Online retail sales growth slowed in May following a fairly strong April

Insight

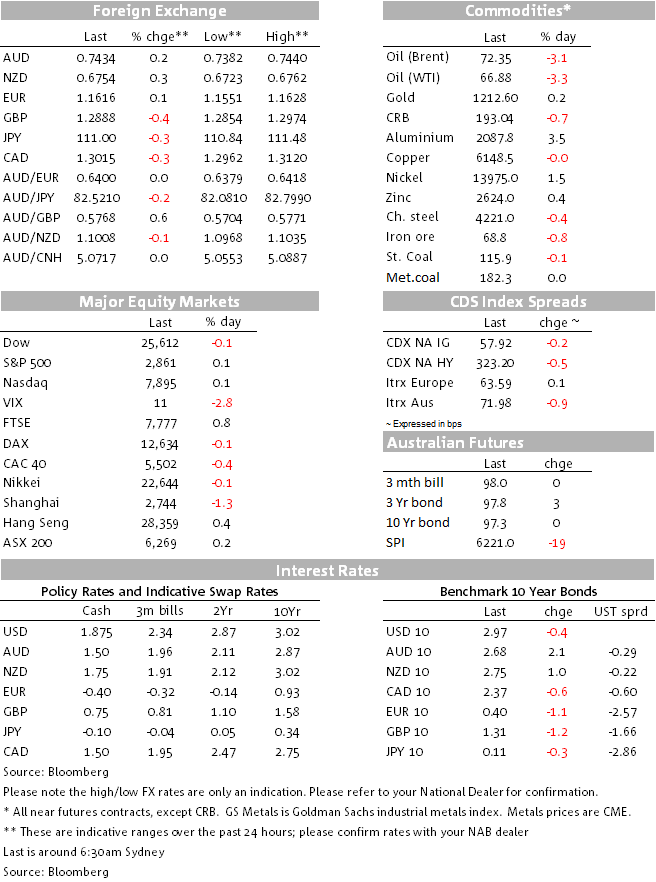

The markets are a little subdued this morning.

“And now you’re pumped, you gotta get ready for the big payback” –James Brown

After yesterday’s confirmation by the US that it will follow through with its plans to impose 25% tariff on the $16bn of Chinese exports (remainder of $50bn after initial $34bn). Overnight and as expected, China said that it will make the necessary counter measures of 25% on $16bn of US goods including US fuels amongst other products. Reaction to the news has been fairly muted with oil prices the exception, dropping over 3%. The USD is a touch lower with JPY and commodity linked currencies outperforming while GBP has remained under pressure. 10y UST yields are 1bps lower after a well-received record sized 10y auction and the RBNZ this morning left the official cash rate unchanged at 1.75%, as expected, but it sounded a bit more dovish noting recent moderation in growth could last a bit longer and pushed out it expectations for a rate hike to 2020. As we type NZD is 50pips lower at 0.6700

After trading to an overnight high of 95.406, DXY, the USD index is about 0.10% lower over the past 24hrs and currently trades at 95.097. There was little reaction in currency markets to China’s expected response to the US additional trade tariffs, looking at the intraday charts the overnight high in DXY can be largely attributed to the mover lower in GBP, dropping one big figure to 1.2855, before settling at 1.2884 where it currently trades. There was no major news driving the move lower in the pound, nevertheless the market is clearly getting more nervous over the possibility of a no-deal Brexit, which would be a messy outcome for the UK economy. News reports suggest that May is planning a top-level meeting of her cabinet ministers early in September specifically to discuss how to ready the UK for such a possible outcome.

JPY sits at the top of the leader, up 0.4% and currently trades just below the ¥111 mark, after trading down to ¥110.65 late yesterday. Yesterday the Summary of opinions from the BoJ last policy meeting showed that that one member said the 10-year yield could move upward and downward by around 0.25%. The market is sensing that the BoJ may be a bit more interested than initially thought in backing gradually away from its super easy policy. That said, we know that there are 3 hawks in the Board of 9, so the fact that one board member wanted the 10y JGB band to be 0.25% rather than 20% shouldn’t be a major surprise. The summary of opinion also showed another member said allowing a wider range may lead to an increase in real interest rates and weaken prices. Thus other more influential factors playing into JPY strength can be attributed to US China trade concerns and the inability of 10y UST yields to head back above 3%.

Somewhat surprising given the increase in US-China trade tensions and the sharp decline in oil prices, CAD and AUD are among the USD outperformers. CAD is up 0.23% and now trades at 1.3021 and AUD is at 0.7431, up 0.15% after trading down to an overnight low of 0.7387. So the AUD is now closer to the top of its 0.7311-0.7484 range held since mid-June, but given the increasing prospect of US-China trade tensions getting worse before they get better, we still think risks to the AUD remain tilted to the downside. The big test will come early in September with the US decision to impose or not additional tariffs on $200bn imported goods from China.

Yesterday RBA Governor Lowe gave a relatively upbeat assessment of the economic outlook yesterday, repeating that the likely next move in rates will be up and adding that the Bank will not wait for inflation to hit the mid- point of the target range, 2.5%, before moving. Inflation is expected to get there in 2020, suggesting 2019 is still front of mind for the Board in terms of timing for a possible rate hike. The AUD didn’t react to the speech.

One observation post RBNZ (re AUD/NZD) is the juxtaposition of RBA’s Lowe indicating yesterday that the Bank is apt to lift rates head of inflation even hitting the mid-point of the 2-3% target range, while RBNZ Governor Orr has made clear policy is expected to be on hold at least through 2019 and that higher headline inflation is to be both looked through and/or welcome.

Relative rates are only one component of the AUD/NZD equation, but with other key drivers (relative business conditions and relative commodity prices) also supportive of AUD/NZD of late, there appears scope for AUD/NZD to make further progress above 1.10

As noted above oil prices have been the big movers in commodities with both Brent and WTI down more than 3%. the escalating trade dispute between the world’s biggest economies dwarfed a decline in U.S. crude stockpiles. The move lower in prices appears to have been driven after China announced that it will levy 25 % tariffs on U.S. gasoline, diesel and other goods in response to the $16bn tariffs announced by the US yesterday.

Meanwhile aluminium had a great day jumping 3.34% helping other metals perform. Iron ore, gold and coal were little changed

The S&P 500 Index closed marginally in negative territory after a four-day advance with tech and bank shares the outperformers. The NASDAD was also little changed and European equities were mostly lower with the UK FTSE the exception, up 0.75% and probably reflecting the sharp decline in GBP.

US Treasury yields are little changed and remain within recent tight ranges. The record $26bn US 10y auction met decent demand, clearing without a tail and similar coverage (ratio of 2.55) and indirect bidding (61%) to recent sales. The yield near 3% clearly still represents value to many investors

Richmond Fed President Barkin gave his first substantial speech since becoming a voter on the FOMC. His comments seemed to be in line with the consensus, where he outlined the case for further gradual rate increases with the extent required depending on the dataflow. “It is difficult to argue that lower than normal rates are appropriate when unemployment is low and inflation is effectively at the Fed’s target”, he noted.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.