A private sector improvement to support growth

Insight

Thanksgiving week finished with a rapidly falling oil price and questions over the strength of growth in the US economy.

https://soundcloud.com/user-291029717/no-love-to-share-at-the-end-of-thanksgiving

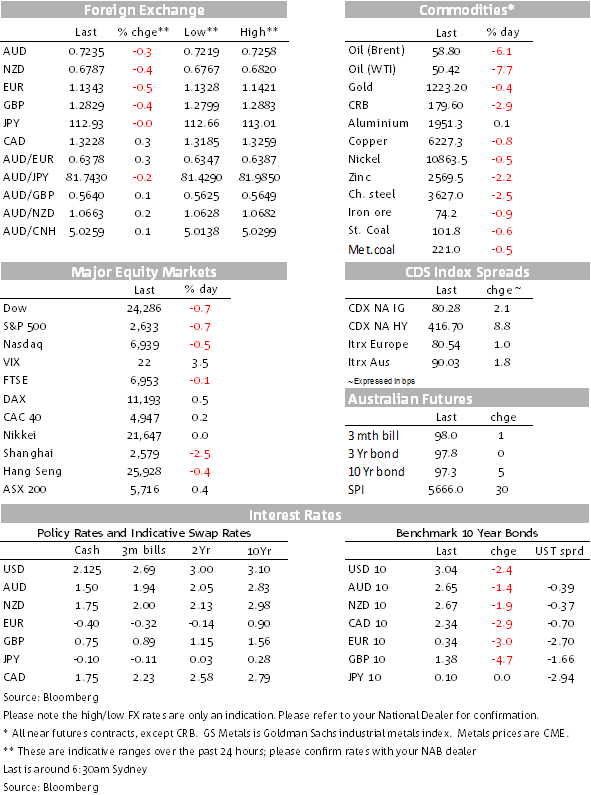

It seems that there is still plenty of life in the good old greenback. Despite concerns over the US housing sector, volatile equity markets, tighter financial conditions and a potential blink by the Fed, the US continues to win the least ugly contest with other major economies showing a greater degree of sensitivity to trade tensions and economic growth slowdown. Softer EU preliminary November PMI’s on Friday have confirmed that the current slowdown is more than just a temporary auto driven story. In November EZ Business activity grew at its weakest rate in nearly four years and worryingly leading sub-indices suggest the slowdown still has some legs. The Markit EZ report revealed a slower order book growth and falling exports were accompanied by deteriorating optimism about the outlook, as well as rising costs and prices. Speculation on whether ECB guidance could turn dovish in December is now on the rise. Meanwhile the oil slide continues with prices falling between 6% and 8%, prospects of an OPEC and friends’ production cuts have been overwhelmed by increasing global growth anxieties.

Amid softer European activity readings and sharp declines in oil prices, the USD was the outperformer on Friday erasing some of the losses incurred earlier in the week. A Brexit resolution boosting GBP and EUR is one potential negative near term USD driver and after resolving the Gibraltar objections with Spain late Saturday, overnight PM May secured EU leaders approval for the deal, now the major obstacle remains UK Parliament approval. Weekend news suggests this remains either very difficult or not possible at this stage.

The narrow DXY index gained 0.21% and ended the week just below the 97 mark at 96.94. The broader BBDX index climbed 0.39%, closing the week at 1207.5 while ADXY (-0.12%) and EM FX (0.42%) also gave back some of their recent gains. European currencies were the big losers on the day with EUR (-0.58%) closing the week at 1.1337.

Unsurprisingly amid a softer commodity backdrop, wobbly equity market and disappointing EU activity readings, the AUD (-0.29%) and NZD (0.48%) traded with a softer tone on Friday. On the week both currencies lost ground against the USD, AUD ended the week at 0.7232, leaving the pair around the middle of its 0.7164-0.7338 range held since early November. Meanwhile NZD closed the week at 0.6782, so about one big figure from the 0.6884 high reached mid-month, but still about 3 and a half big figures above the lows reached mid in October.

Oil remains the focus in commodities. News of a potential Opec and Friends production cut (see below for more) did little to stem the decline in prices ( Brent -6.07%, WTI -7.71%) with demand concerns dominating amid disappointing (EU) economic activity readings. WTI prices closed at $50.47, comfortably through the 50% retracement level of $51.47, now technical resistance for prices to trade into the high 40s looks pretty flimsy and once through, many will start pondering a move into the low $40s.

On the week oil prices are down between 10%-12%, iron ore closed 1.1% lower, but at $74.2 prices remain elevated.

UST Yields drifted lower on Friday with the 5 and 10y tenors leading the decline, flattening the curve. 10Y UST traded down to an intraday low of 3.03%, following the move lower in oil prices, before recovering somewhat to close the week at 3.04%. On the week 10y BTPS are the outperformers (-8.5bps to 3.40%) while all core yields drifted lower a few bps.

The Shanghai Comp was the big loser on Friday (-2.49%) with IT and communication sectors suffering the most. US equities closed mixed with minor gains (NASDAQ)/losses (S&P 500) amid light volumes suggesting a Thanksgiving hangover or a Friday holiday for many.

On the week, US equities were the distinct underperformers with DJ (-4.4%), NASDAQ (-4.26%) and S&P500 (-3.79%) at the bottom of the pile.

Ahead of the G20 Trump-XI meeting next weekend, Australia’s GDP partials will be of interest for the AUD, both RBA Governor Lowe and Assistant Governor Kent speak on Monday, with Kent’s speech on ‘Securitisation and the Housing Market’ likely to be of more market interest. A solid NZ Q3 retail sales report on Monday should be NZD supportive with the focus shifting to RBNZ Financial Stability Report and RBNZ speakers on Wednesday. That said, both antipodean currencies are likely to remain very sensitive to global themes, the G20 Trump-Xi meeting is now within sight and sound bites backing a temporary cease fire, should be supportive, but if the AUD and NZD are to test recent range highs, at a minimum we need to see an end to the current decline in oil prices and here the technical picture does not look encouraging.

See our What to Watch for more details

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.