Online retail sales growth slowed to almost flat in March

Insight

NY Fed’s Williams stressing importance of financial conditions in policy reaction function..

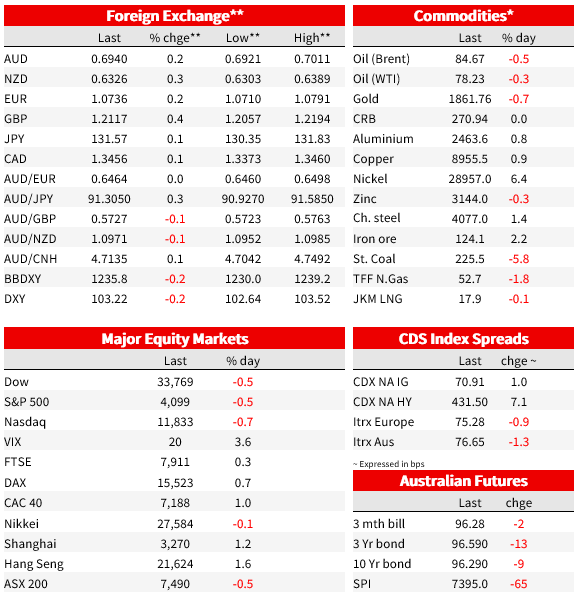

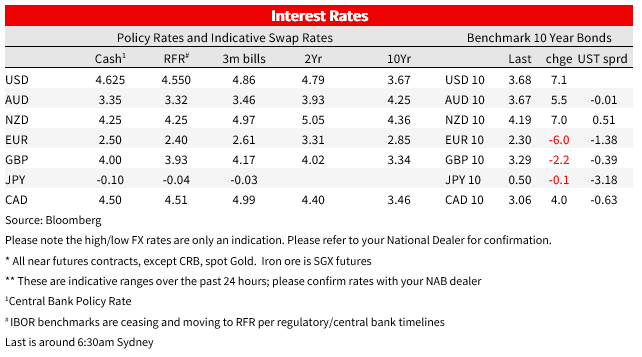

It was a quiet night for news flow. US yields are higher amid growing bets the Fed will push higher after last Friday’s strong jobs numbers, but there was little new information overnight. Gains in the shorter end saw the 2s10s curve widening to its most inverted level since the early 80s at -87bp, though has since narrowed back to around -82bp

US equities were higher through most of the US trading day, but declined over the session. The S&P500 opened around 1% higher, but declined through the day to now be around 0.5% lower. The NASDAQ is around 0.7% lower, while in Europe the Euro Stoxx 600 index closed 0.6% higher.

US yields were higher. US 2yr yields rose 8bp to 4.50% while the 10yr rose 6bp to 3.68%. The 2yr yield in the wake of the US Payrolls data last Friday is now at its highest level since November 30, after falling as low as 4.03% as recently as 2 February. The 2s10s spread flattened marginally to -82bp, but intraday fell to as low as -87bp, surpassing the earlier December lows and the lowest since the early 1980s before a late selloff in 10yr treasuries. Richmond Fed President Barkin added to the chorus of Fed-speak this week. His views were consistent with others on the committee, noting still-elevated inflation that “makes the case for us to stay the course…I think we’ve still got a ways to go”.

US initial jobless claims rose 13k to 196k, larger than the consensus for 190k. That was the first rise in six weeks after a January. Other indicators including higher layoffs reported in the Challenger layoffs series could point to further increases from here, though the level of jobless claims remains very low. Headline grabbing layoff announcements continue, with Disney saying it would cut 7,000 jobs or 3% of its workforce.

The delayed preliminary German January CPI showed HICP 9.2% higher over the year from 9.6%, a five-month low. The delayed release was due to technical issues, and less information than usual was provided in the data. Significant weighting changes and no information of how the figure was adjusted for government subsidies to cut energy bills make it hard to read too much from the result. The final number is released on 22 February.

Currency moves were generally muted on net, with the notable exception of Sweden and Norway. The US dollar was 0.2% lower on the DXY at 103.22. The AUD gained 0.2% and is now around 0.6940, though did get above 70c intraday before paring gains alongside the move higher in US yields. As for the exceptions, The Swedish krona was 2.3% higher, the move also spilling over into a 1.5% higher NOK. The new Swedish Riksbank Governor Thedeen was hawkish in the first evidence of his monetary policy stance since taking office. While the 50bps hike in the policy rate to 3.0% didn’t surprise, the Bank said it would actively sell bonds (quantitative tightening) from April. The statement made direct reference to the krona, overtly stating that “a stronger krona would be desirable,” a stark departure from previous communication which had been sanguine about a weaker krona.

Bank of England members were testifying to parliament, where the contrast between the more hawkish majority and dove Tenreyro was clear. On the more hawkish side, Haskel noted the need to “guard very vigilantly against really bad outcomes,” adding “I am super worried about going under the target, but, as I say, given the uncertainties at the moment, I’d rather put a rather little bit less weight on that medium-term forecast, ” Tenreyro, in contrast, said “where things stand right now I would see myself considering a cut.” The UK 2yr yield was 3bp higher at 3.5%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer

Online retail sales growth slowed to almost flat in March

Insight

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.