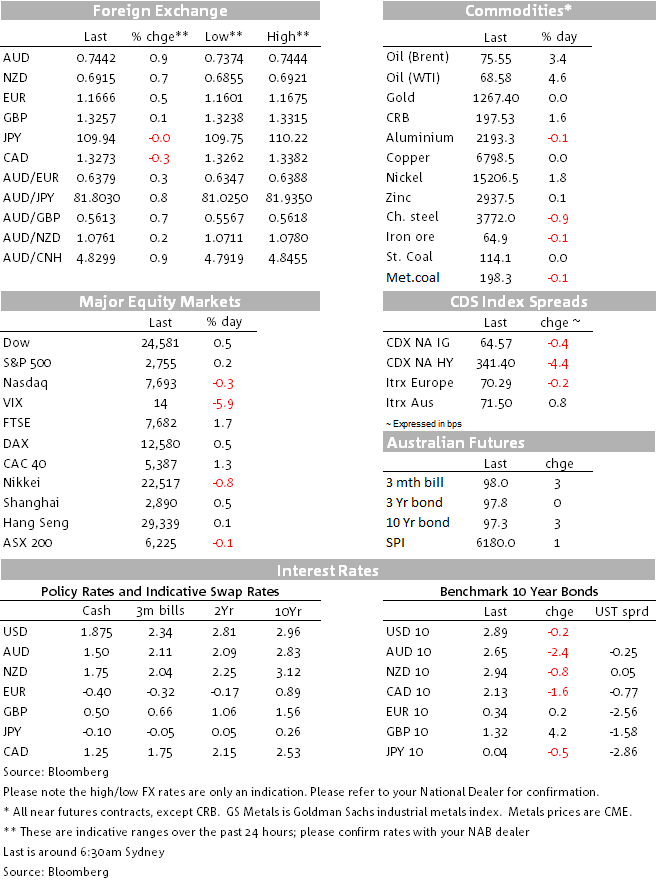

On Friday night OPEC confirmed plans to increase oil output next month, triggering a big jump in oil prices (Kriss Kross one hit wonder, Van Halen or Rihanna?), fuelling energy shares on either side of the Atlantic while also boosting commodity linked currencies with AUD the outperformer. It was a quiet night for bonds and the USD was broadly weaker with the euro helped by solid PMI prints. On Sunday the PboC cut the reserve ratio requirement to boost China’s economic growth, amid signs of activity slowdown and heightened trade tensions with the US. This morning Trump has ramped up protectionism via tweets and reports US will curb Chinese investment ahead.

OPEC reached an agreement to increase oil production by 1m b/d after a last minute compromise with Iran. But in what perhaps reflects the lack of shared views between members, the deal did not specify which countries would increase output and by how much. On Saturday the deal was ratified by non-OPEC nations and again no details were given on how the increase in production would be split between OPEC and OPEC allies.

As the increase in oil output is meant to be shared by all members/allies and many of them at this stage are unable to increase their current level of production, in practical terms the agreement is expected to result in an increase of 600k to 700k barrels a day. As such market reaction to Friday’s news boosted oil prices with both Brent and WTI enjoying their biggest one-day gain since 2016. Brent closed the day above the $75mark, up 3.42% while WTI gained 4.64%, ending the day at $68.58.

All that said the FT reported over the weekend that Saudi Arabian officials were widely disappointed with Friday’s oil price reaction and Mr Falih, Saudi Arabia’s energy minister was quoted as saying that “strict” adherence to individual production quotas would not take priority over adequately supplying the market. Reaction to Mr Falih’s comments may see oil prices give back some of their Friday’s gains at the start of the new week.

In spite of what was a very muted day for other commodities, the rise in oil prices lifted commodity linked currencies and helped the AUD become the top G10 performer on Friday. The AUD closed the week at 0.7441, up 0.83% on the day, but essentially unchanged on the week. NZD gains were also fuelled by the gains in oil prices with the kiwi coming second in the G10 leader board, up 0.57% and closing the week at 0.6908, closer to the bottom of its 0.6826-0.7060 monthly range.

Meanwhile the CAD was unable to fully enjoy the oil induced party initially selling off amid soft domestic data releases (softer CPI and retail sales, see details below) but the oil rally eventually helped the CAD end the day up 0.1% to end the week at 1.3269. Prior to the data releases pricing expectation for a BoC hike in July sat just above 70%, now they are at 54% and with NAFTA negotiations not getting any better the case for the BoC to stand pat in July is growing in popularity.

Early in the session, the euro was boosted by better than expected services and by inline manufacturing PMI readings. The data releases help the euro reach an overnight high of 1.16373 and although Trump’s tweet threatening a 20% trade tariffs on EU cars unless EU tariffs on US are not removed soon, weighed on the euro before the close, the union currency still managed to end the week close to the intraday highs at 1.1654.

Overall Friday was not a good day for the USD with the greenback also underperforming on the week. European currencies (ex GBP and SEK) and the yen where the big winners on the week and despite having a solid Friday, most commodity linked currencies underperformed the USD. Notably AUD was unchanged on the week

While energy shares managed on Friday to uplift many equity indices on either side of the Atlantic (S&P 500 0.2%, DJ 0.49% and Eurostoxx 50 1.125%), the picture on the week is less rosy with all major indices registering negative returns. Our S&P/ASX 200 was one exception boosted by gains in financial and healthcare while China’s Shanghai was the big loser down -4.73%. Overall the trade tension/uncertainty was overriding theme for equities underperformance over the past week.

Action in the bond market was relatively subdued on Friday. 10y UST yield closed essentially unchanged at 2.895%. Oil headlines pushed the benchmark yield to an overnight high of 2.9261% but then the Trump EU trade tweet was seemingly the catalyst for the 3bps rally that ensued before the end of the day. German Bunds were little changed on Friday but on the week they led the decline in core global bond yields.

Yesterday, the PBoC announced that it would cut the reserve ratio requirement for large commercial banks by 0.5% and cut reserve requirements for smaller banks. This action will free up over $100bn in capital. Larger banks will be required to use the funds towards debt-to-equity swaps while smaller banks can use the funds to extend credit. This easing in monetary policy follows signs of softer growth momentum in China and some market concern about the impact of US import tariffs.

This morning, the FT reports that the Trump administration has decided “to restrict Chinese investment in US companies and start-ups in sectors from aerospace to robotics as it prepares to deploy its latest weapon in the escalating trade war with Beijing”. It is set to come in a series of restrictions on inbound Chinese investment that Trump has ordered the US Treasury to draft and release this week.

As I am about to press the send button, headlines are hitting the screen with another Trump tweet “The United States is insisting that all countries that have placed artificial Trade Barriers and Tariffs on goods going into their country, remove those Barriers & Tariffs or be met with more than Reciprocity by the U.S.A. Trade must be fair and no longer a one way street!”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.