Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

So what now for Brexit? Plus the marked reaction to yesterday’s Fed forecasts.

https://soundcloud.com/user-291029717/may-day-for-uk-hits-sterling-a-week-out-from-brexit

I’ve changed my mind, I take it back Erase and rewind – The Cardigans

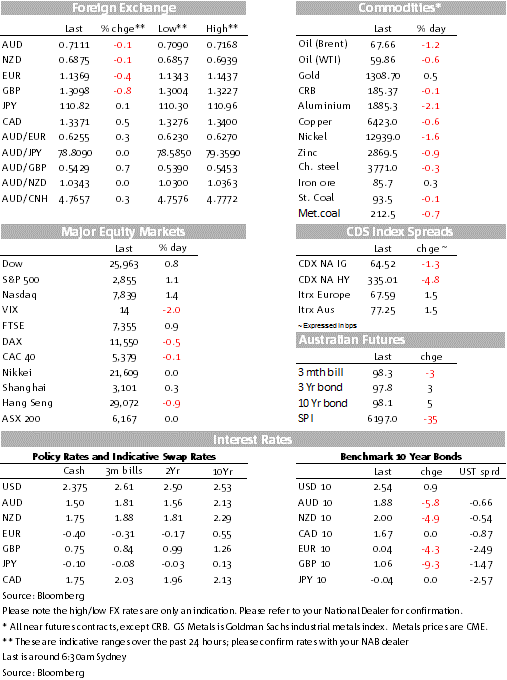

Markets have continued to digest the implications of a dovish Fed that looks set to leave the Fed Funds rate unchanged this year and potentially next. Tech shares have led the gains in equities, although financials have continued to struggle. USD indices have erased their post Fed losses with AUD and NZD also giving back their post Fed gains. Brexit woes is one factor at play, although arguably the USD is still supported in its own right. In a world where central banks are going nowhere in a hurry, the USD looks attractive amid a likely low volatility environment and carry appeal.

US shares look have closed the day with decent gains ( S&P 500 1.09% with the IT sector leading the charge while a flatter yield curve weighed on financial shares for second consecutive day. Europe had a mixed night, but notably bank shares also underperform amid broad declines in EU government bond yields.

USD indices have essentially erased all of their post Fed losses with DXY now trading at 96.471, up 0.74% over the past 24 hours. Looking at G10 pairs, the USD is stronger across the board with GBP leading the declines amid ongoing Brexit woes while NOK is the only outperformer boosted by the Norges Bank decision to hike its policy rate by 25bps to 1.0%. The decision was expected, but the surprise was in the guidance with the Bank retaining a tightening bias (“Our current assessment of the outlook and balance of risks suggests that the policy rate will most likely be increased further in the course of the next half-year”). NOK now trades at 8.4591 (+0.30%), after trading down to 8.4112 immediately after the Norges Bank policy announcement.

Brexit news remain pretty fluid and mostly not very encouraging for the pound. PM May pitched her delay plan to the EU and as we type it seems that the EU is considering an unconditional extension until May 7 ( the UK was aiming for a conditional extension to June 30th ), but of course if PM May is unable to get her deal through Parliament next week a longer extension is likely to be granted subject to the UK agreeing to hold EU elections end at the May. Meanwhile back at home, DUP’s Wilson said ‘we are no closer to backing Brexit deal’, so at this stage the prospect of Parliament passing PM May’s Withdrawal Agreement next week remain slim. Unsurprisingly Brexit uncertainty has weighed on GBP with the pair drifting lower over the course of the night, trading down to a low of 1.3004. News of the EU counter offer has helped the pair stabilise just above the figure ( @ 1.3097).

Brexit induce GBP weakness had spill over effects onto other European currencies with the euro giving back most of its post Fed gains. The pair now trades at 1.1364, after trading to an overnight low of 1.1344. A reading of EU Consumer confidence remained pretty subdued in March printing at -7.2 essentially unchanged from previous month.

AUD and NZD also gave back their post Fed and post-employment (AU) and GDP (NZ) gains overnight. After trading very close to its year to date high (0.6940 vs 0.6942), NZD now trades at 0.6874 and AUD is at 0.7111 after reaching a high 0.7168 post yesterday’s solid AU labour force report. Both antipodean currencies have succumbed to a stronger USD overnight despite an improvement in risk appetite evident by the gains in US equities. Brexit woes is an offsetting factor for risk sentiment, that said a case can also be mad for a stronger USD in its own right. In a world where major central banks look set to remain on the sidelines for the remainder of this year with the risk of easing more likely than tightening, the US economy continues to win the least ugly contest. Thus the USD looks attractive amid a likely low volatility environment and carry appeal.

US Treasury yields fell post yesterday’s Fed statement and consolidated the move overnight. The US 10 year yield did try and press lower as yields in Europe fell, dipping just under 2.50% at one point. But it has since recovered to sit around 2.54% currently, nearly up a point on the day. The Fed’s more-dovish-than-expected statement is clearly supportive of Treasuries. However, we see them struggling to rally too much further from current levels in the absence of weaker data. We see the 10 year note towards the bottom of a 2.40% to 2.90% range.

Commodities had a mixed to soft night, iron ore (+0.30) and gold (+0.50%), but these modest gains were offset by declines in Brent oil (-1.21%) and Aluminium (-1.94%)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.