Total spending grew 0.9% in June.

It's been a quiet session overnight. Oil rallied as supply fears rose on Trump’s sanctions imposed on the country this week, but it has since retreated.

https://soundcloud.com/user-291029717/oil-choppy-over-venezuela-trump-doubtful-on-north-korea-outcome

There have been no major economic releases and the news has been more of another instalment of recent themes. China trade tension news was risk-supportive, China announcing a cut from July 1 of car tariffs from 25% to 15% and some car parts to 6%. Germany and then the US are the largest beneficiaries of this announcement, then the UK (Europe larger than the US) helping to lift sentiment in European stocks generally, the DAX up 0.71% with Volkswagen and BMW stock both rising by over 2% and Daimler (Mercedes of course) up close to 1½%. US stocks did open higher but were unable to sustain the move, the Dow the heaviest among the major indexes, down 0.72%, the S&P down 0.31%, and the Nasdaq down 0.21%.

Also in the geopolitical sphere, President Trump has cast doubt on whether the June 12 summit will take place. “There’s a chance, a very substantial chance it won’t work out”, he said during a meeting in his office with South Korean President Moon Jae-in. “I don’t want to waste a lot of time and I’m sure he doesn’t want to waste a lot of time,” he said of Kim. “So there’s a very substantial chance it won’t work out and that’s OK. That doesn’t mean it won’t work out over a period of time.”

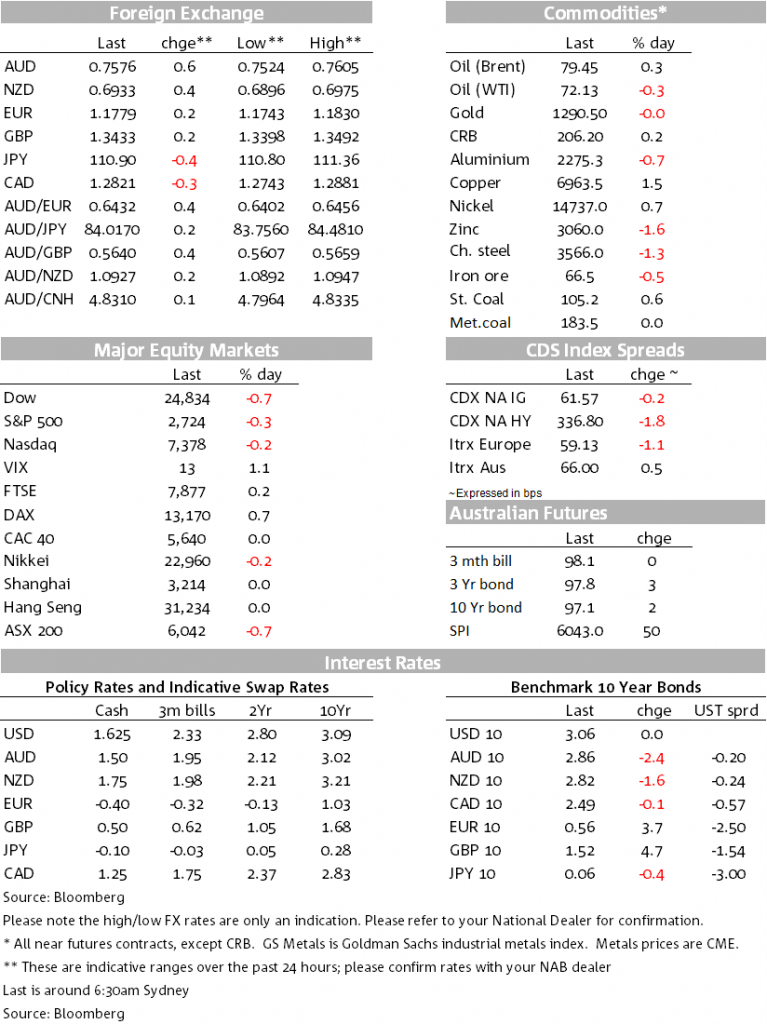

On the currency front, the commodity currencies were bid higher for a time, the AUD/USD initially testing above 0.76 earlier in the session before relenting to below the figure where it sets this morning, lifted perhaps initially be the backwash from a higher bid for Santos for Harbour Energy, rejected by Santos. AUD/NZD trades this morning at around 1.093 after having initially tested higher levels while AUD/CAD has made some net gains over the past 24 hours. Oil has changed little over the past 24 hours notwithstanding the sanctions pressure on Venezuela and the background pressure on Iran from the US Administration. The LMEX was up 0.58% with copper up a solid 1.45% to $6,979/t, other metals mixed (Ally and Zinc down, Nickel up).

There’s also been something pf a saw-tooth pattern in the Pound with the appearance of several BoE/MPC members appearing before a select Parliamentary Committee. MPC member Vlieghe’s view was that rates were likely to rise 1-2 times per year for the next few years, giving the Pound some initial support that faded, BoE Governor Carney and MPC member Saunders with more temperate view, Carney suggesting a more gradual approach along the lines of the recent BoE Inflation Report that suggested one per year, a view we agree with for this year anyway, next year open to Brexit developments.

The Italian political leadership situation remains in a state of flux with Italian President Mattarella taking more time to consider the credentials of the candidate for the top job of Prime Minister (law professor Giuseppe Conte) and Eurosceptic Savonna as the candidate for the key Finance post, nominations from the League/Five Star coalition. (There was also some questioning from the New York Times over Conte’s CV, coalition rejecting that as “mud slinging”.) The Italian press is reporting that a decision is expected perhaps tonight. Italian bonds however managed to claw back a little territory, down 6.1bps for the session, though are still 59bps higher so far this month, including against German Bunds. Italian credit default swaps though did not manage to pull back and sits at a seven month high of 139, up a little further on the day and up from as low as 84 in late April. US Treasuries have been rather range bound with little in the way of new moves.

In late news, diary giant Fonterra has just announced a strong opening forecast for the new 2018/19 NZ milk season at $7. Our BNZ colleagues thought a range of $6.50 to $7.00 was possible based on current pricing and currency levels, so it’s at the top end of that. Kiwi is not so far showing too much of a response.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.