Online retail sales growth slowed in May following a fairly strong April

Insight

The markets outside of the British Isles have seen some positive sentiment, including Australia.

https://soundcloud.com/user-291029717/bojo-goes-davis-departs-its-mayday-for-the-tories

No new news from the US-Sino trade war has helped investors focus back on fundamentals and with the US earnings season starting later this week, the US has led the gains in equities overnight. Commodities also had a good night, helping the AUD retained most of yesterday’s gains. GBP remains volatile amid cabinet resignations and the USD staged a comeback in the US session aided by a move higher in US Treasury yields.

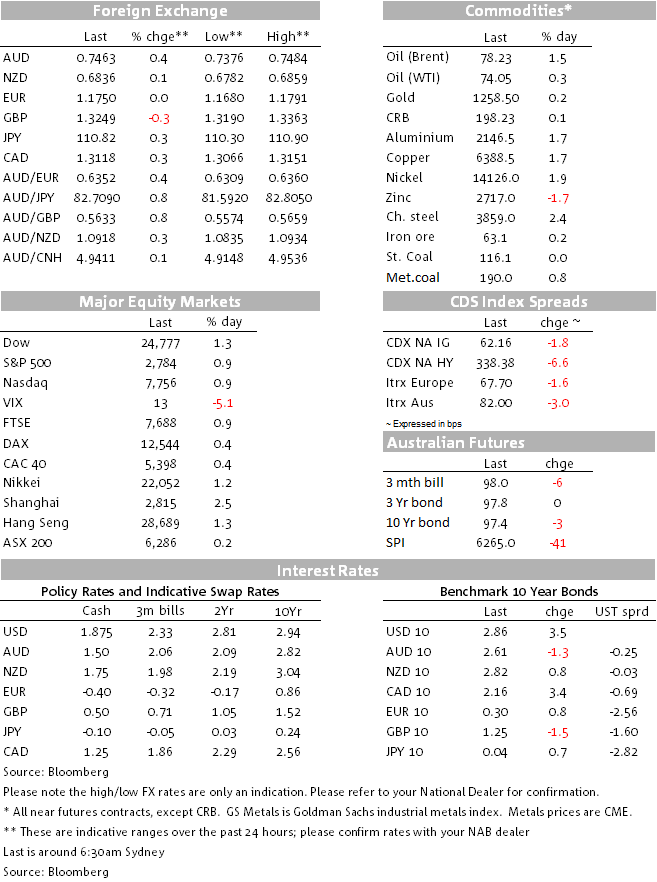

It was a good night for equities on both side of the Atlantic, but US equities were the outperformers with the Dow leading the way, up 1.31%. Lack of new news in US-Sino trade tensions have helped the S&P500 record a third day of positive returns with financials and industrial shares leading the way. IT and Energy shares led the gains in Europe with the later probably benefiting from a solid night for commodities.

Copper and aluminium have led the gains, up 1.97% and 1.65% respectively while Brent (+1.45%) and metallurgical coal (+0.80%) were not too far behind. So amid this positive backdrop, which also saw the VIX index dip down to a 12 handle for the first time in two and a half weeks, the AUD has retained most of yesterday’s gains and as a result it is the best G10 performer over the past 24hrs. The aussie currently trades at 0.7467, up 0.50% relative to levels this time yesterday and with President Trump seemingly too busy with a Supreme court nomination and NATO negotiations, the lack of new news in the trade front has been good news for the AUD. So near term the AUD has room to trade higher, but we remain sceptical the currency can sustained a move above 75c. We think it is only a matter of time before Trump makes an announcement on additional China trade tariffs ( more likely next week, if not the week after) and thus we wouldn’t be surprise to see the AUD eventually coming under renewed downward pressure.

GBP has seen a fair bit of volatility overnight trading in a 1.3190-1.3363 range ( now at 1.3252) after Boris Johnson followed David Davies and his assistant (Steve Baker) in resigning from PM May’s Cabinet. The resignations have sparked speculation over a possible leadership challenge, (48 MPs are needed to initiate a challenge), but in the event, we think it is unlikely there are enough votes for the PM to be ousted. Overall, while PM May’s move to a softer Brexit is a positive, there are still a lot of uncertainties. At this stage the proposal is short on detail, it provides a solution for goods trade with Europe, but there is no clear strategy on the services sector which represent around 80% of the economy. Europe is unlikely to offer an opinion until its sees the white paper, so it remains to be seen if this proposal is workable and next week the custom and trade bill may also present a big obstacle for PM May’s proposal. Political uncertainty remains a big cloud over GBP, making it a dangerous currency to trade and this is unlikely to change any time soon.

The risk positive backdrop has also seen US Treasury yields edge higher overnight with the move led by the back end of the curve. 10y UST yields are up 3.4bps to 2.8% but remain well within last week’s tight ranges. Focus is now likely to turn to the 3y, 10y and 30y supply this week, as well as CPI on Wednesday.

Amid a higher UST yields, the USD staged a small recovery during the US session with the DXY index back above the 94 mark. Unsurprisingly, amid the rise in UST yields, the USD was notably stronger against the yen, USD/JPY now trades at ¥110.82, up 0.34% over the past 24hrs. The trend line from the 2015 highs continues to suggest some resistance should be expected around the ¥111 mark.

On other news, ECB president Draghi addressed the European Parliament overnight and said that “We’re confident that basically thanks to our monetary policy the inflation rate will converge to our objectives,”. Draghi also urged lawmakers to push back against creeping protectionism, which he singled out as the main risk for the area’s economic expansion.

Lastly just release this morning, CFTC positioning data through to 3-July showed net NZD shorts extending to 26.4k, a record position. Our BNZ strategist notes that NZD is up 1.5cents since ( now at 0.6837), so some of these likely closed over recent days. USD longs extended, at the expense of CAD, GBP, JPY and NZD and notable improvement in MXN as well. Insignificant change in AUD positioning to remain moderately net short.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.