Robust growth for online retail sales observed in June

Insight

Markets are showing relief that the key US CPI release overnight was not higher than expected

Data round up:

US: April CPI 0.4% m/m vs 0.4 expected.

US: April CPI ex food, energy 0.4% vs. vs 0.4 expected.

US: April CPI 4.9% y/y vs 5.0 expected.

US: April CPI ex food, energy 5.5% yr/yr vs 5.5 expected.

Want me to love you in moderation, Do I look moderate to you? Sip it slowly and pay attention, I just have to see it through – Florence and the Machine

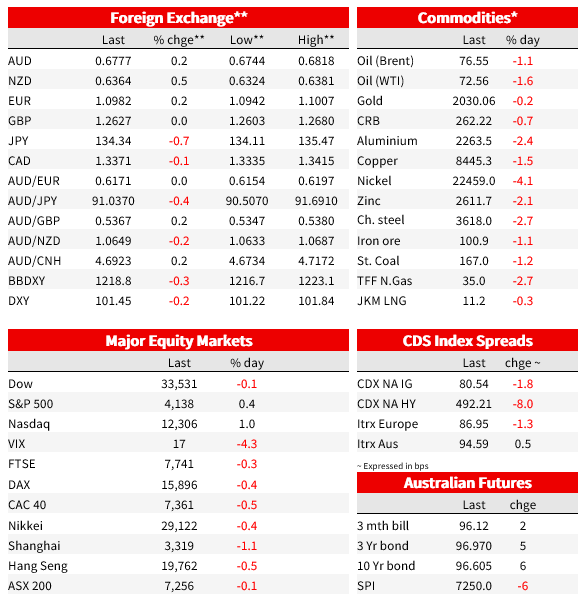

US CPI may not have come in materially different from expectations but the absence of any upside surprises sufficed to generate a relief rally in the bond and US money market, higher stocks (NASDAQ-led on lower bond yields) and a weaker US dollar, the latter enabling AUD/USD to briefly punch above through its now two-and-a-half-month range top (to a high 0.6820). But as with the USD, knee-jerk moves have failed to be sustained and AUD is back below 0.68 (still 0.25% up on the day). The BoE rounds out a second week of G10 central bank action tonight, while US PPI and China CPI and PPI are the highlights of the economic data calendar.

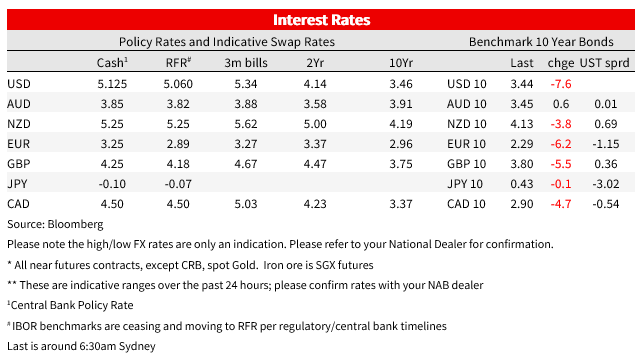

The week’s main economic events has come and gone without a huge amount of fanfare, but there is noticeable impact on bond and money markets, where in the latter the prior 4bps of Fed tightening priced into June Fed Funds futures has reduced to zero, and the strip now has more than 75bps of easing priced for December (-78bps to be precise, down from -65bps pre-CPI). In bonds, bullish curve steepening has been the order of the day, with 2-year yields down 11 bps and 10s 8.bps – continuing the re-steepening theme that is wholly consistent with the US economy being on the cusp of recession.

CPI showed 0.4% monthly rises for both headline and core in line with expectations (the ‘core’ median had ticked up from 0.3% to 0.4% in the day or two leading up to the release). The headline year-on-year rate of 4.9% was against an unchanged 5.0% expected thanks to rounding and is the first sub-5% headline print since April 2021. Ex-food and energy ticked down 0.1% to 5.5%, in line with expectations.

Some of the detail is encouraging, for example ‘core services ex rent up just 0.1% on the month and core services ex energy and rent – akin to the Fed’s currently preferred ‘cores services PCE ex housing’ at 0.2%. As for the identical headline and core monthly readings, this was largely because gasoline prices (+3%, but with ‘household energy services’ -1.7%) and food prices (-0.2%) largely cancelled each other out. Used car prices jumped 3% on the month, catching up with previously higher car auction prices, but the latter have since fallen back down which bodes well for falls in the CPI measure in coming months.

Not much to note in terms of economic data overnight bar Norway CPI (See currencies below) though ECB speakers have again been out in force, with some pushback against the generally hawkish rhetoric from the day before. Of note the Banque de France’s Villeroy says there is only a ‘marginal’ distance left to cover. Governing Council (GC) member Muller (Estonia) hinted at scope for pause in the cycle, saying that rate rises so far have been fast and that we’ve reached a level where’s it’s reasonable to evaluate what the actual effect on the economy is. And the GC’s Mario Centeno offered a view that we ‘may be nearing the moment’ where borrowing costs reach their peak for the cycle and may start falling at some point in 2024. All that said, Bloomberg are running a source story – doubtless coming from one or more of the more hawkish GC members – saying that officials are starting to accept that rate rises may have to continue through September (meaning they could hit 4% from the current 3.25%).

US equities have finished the day with the Dow little changed, the S&P500 +0.5% and the more interest rate sensitive NASDAQ +1%. IT (1.2%) and Communications Services (+1.7%) are the two S&P sectors showing gains of more than 1%, while energy is the drag, -1.2%. This is after European stock indices all ended in the red, albeit most by less than 0.5%.

In currencies, NOK is the strongest G10 performer (0.7%) and where big upside CPI surprises (headline 1.1% against 0.7% expected, underling 1.0% vs 0.8% consensus) have trumped lower oil prices. Norges Bank has already flagged another (June) rate rise but thinking now is that may not be enough. JPY benefits most from lower US Treasury yields (USD/JPY down 0.6%) while NZD (+0.5%) has again outpaced AUD (0.25%), outperforming gains of 0.2% for the EUR and virtually nothing for GBP in front of the BoE tonight..

In commodities oil is down over 1% (WTI -1.2% to $72.80) after the EIA reported an unexpected 3 million barrels lift in crude inventories last week (consensus has been for a 1.8 million barrels draw), albeit there were big falls for gasoline and distillates. Base metals and iron ore are all lower with aluminium, iron ore and steel rebar all down more than 2% and nickel more than 4%. Gold is $3.5 down despite lower US rates and a softer USD.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.