Online retail sales growth slowed in May following a fairly strong April

Insight

The continuing rise in oil prices and rising bond yields in the US – where they have tipped the 3% yield mark again.

https://soundcloud.com/user-291029717/oil-rises-on-uncertainty-us-and-oil-rises-on-unrest-us-and-european-yields-boosted

It’s been an overnight night absent of key releases where a further lift in oil prices seems to have had the largest identifiable role in bond and equity markets. The USD has regained a measure of support, though it’s been at the margin rather than specific US factors. Even the Euro struggled for support despite what should have been Euro yields supportive comments from an ECB Governing Council member, even if not Draghi.

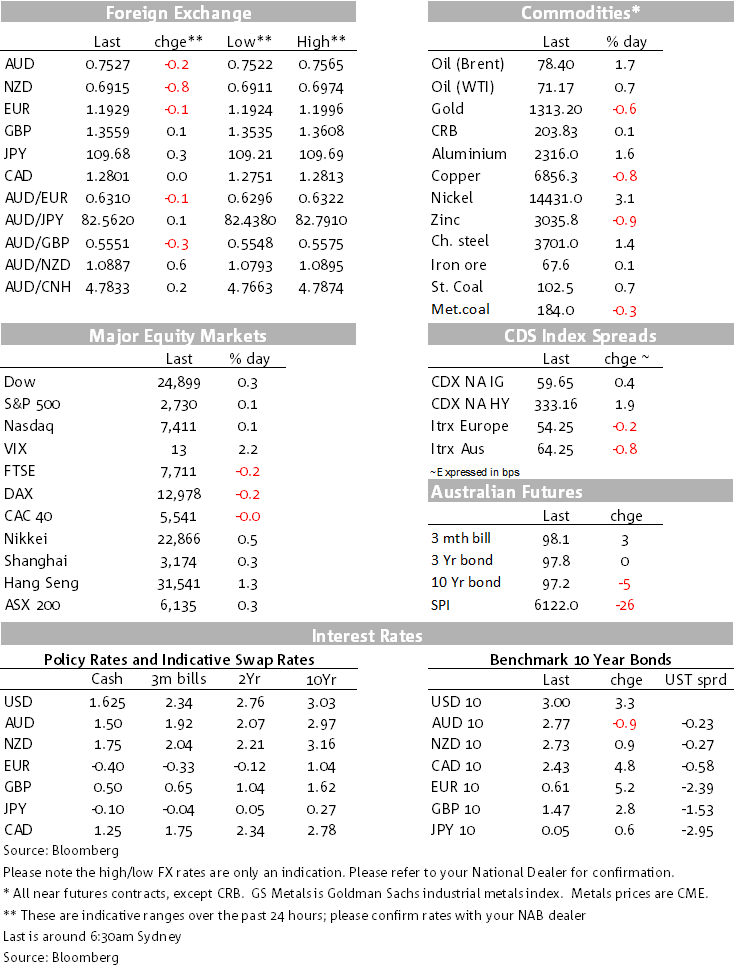

With the US embassy slated to open in Jerusalem today, it’s been unrest on Gaza border strip that has seen dozens of Palestinian deaths as tens of thousands converged to protest, a stark contrast to the celebratory scenes at the embassy’s opening. This unrest news saw further support for the oil price, coming on top of the renewed US sanctions on Iran. Brent is up over 1½% on the day to over $78 d with the price of Brent (and the Brent-WTI premium front end contract premium) rising to the highest levels seen since 2014 when oil prices were on the way down from over $100/bbl.

Bond yields were first supported in Europe and the US, the German 10y up 5.2bps to 0.611% and the US 10s tipping over 3.00% again in the afternoon US session. US equities have made small net gains (0.1%-0.3%) with energy (and health) stocks the standout.

The USD has been steady to a little higher, the Bloomberg spot dollar index up 0.2% with the AUD back to 0.7527 this morning amid a slight rise in the VIX (but still with a 12 handle, just), small net gains on the LME (nickel the stand out) and supportive major resource commodity prices, including by extension from its oil price link, LNG.

Among central bank speakers, it was the remarks from the Banque de France Governor and ECB Governing Council member Villeroy that attracted market attention, adding to bond price headwinds. He noted that the current inflation slowdown is clearly temporary and that the first rate hike could come after a few quarters following the end of the Asset Purchase Program, not years: “The time when our net asset purchases will end is approaching — and as I already said, whether it will be in September or in December is not a deep existential question.” “As far as the first rate hike is concerned, we could give additional guidance on its timing — ‘well past’ meaning at least some quarters but not years — and it’s contingency on the inflation outlook.”

Also speaking at the same Banque de France Conference, the Fed’s Mester (voter) also gave her usually hawkish bias on the outlook for rates, noting the Fed may have to raise rates above 3% and that the short-term equilibrium interest rate is rising on the back of “fiscal policy turning from restrictive to stimulative, the economy growing above trend, and investment rising”.

Trade tension talk has also been getting a further run. There was Trump’s Twitter announcement over the weekend that he had instructed the Commerce Department to help out China’s large telecoms firm ZTE – the first major concession in the trade negotiations. Media reported yesterday that China would reciprocate, with Chinese regulators restarting their review of Qualcomm’s takeover. Meanwhile, the WSJ reported that China would remove tariffs on some US agricultural products in exchange for Trump’s U-turn on ZTE. Vice Premier Liu He, a key economic advisor to President Xi, will visit the US this week to continue the talks. Adding to the uncertainty, US Commerce Secretary Ross has been talking up trade tensions on the wires, saying that the US market is the most open and exploited market in the world and that ZTE had done some inappropriate things and raising the possibility of alternative sanctions. Clearly, it’s all still very much a work in progress.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.