Coming in for landing in a heavy cross wind

Insight

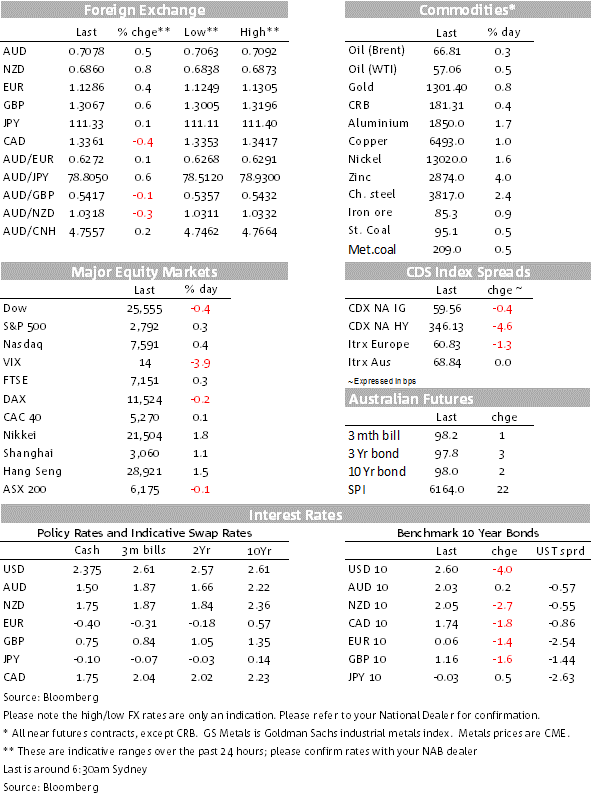

Boeing's share price has driven the Dow down whilst lower than expected inflation will have had a bit to do with bond prices today.

https://soundcloud.com/user-291029717/may-defeated-boeing-grounded

Brexit has continued to dominate the market’s attention in the past 24 hours, with a new deal yesterday then the vote on that deal in the House of Commons this morning.

A vote on the revised further 11th hour deal nutted out between May and Juncker has been lost in the Commons by a resounding 242-391. PM May announced to the Commons that she will proceed with a vote Wednesday on whether to leave on 29 March without a deal. The news is that PM May has told the Commons that this will be a ‘free vote’ for Tory MPs, allowing Conservatives, including cabinet ministers to vote against the government and not be sacked or forced to resign.

That vote tomorrow seems certain to go against the government as well. In other words, there is a majority in Parliament that will wish to avoid a ‘no deal’ crash out Brexit deal. That will be followed by a vote on Thursday to extend Article 50 (assuming this also finds a majority in favour of an extension – as we expect), likely of some comfort to GBP. That’s very likely to be supportive of Sterling. It’s still a fast moving environment, political pressure at understandable extreme levels.

In the immediate aftermath of the vote, Sterling has been whippy but not finding new direction. After rallying yesterday by two big figures on the prospect of a deal, most of those gains were reversed overnight as it became clearer that it would not be approved by Parliament.

Sterling this morning is sitting at 1.3060, AUD/GBP at 0.542.

The Aussie meanwhile has continued to garner some further limited support in what’s transpired for the session as a mildly risk-on one. An important support has come from yet another softer than expected reading on US consumer inflation. February Headline CPI rose by 0.2% as expected, taking annual CPI down to 1.5% from 1.6% from base effects, but core CPI rose by a softer than expected 0.1%, the market expecting another monthly rise of 0.2% that would have seen annual core steady at 2.2%.

Instead annual core CPI was 2.1%,a tenth less than expected, further supporting bond and relative valuations of other asset classes such as stocks. The US 2 year Treasury has rallied by 2.46bps to 2.4506%, 10s by a somewhat larger 3.60bps to 2.6033%, within sight of the 2.50% early-year low so far this year.

The S&P500 and the Nasdaq are both higher (by 0.4-0.5% as we go to press), but the Dow is lagging, owing in part to further attrition in Boeing’s share price, along with some softness in other big board names.

Boeing’s shares are down so far in this session by a further 6% on news in the past 24 hours of further countries grounding the 737-8 Max aircraft involved in the Ethiopian plane crash. Some other main board stocks such as 3M, JPM, Nike, Coca-Cola, and Caterpillar are also languishing, to a much more limited extent.

Released earlier than expected, the US NFIB Small Business Optimism Index for February showed something of a recovery after the ructions from the government shutdown at the start of the year. The headline index rose marginally to 101.7 from 101.2 (102.5), also coming after the equity market volatility at the end of last year had dented small business confidence.

It wasn’t a resounding spring back, but a hopeful one, unlike yesterday’s local NAB Business Survey for February that confirmed a further slowing in business momentum into the first quarter of this year. Both the NAB Business Conditions and Confidence indexes were down 2 points to below long term average levels, held back by particular weakness in Retail and Construction (likely candidates for weakness) as well as in NSW. The Survey’s release also came with another soft read through on Housing Finance approvals for January, pointing to further particular softness in Investment Lending approvals across the country.

By this time next year, the market is now pricing for a 1.115% cash rate, pricing in one cut by September and just over 50% of another. NAB looks for two cuts from the RBA this year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.