Total spending grew 0.9% in June.

It’s looking likely the 1 March deadline for higher Chinese tariffs will be pushed back on the hope of progress on trade talks next month.

https://soundcloud.com/user-291029717/market-optimism-as-deadlines-pushed-back

Market sentiment has been boosted over the past 24 hours by some more encouraging news on US-China trade negotiations. Yesterday, White House press advisor Kellyanne Conway told Fox News that Trump “wants to meet with President Xi very soon” while the President added at a campaign rally that “we don’t want China to have a hard time.”

Adding some fuel to the risk on mood, Trump said overnight that “If we’re close to a deal where we think we can make a real deal and it’s going to get done, I could see myself letting that slide for a little while,” speaking of the looming 1 March date when tariffs on $200b of Chinese goods jump to 25% from 10%. “But generally speaking I’m not inclined” to delay raising tariffs, he added. He also said that he had no current plans to meet with President Xi in March and that he’s OK with either a deal of tariffs with China.

There is something for both sides of the risk-on/risk-off line for everyone in all of that in a market that’s being driven by soundbites as much as policy commitments. Talks start tomorrow in Beijing between U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin with Chinese Vice Premier Liu He.

While the trade issue is bubbling away, there is a little more hope now that Republican and Democratic negotiators have made some progress on a deal to avert another government shutdown. The tentative agreement provides $1.5b for “modern physical barriers” (a “wall” or a “fence” depending on what side of the political fence one sits on) along the border with Mexico, well below the $5.7b Trump has demanded. The deal needs to be signed off by the Senate and House as well as the President before Friday to avert a shutdown. Trump sounded lukewarm about the tentative deal, telling reporters “I can’t say I’m thrilled”, but said he would study the proposal.

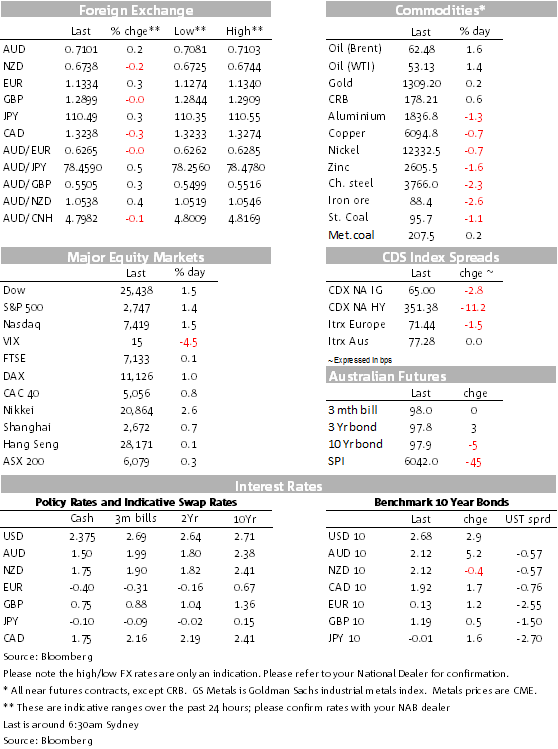

With markets back in risk on mode, equities are a sea of green in the US session as we go to print, the main board indexes all up comfortably over 1% (the S&P +1.32%), all sectors enjoying the ride after all the political machinations and a disappointing season for the earnings outlook, companies downscaling expectations for no earnings growth in the current quarter.

The USD has been on the back foot against most other major currencies, excepting (in part) the usually risk-absorbing Japanese yen and Swiss Franc. Since late APAC time yesterday the Yen has held its ground (JPY benefitting from a mildly yield-supportive for once BoJ) while the CHF has adopted its defensive risk-on posture. 10 year JGBs have been marginally negative recently. They did rise 1.6bps yesterday to -1.3bps (-0.013), but still short of the BoJ’s +0.10% 10y target.

The AUD and NZD have both inched somewhat higher in a mixed night for commodities and, for the NZD, ahead of what the market expects will be a more dovish RBNZ at its cash rate announcement window later today, now shifted to 2pm Wellington time, midday AEDT. The EUR and Sterling both performed a little better overnight. Dutch central bank Governor Knot has been urging for action to moderate Dutch house prices and meeting with other regulators to discuss what could be done.

Fed Chair Powell was speaking overnight to college students in Itta Bena, Mississippi (the second poorest US state), remarks familiar now to market thinking. He gave an understandably generally upbeat report on the national economy, saying that economic output has been growing at a solid pace, unemployment is at a near half-century low (it’s 7.3% in MS, well above the national average) and that officials “don’t feel the probability of recession is at all elevated.’’ He acknowledged that “prosperity has not been felt as much in some areas, including many rural places”, having been introduced as the most important visitor to the State since Bobby Kennedy in the 1960s.

Also speaking overnight, BoE Governor Carney called for clarity over Brexit in an economy that barely grew at in the final quarter, growing by just 0.2%. “What those figures show”, he said is underscoring the “importance of a transition to whatever end-state Parliament decides.” “There is a very high level of uncertainty of the degree of access companies are going to have in the next two months, which is quite an extraordinary situation to be in,” he said. “Quite logically, rationally, understandably, they are holding back on making bigger investment decisions. Those who have contingency plans are putting them in place” he said, adding “but not all companies can self-insure against this possibility.”

He also expressed his hope that out of Brexit might evolve new freer trade in services as helping to resolve external imbalances, “barriers to services trade currently up to three times higher than those for goods, the Bank estimates that eliminating this differential could reduce the excess deficits of the US by up to one third and of the UK by up to one half.” This, he hoped, might also build a bridge to resolve the democratic shortfall in the current system. These are interesting thoughts from someone who has in the past championed the risk of Brexit through Project Fear.

The data flow was relatively light overnight with the US NFIB Small Business Optimism Survey for January (101.2, down from 104.4), still high historically but the lowest since the post-Trump election bounce. It was also likely plagued by the government shutdown, but it’s been pulling back for the best part of six months now, small businesses expecting softer economic conditions and sales. Also released was the US JOLTs Job Openings report for December, of historical interest largely, but revealed record openings and still strong rates of labour turnover (new jobs, hiring, separations, and quit rates), reflective of the still strong labour market.

Oil has had a good night, WTI up by 1.39%, buoyed a little by a marginally softer USD, but also getting some support despite the EIA raising its 2020 projected US crude production forecast to 13.2m b/d from 12.86, production currently 11.9. Base metals were softer, iron ore has rebalanced lower as the market weighs up Vale’s production woes against possible mandated Chinese steel cuts ahead of the summer. Met coal was higher but steaming coal eased. Gold was little changed. US Treasury yields rose by 2-3 bps.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.