Online retail sales growth slowed in May following a fairly strong April

Insight

Could oil reach $100 a barrel? And why have US treasury yields leapt forward overnight?

https://soundcloud.com/user-291029717/oilmaggedon-and-the-great-treasuries-sell-off

Work it Make It Do it Make us Harder Better Faster Stronger – Daft Punk

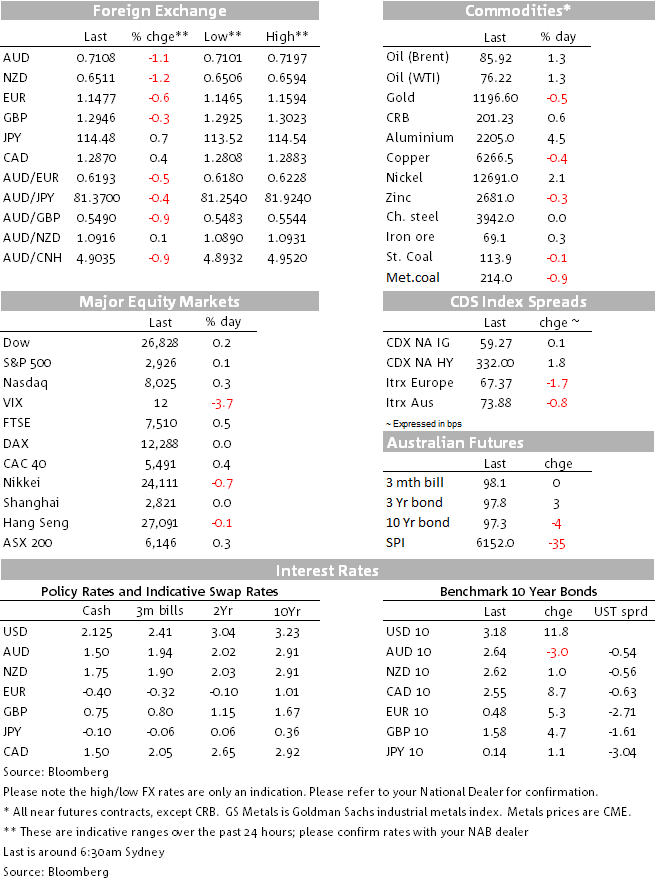

Solid US data releases triggered a sharp selloff in US Treasury yields with the 10y rate climbing to its highest level in 7 years while the 30 year tenor ascended above 3.30% for the first time in four years. Both the ISM non-manufacturing and ADP employment print beat expectations reinforcing the perception the US economy is currently firing on all cylinders and as a result US equities have had a positive day unperturbed by the move higher in yields. The USD is also stronger across the board with AUD and NZD the big losers within G10, both down more than 1% and again reflecting their sensitivity to EM fortunes.

The move higher in US Treasury yields is the major highlight from the overnight price action with the move triggered by a jump in the September ISM Non-manufacturing print to a new cycle high of 61.6 and the second highest in the history of the series. The employment component of the report rose sharply as well, to its highest level since the survey’s inception in 1997 (see details below). Separately, the ADP employment report beat expectations as well and helped raise expectations for tomorrow night’s payrolls report. The Bloomberg consensus is for a 181k increase in US jobs last month, but the very strong employment components of both ISM surveys and the ADP surprise will undoubtedly see those payrolls estimates revised higher (the ISM non-manufacturing employment index would point to a job gain of over 300k).

The break above the 3.12% May 2018 high in the 10y rate means that current levels are the highest since early July 2011. Back then 10y UST yields were on a downtrend after peaking at 3.73% in February of that year. Notably too, the 30y tenor now trades above 3.30% for the first time in four years, yesterday the long bond closed at 3.2175% and since 2015 moves into the low 3.20% have preceded decent downward corrections. Solid data releases, higher oil prices and a technical backdrop that suggests there are not a lot obstacles for yields to continue to push higher will have many wondering how far this new push higher can go.

Often solid US data releases tend to have a bigger impact in the front end of the UST curve, this time however the move has been led by the back end of the curve with the 2y10y curve now trading at 30.6bps. Late in August the curve traded down to 18bps sparking concerns of recession signals, so the recent steepening in the US yield curve is an encouraging sign.

Fed rate hike expectations were bolstered by the data surprises, with the market nudging up the probability of a December hike to near 80%, and moving to price slightly more than two full hikes for the 2019 calendar year. Early in the session Chicago Fed President Charles Evans, who has, until recently, been one of the most dovish voices on the committee over recent years noted that “getting policy up to a slightly restrictive setting — 3, 3.25 percent — would be consistent with the strong economy and good inflation that we are looking at.” The market prices the Fed funds rate to top out close to 3% in the first half of 2020.

Also speaking over the past hour, Fed Chari Powel said the current combination of low inflation and low unemployment is “not too good to be true,” and that the pleasant pairing could continue for some time. In a slightly hawkish remark the Fed Chair also noted that “Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral,” he added. “We may go past neutral, but we’re a long way from neutral at this point, probably.”

The US Treasury move reverberated around other global bond markets, with UK 10 year gilts and German bund yields up 5bps. The move higher in German yields was aided by an easing in concerns around Italy (more below) and some associated unwind of safe-haven buying.

Solid US data releases and higher UST yields have helped the USD performed across the board. In index terms the DXY index is up 0.58%, ADXY is -0.23% and BBDXY is +0.44%. AUD and NZD are the big underperformers within G10, both down over 1%, AUD now trades at 0.7108 and the year to date low of 0.7085 looks too close for comfort. Meanwhile NZD is at 0.6513 with the year to date low of 0.6501 also well within site.

Looking at DM markets, main equity indices ( US and Europe) have had a good night and the commodity complex is mostly above water suggesting risk sentiment should be supportive for both the AUD and NZD. Unfortunately as it has been the case this year, both currencies have displayed a high degree of sensitivity to the EM fortunes, so in an environment of higher US Treasury yields, higher oil prices (see more below), it is difficult to see EM having a good time and consequently both the AUD and NZD are likely to remain under pressure, even though from a fundamental basis both look undervalued.

The Euro has also come under significant pressure in the past hour with the break below key support level at 1.15, triggering a swift move to 1.1478 as we type. Early in the session good news on Italy turned out to be only a small reprieve. Prime Minister Conte announced that the coalition government had decided to cut its fiscal deficit targets for 2020 and 2021 to 2.1% and 1.8% respectively (lower than the 2.4% previously announced). The coalition was sticking with its deficit target of 2.4% for the 2019 fiscal year. While history would suggest that a lot can change in Italian politics over a three year horizon, so the later year fiscal targets should be taken with a grain of salt, the coalition’s decision to make the fiscal adjustments suggest its sensitive to market pressure and the moves should help calm market nerves in the near-term. Italian 2 year yields fell 27bps on the day.

After trading down to a low of ¥113.60 yesterday, USD/JPY is now up to ¥114.53 and the pair is now very close to its November 2017 high of ¥114.73. Buoyant DM equity markets and higher UST yields are the major factors for the move higher in USD/JPY and from a technical perspective a move above ¥115 will have many pondering a whether the pair can revisit the early 2017 highs of ¥118.60.

US equities closed higher with the S&P 500 almost breaking a new record high intraday. Looking at sector performance the move higher in yields boosted financial shares with sector up over 1% while rate sensitive sector such as utilities and real-estate under performed. Early in the session most European major equity indices also closed with positive returns.

Brent and WTI climbed over 1% overnight, but aluminium was the big performer up over 4% following news that Norsk Hydro ASA will temporarily close the Alunorte alumina refinery in Brazil because the only area it can use for waste processing is already close to reaching its capacity. Metal prices also had a positive day and copper gained 0.64%. Met coal and lead underperformed.

ISM Non-manufacturing for September was much stronger than expected at 61.6 against expectations of 58.0 (58.5 previously). Driving the acceleration this month was a sharp rise in Employment to a new series high (+5.7 to 62.4) and a rise in Business Activity (+4.5 to 65.2). Today’s rise takes the Index to a new cycle high and is the second highest in the history of the series.

The US ADP private sector payrolls print for September came at +230k well above the +184k expected by consensus

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.