Robust growth for online retail sales observed in June

Insight

The Fed isn’t the only central bank making a call this week. There’s also that expected hike from the Bank of England, plus the central banks of Japan, Switzerland, Sweden and Norway.

US: U. of Mich. 5-10 yr inflation exp, Sep: 2.7 vs. 3.0 exp.

US: U. of Mich. cons. Sentiment, Sep: 67.7 vs. 69.0 exp.

US: Empire manufacturing, Sep: 1.9 vs. -10 exp.

US: Industrial production (m/m%), Aug: 0.4 vs. 0.1 exp.

CH: 1-Yr med.-term lending rate (%), 2.5 vs. 2.5 exp.

CH: Industrial production (y/y%), Aug: 4.5 vs. 3.9 exp.

CH: Retail sales (y/y%), Aug: 4.6 vs. 3.0 exp.

CH: Fixed assets invest. (YTD, y/y%), Aug: 3.2 vs. 3.3 exp.

Good morning

“Tommy used to work on the docks, union’s been on strike; He’s down on his luck, it’s tough, so tough”, Livin’ On a Prayer, Bon Jovi 1986

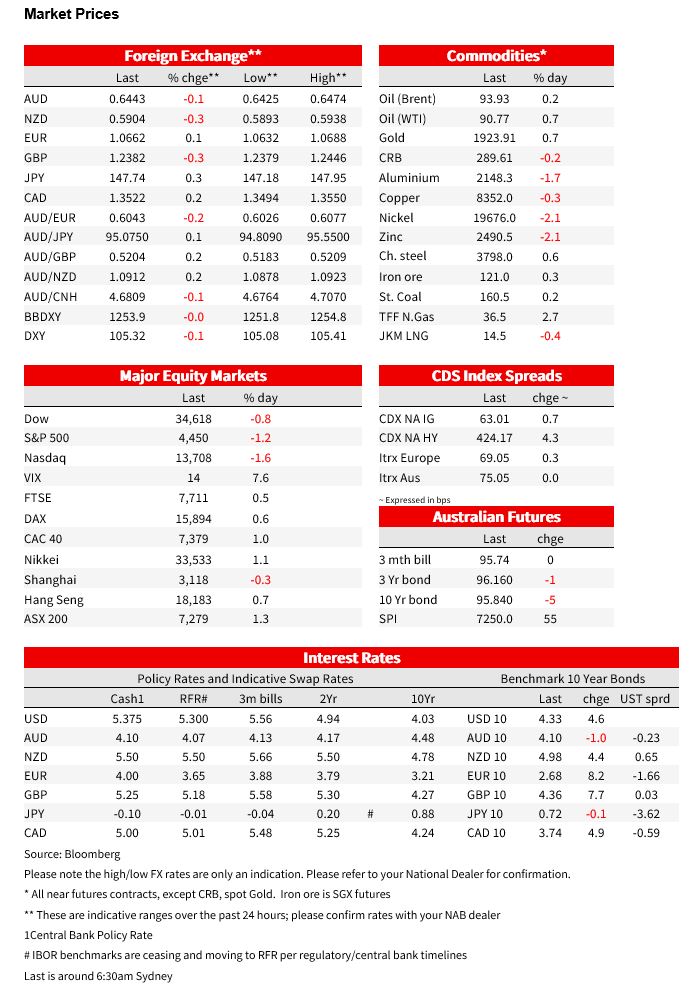

Yields rose on Friday following an ECB sources piece in the FT which pushed back on assertions the ECB is done hiking rates (see FT: ECB hawks warn of December rate rise if inflation and wages stay hot). German 10yr Bund yields rose 8.2bps to 2.68% (unwinding Thursday’s move lower post-ECB) along with US 10yr yields which rose 4.6bps to 4.33% – near its cycle high. The FT article was a clear push back by hawks on the market’s interpretation of Thursday’s post-ECB Statement where it was noted “ key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target.” Equities were mixed with APAC boosted by better than expected Chinese data and from the US session on Thursday (ASX200 +1.3%), but which wasn’t sustained in overnight trade with the S&P500 ‑1.2%. Technology stocks underperformed following indications of weak demand from Taiwan’s TSMC (NASDAQ -1.6%).

Data was mostly second-tier and did not have an enduring impact on markets. The most interesting was the US University of Michigan Consumer Sentiment where the 5-10yr inflation expectation fell back to 2.7% from 3.0%, its equal lowest since December 2020, though it was 2.7% in September 2022. The 1yr inflation expectation also fell back to 3.1% from 3.5% and is the lowest print since March 2021. As for headline sentiment, it was lower than expected at 67.6 vs. 69.0 expected and 69.5 previously. On the positive side the US Empire Manufacturing Survey beat at 1.9 vs. -10.0 expected and -19.0 previously. The survey is incredibly volatile, though it is worth noting the index for future business conditions rose to its highest level in more than year. Also out was US Industrial Production which beat at 0.4% m/m vs. 0.1% expected. Downward revisions blunted the beat and the better than expected outcome was not drive by manufacturing which was as expected at 0.1% m/m.

Earlier on Friday, Chinese activity data did beat, signalling some stabilisation in the economy after a series of incremental policy actions over the past few months. Industrial production grew 4.5% y/y vs. 3.9% expected, retail sales rose 4.6% vs. 3.0% expected, and fixed asset investment was 3.2% YTD y/y vs. 3.3% expected. APAC equities reacted positively with the ASX200 up 1.3%, with iron ore majors up sharply – FMG +4.0%; BHP +3.5%; RIO +3.0%. The Yuan advanced immediately following the data, but subsequently faded and ended little changed.

In FX markets, the US Dollar traded higher overnight Friday and was broadly flat over a 24 hour period (DXY -0.1%). Although EUR was stable (EUR +0.1%), the Yen underperformed amongst the majors and made a fresh 2023 low against the US Dollar (JPY +0.3% to 147.74). BOJ sources suggested financial markets had misinterpreted previous comments by Governor Ueda about potentially ending negative interest rates. The Antipodes underperformed within G10 with AUD -0.1% to 0.6443 and NZD -0.3% to 0.5904. Earlier gains, following the better than anticipated activity in China couldn’t be sustained.

Finally, and justifying today’s song title lyric, in the US UAW union automaker strike began a strike with around 11k workers touted to have walked out in the US. Strike action is on the rise and the WSJ noted last month, large stoppages from strikes resulted in 4.1 million missed days of work. That preliminary estimate was the biggest monthly total since August 2000 and importantly highlights the ongoing demand for higher wages. The UAW’s current demand is a wage increase of 36% over four years and to abolish the two tier wage system where it takes new workers four years to reach the same pay as long time employees. The carmakers offer is wage increases of up to 20% and/but they are not agreeing to remove the two-tier wage system.

Coming up this week

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.