Coming in for landing in a heavy cross wind

Insight

The markets are on-hold ahead of the FOMC meeting later in the week.

https://soundcloud.com/user-291029717/may-may-have-to-delay-for-another-day

It’s been an overnight holding pattern with little to no data and markets trading in familiar ranges.

The only data of note was the US NAHB Housing Index for March which revealed a steady and still high level of 62, the two “single family sales” present and future components both higher but the prospective buyer traffic component down. The rally in the bond market in recent months seems to have done the trick by restoring borrowing affordability for prospective buyers.

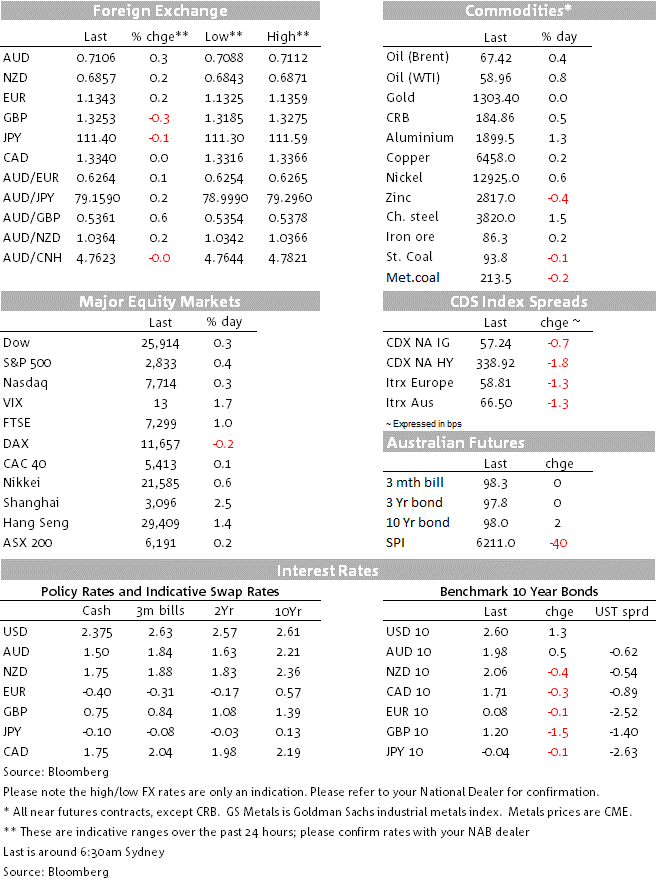

The USD has been steady, the DXY index at 96.487 this morning, right in the middle of its range of recent days ahead of the FOMC. US Treasury yields are also little changed, both two and 10 year yields up 1-1.5bps overnight. European bonds were also little changed, Germany’s 10 year bund at 0.083%.

With the EU Summit approaching later this week, all eyes have been on whether PM May can get another deal together with the Europeans that would get the support of sufficiently more MPs in the Commons, before the Summit. It seems not. Sterling is down 0.37% since late afternoon trade yesterday to 1.3230-35 as the possibilities on the next big steps come back into contention, not that they were far away. (The AUD/GBP is at 0.536 this morning; the AUD also down from its late yesterday highs in the 0.71s.)

The Speaker of the House of Commons warned PM May that she will not be able to re-table the same Brexit deal to another parliamentary vote, thanks to a convention dating back centuries that stops a government from re-tabling the same proposal as tantamount to bullying of the Parliament. She can only put it to a vote if there are substantial changes to it. Another proposed deal then would likely require at least a meaningful change to the Irish backstop, a key point of contention. Given the EU’s stand seems to be that negotiations have finished on the Withdrawal Agreement, if that’s right then time’s up, and so the odds of May’s soft Brexit plan being approved now have fallen dramatically.

Earlier, there was talk of May not getting the required support of the DUP anyway, feeding a weaker GBP. The media report that May will ask the EU for a nine month extension, which means several more months of uncertainty about the endgame for Brexit, but likely some further near term relief rally in Sterling, subject to the other potential political developments. Those next big possibilities include: the status quo in terms of leadership as May battles on for another nine months, a PM leadership challenge, fresh elections, a second referendum on Brexit, and revoking Article 50 all still remain in the mix.

On the commodities front overnight, the larger mover has been in Dalian iron ore and Chinese steel rebar futures, both up by over 1% amid the continuing uncertainty over the supply from Brazil. It also comes ahead of updates from the industry at the Global Iron Ore & Steel Forecast Conference being held in Perth tomorrow and Thursday in Perth. The Conference includes updates from BHP, Fortescue, from the Singapore representative of the Dalian Futures exchange, and more.

Just released this morning, NZ Consumer Confidence for the first quarter shows Confidence back down from 109.1 to 103.8. It’s not a market sensitive release.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.