Online retail sales growth slowed in May following a fairly strong April

Insight

Words from the RBA’s Governor Lowe send the Aussie dollar spiralling downward yesterday.

https://soundcloud.com/user-291029717/lowe-sends-aussie-lower-markets-unmoved-by-trump

For once most of the market price action of the past 24 hours occurred during our time zone, most notably in the AUD and local interest rate markets, after RBA Governor Lowe asserted in his lunchtime speech on the ‘Year Ahead’ that the interest rate outlook is now more evenly balanced. The killer paragraphs from his speech read:

“There are scenarios where the next move in the cash rate is up and other scenarios where it is down. Over the past year, the next-move-is-up scenarios were more likely than the next-move-is-down scenarios. Today, the probabilities appear to be more evenly balanced”.

“If Australians are finding jobs and their wages are rising more quickly, it is reasonable to expect that inflation will rise and that it will be appropriate to lift the cash rate at some point. On the other hand, given the uncertainties, it is possible that the economy is softer than we expect, and that income and consumption growth disappoint. In the event of a sustained increased in the unemployment rate and a lack of further progress towards the inflation objective, lower interest rates might be appropriate at some point. We have the flexibility to do this if needed.”

In subsequent Q&A. Lowe said that its ‘entirely plausible’ the next move is up, and ‘possible’ it could be down, adjectives which could be construed as suggesting the RBA still thinks a rate rise is slightly more likely than a cut as their next move (though as he earlier made clear, in either case not for a good while yet).

No matter, it was off to the races in the currency and rates market. OIS market finished the day with a quarter point rate cut fully priced by February 2019 (which some could interpret as meaning a near 50% chance that the Cash Rate will be lowered to 1% from 1.5% now, bearing in mind that back in 2016 when the RBA changed tack, rates were lowered from 2% to 1.5% in fairly short order).

On this, while we are not rushing to challenge the currency market’s response to Lowe’s comments, and tend to agree that if rates were to be cut once there’s a fair chance they would be cut twice, we would point out that in our short term fair value model for AUD/USD, a 50-point cut to the cash rate from present level only produces about a one cent fall in fair value – less than we have seen in the last 24 hours – and that we currently peg fair value at about 0.7150. As such, we aren’t rushing to suggest we are headed back sub-0.70.

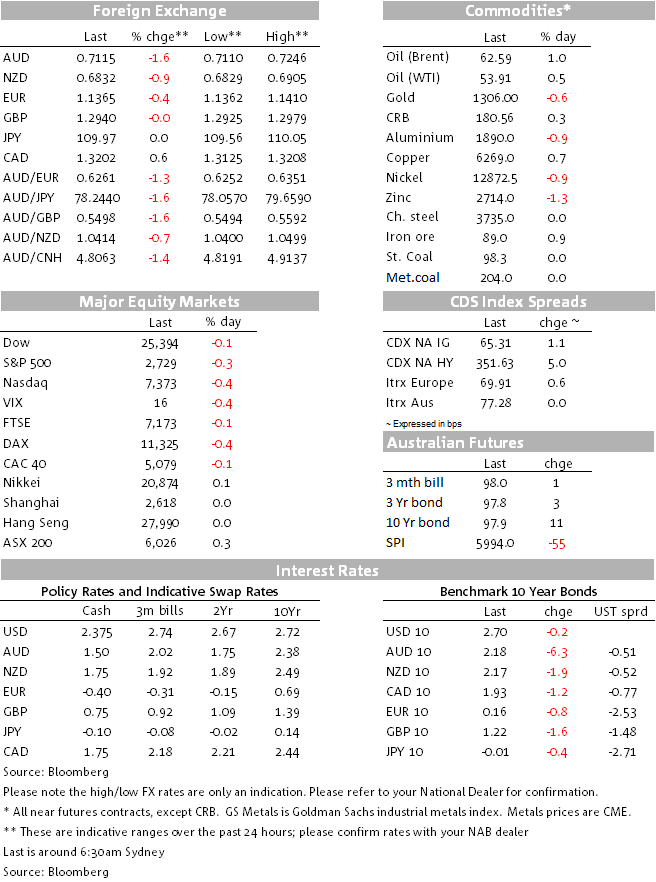

The AUD fell from 0.7240 to 0.7180 in short order post-Lowe, losses extending to 0.7140 by the Sydney close and 0.7110 offshore (we have been making fresh lows as I write). The moves had had predictable spill-over effects to other commodity linked currencies, with NZD the next worse performing G10 currency overnight (currently down about 1%) and CAD and NOK 0.6-0.7% lower.

Weakness across the commodity currency complex has come despite generally positive commodity price news. Yesterday iron ore futures added another 50 cents (to be 5.5% up on the week) after Brazil’s Vale declared force majeure on supply contracts following a judicial ruling preventing production restarting after last week’s mining disaster. Some 9% of Vale’s annual iron ore output is currently impacted.

The latest GDT dairy auction produced a winning bid up 6.7% on the prior auction (and 8.4% for whole milk powder), results which could see Fonterra lifting its estimated payout for the current season.

And oil prices are 0.5-1.0% higher, after the EIA reported a smaller than expected build in crude inventories last week (1.26 million barrels against the Bloomberg consensus estimate of 1.86 million).

Other news to note overnight included another bigger than expected drop in German factory orders, -1.6% in December (versus +0.3% expected) and now 7% down on a year ago. This took a fresh bite out of the Euro and is the main reason the DXY dollar index is 0.34% higher on the day.

The US November trade balance came in on the low side of expectations at -$49.3bn versus -$54.0bn expected, which largely reflects a drop off in imports that were front loaded ahead of the imposition of US tariffs on $200bn worth of Chinese goods.

On Brexit – and where GBP is little moved overnight – the EU’s Donald Tusk has been out saying there will be no new EU proposal to break the deadlock in Brexit talks regarding the backstop. The FT reports the EU is frustrated about the UK’s unclear position with Tusk “wondering what a special place in hell looks like for those who promoted Brexit without even a sketch of a plan for how to carry it out”.

UK PM May’s (hard line) response has been to say that if the EU wants the UK to leave with a deal, there will have to be changes to the Withdrawal Agreement. Assuming this is not to be the case, or not to the extent that allows May’s deal to win parliamentary approval, then we continue to look for an “Yvette Cooper Mark 2” plan that would prevent a no deal Brexit/lead the UK to request an Article 50 extension – a GBP-positive development to be sure.

Finally, an hour ahead of the NYSE close, US stock indices are anywhere between flat and 0.4%. US VP Mike Pence has been out saying he can’t guarantee there won’t be another US government shutdown though several Congressmen and women have been out saying they think it can be averted. US bond yields are unchanged at 10 years, currently 2.70%.

Germany factory orders -1.6% (0.3%E, -1.0%P); -7.0% yr/yr

GDT dairy auction winning price +6.7%

US Nov trade balance -$49.3bn (-$54.0bn E, -$55.5bn P)

Canada Dec Building permits 6.0% (-1.0%E, +22.6%P)

Canada Ivey Purchasing Managers Index 54.7 from 59.7

NZ Q4 labour market data are expected to look a bit slower, but only in a statistical sense, after the incredible strength displayed in Q3. The market is looking for a slight back-up in the jobless rate (4.1%, from 3.9%), slower growth in employment, but slightly stronger wage inflation.

Fed chair Jay Powell to host Town hall meeting with educators

NAB releases its quarterly (Q4) business survey

Germany Dec industrial production

ECB Economic Bulletin

BoE meeting (no change in Bank Rate expected

US weekly initial jobless claims, consumer credit

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.