Online retail sales growth slowed in May following a fairly strong April

Insight

Could Trump’s declaration of an emergency to fund his wall have consequences for the markets?

https://soundcloud.com/user-291029717/no-shutdown-just-an-emergency-and-a-holiday

Risk sentiment was kicked off Friday by the President averting another government shutdown, even if by declaring a national emergency to procure his Wall funding. He was then briefed on Saturday by his key economic and trade officials on the trade talks at his Mar-a-Lago club Florida retreat. He tweeted that “Trade negotiators have just returned from China where the meetings on Trade were very productive … In the meantime, Billions of Dollars are being paid to the United States by China in the form of Trade Tariffs!” He had said on Friday that he might keep the tariffs on Chinese goods from rising.

The two sides are working toward a “memorandum of understanding” to form the basis of an agreement between the Presidents, whenever that might be. There are more talks in Washington this week between the US trade head Lighthizer and his Chinese counterpart Vice-Premier Liu He and Lighthizer.

Trump also held out an olive branch to the Democrats, saying that “any deal I make toward the end I’m going to bring Schumer – at least offer him – and Pelosi. I’m going to say please join me on the deal,” Trump said, referring to Senate minority leader Chuck Schumer and House Speaker Nancy Pelosi. “I’ll put them in the room and let them speak up.”

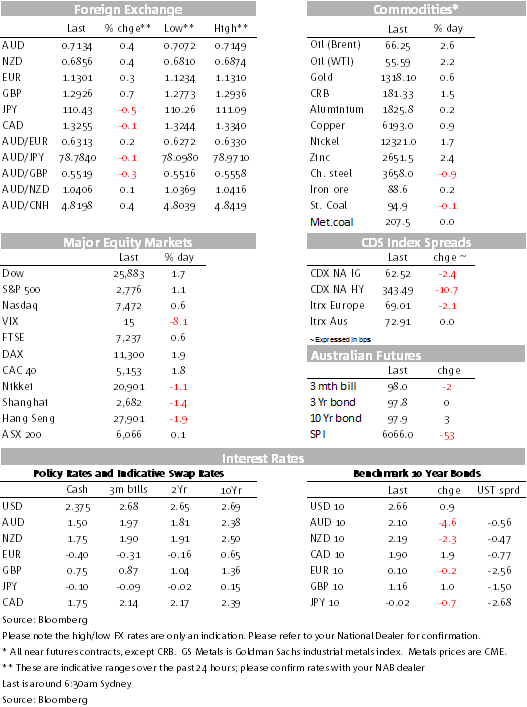

With risk sentiment back, commodity currencies outperformed alongside GBP, while US and European equities made decent gains. The AUD, NZD, and CAD all made gains of between 0.4-0.6% since late Friday APAC time. The EUR has made little to no gain since late Friday APAC time, held back by a cautious outlook from the ECB’s Villeroy and Coeure.

Meanwhile, the slowdown in global trade and global growth momentum caught up with Hong Kong’s economic growth down at the end of last year, with exports showing almost “zero growth” and GDP slowing to “less than 1.5 percent,” according to a blog post on Sunday from Financial Secretary Paul Chan, short of Q3’s 2.9%.

From a European perspective, cautious comments from ECB members Villeroy and Coeure weighed on the EUR. Banque de France Governor Villeroy said the slowdown of the European economy is “significant” and the ECB could change its rates guidance if it becomes clear the situation isn’t temporary. In an interview in the Spanish press, he said that “the key question will be if the slowdown is temporary — with a bounce-back during this year — or more durable”.

Spill-over from the softened-up European economy into ECB policy was also mentioned by ECB Board member Coeure, saying Friday the ECB is discussing whether to offer new longer-term loans to banks.

Data out of the US on Friday showed weaker than expected industrial production in January (-0.6%; consensus +0.1%), the Empire State Manufacturing survey for Feb at 8.8, up from 3.9, while the UoM Consumer Sentiment index in the first survey for Feb showed a post-shutdown revival of sorts to 95.5 from 91.2, though the 5-10y inflation expectations pulled back to 2.3% from 2.6%, an equal lowest reading since the 1990s, giving the Fed even more comfort on continuing moderate US inflation.

UK Retail Sales for January were much stronger than expected, up 1.2%, though whether this represented any more than concerted efforts from retailers to beef up sales and discounting to shift stock would be a stretch against the Brexit uncertainties. Sterling lifted, helped along by risk sentiment and a stodgy USD.

China released their January money supply, new yuan loan and aggregate financing volumes report over the weekend, revealing the usual New Year reset and strong start to the year. New Yuan loan volumes jumped from ¥1080bn to 3230bn; last year it jumped from 584bn to 2900bn. We wouldn’t be reading too much into these figures from a reflationary policy viewpoint.

On the local front, weekend preliminary auction results for Sydney and Melbourne again surprised on the high side, Sydney’s at 61.0% (likely still comfortably in the 50s when revised later in the week), Melbourne’s at 54.2%. It’s a hint of more liquidity coming back to the market, it seems. Nationally, 1,442 auctions were held, up from 928 last week but well down on the 1,992 held in the same week last year.

The Fairfax Ipsos poll taken in the wake of ramped-up border protection and offshore detention policies saw Labor’s lead narrow to 51/49 from 54/46 in the previous December poll.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.