Long-term signal vs. Short-term noise

Insight

Bond markets are a little feisty ahead of the FOMC meeting tomorrow. NAB’s Taylor Nugent says a hold is still expected tomorrow but there are more signs that inflation isn’t beaten yet.

Events round-up

CAD CPI NSA MoM August: 0.4% vs fcst 0.2%, previous 0.6%

CAD CPI YoY August: 4.0% vs fcst 3.8%, previous 3.3%

CAD CPI Core- Trim YoY% August: 3.9% vs fcst 3.7%, previous 3.6%

CAD CPI Core- Median YoY% August: 4.1% vs fcst 3.7%, previous 3.7%

US Housing Starts August: 1283k vs fcst 1439k, previous 1452k (revised from 1447k)

US Building Permits August: 1543k vs fcst 1440k, previous 1442k (revised from 1443k)

EC CPI MoM/YoY August F: 0.5% (5.2%) vs fcst 0.6% (5.3%), previous 0.6% (5.3%)

EC CPI Core YoY August F: 5.3% vs fcst 5.3%, previous 5.3%

US 20y bond auction: bid/cover 2.74 from 2.56, indirect bids 65.4% from 68.4%.

Good Morning

“Tomorrow we’ll discover

What our God in Heaven has in store

One more dawn

One more day

One day more” – Les Miserables Cast

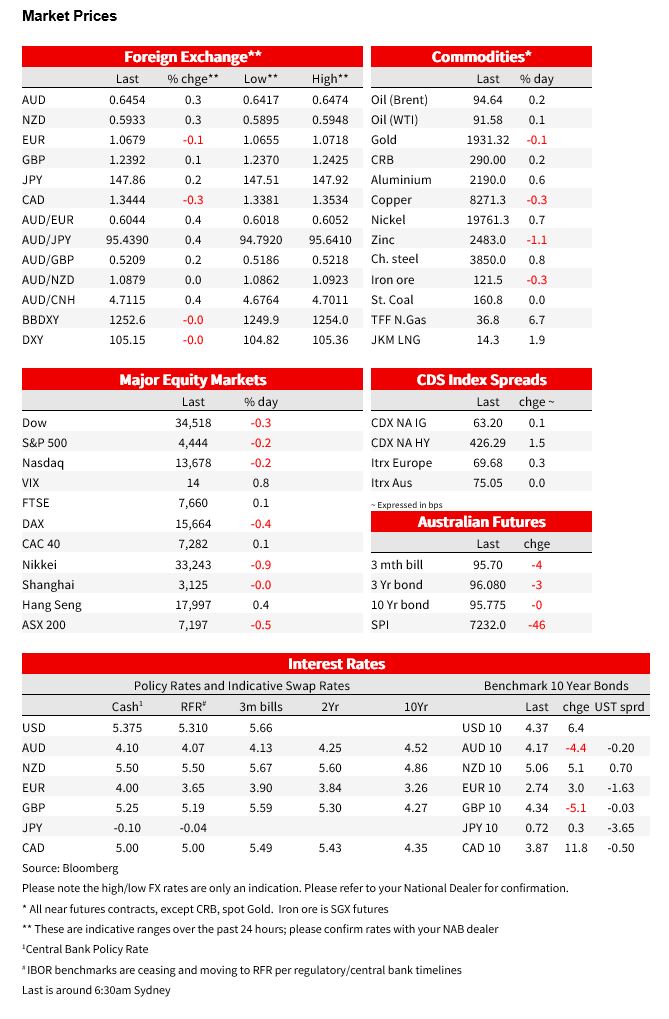

US yields are higher and equities a little lower ahead of the FOMC tomorrow, with surprisingly strong Canadian CPI data supporting the rise in yields. The US 10yr is 6bp higher to 4.365%, ever so slightly above its August high to a new post-2007 high. The S&P500 pared earlier losses to be 0.2% lower over the day and moves in currency markets have been generally modest. The US dollar is down less than 0.1% on the DXY while the AUD, alongside other commodity currencies, is 0.3% higher. Elsewhere, US housing starts were soft even as permits rose.

Canadian inflation rose to 4.0% y/y from 3.3% y/y in July, faster than the 3.8% y/y expected. The y/y rate has accelerated form 2.8% y/y in June as base effect tailwinds have rolled off and fuel prices rose. Excluding gasoline, CPI was flat at 4.1% y/y in August. The average of the trimmed mean and weighted median core rate was 4% y/y, from and upwardly revised 3.75% and above expectations for 3.7% y/y. In 3m annualised terms, a measure referenced by the BoC, it quickened a percentage point to 4.5%. In a speech released later in the day, Deputy Governor Kozicki made the point that swings in headline inflation aren’t unusual, but that underlying inflation remains above a level consistent with the Bank of Canada achieving its target. At the same time, she noted that monetary policy was working, with excess demand easing, and there were risks in both doing too much and doing too little. Following the data, market pricing for the BoC moved to price about a 50/50 chance of a hike in October, from a 25% chance prior to the data, and a full hike by January. Canadian 2yr yields rose 14bp to 4.91%, its highest level since 2001, while the 10yr gained 12bp.

Hotter Canadian inflation also supported US yields. The US 10yr rose 4bp following the data to within a whisker of its August high before another push higher in yield over the past couple of hours sees the US 10yr yield around 5.365%, up 6bp over the day to eke a new post-2007 high. US 2yr yields were 4bp higher to 5.09% while 10yr bund yields were around 3bp higher. The significant exception to the bond selloff has been the UK. 10Y Gilt yields are nearly 5bp lower ahead of the BoE tomorrow where the consensus 25bp hike is 80% priced.

In currency markets, commodity currencies are generally outperformers. The AUD, CAD, NOK and NZD are at the top of the G10 leaderboard. Though gains have generally been modest. Each of those 4 currencies is 0.3% higher against the USD. The dollar is down less than 0.1% on the DXY and was 0.1% higher against the EUR and JPY. The AUD traded up to an intraday high of 0.6474 alongside a generally weaker dollar intraday, with those gains pared to currently sit around 0.6454. USD/CAD fell below 1.34 after the strong CPI, but it has since risen back to 1.3440.

Equities are lower, though have pared losses in the US afternoon. The S&P500 is down 0.2% on the day, after being down around 0.8% at one point intraday. The Nasdaq was also down 0.2% after paring earlier losses, the turnaround led by gains in megacaps including Apple and Meta. 9 of 11 sectors in the S&P500 showed declines, led by energy and consumer discretionary. Brent Oil prices topped US$95 for the first time since November but are now back to $94.64 and up just 0.2% on the day.

US housing data was mixed . August starts fell by a sharp 11.3%m/m to their lowest level since Jun 2020. The decline was led by a 26% fall in apartments. Mortgage rates are higher and commercial credit conditions for apartment lending are tighter, and the plunge in apartments follows a milder downtrend in recent months. But the abrupt fall in starts contrasts the signal from August permits, which were stronger, up 6.9% m/m. In addition, the west of the country was the most obvious weak spot, so there is every chance weather was a factor in delaying starts in August.

The OECD released their interim economic outlook titled, appropriately, ‘Confronting inflation and low growth.’ (see OECD). They note “monetary policy becoming increasingly visible and a weaker-than-expected recovery in China” and conclude that “ Monetary policy needs to remain restrictive until there are clear signs that underlying inflationary pressures are durably lowered” which is “likely to limit scope for any policy rate reductions until well into 2024 in most advanced economies”

The RBA’s September Minutes came and went with little to trouble markets, overall suggesting little reassessment from the state of play at the August meeting. There was a marginal re-centring of the outlook, with the guidance now that “some further tightening may be required should inflation prove more persistent than expected” and that the “ recent flow of data was consistent with inflation returning to target within a reasonable timeframe while the cash rate remained at its present level.” That underscores that an upside surprise is needed in the run of inflation data to see them act on their tightening bias. A ‘more uncertain’ China outlook was included as a consideration for monetary policy, as it was in the post-meeting statement.

Since the Minutes, Q2 GDP was a little stronger than the RBA had pencilled in, and the August employment rebound did its part to keep the focus on how inflation is evolving through Q3.

August Monthly CPI next week and the full Q3 CPI on 25 October ahead of the November meeting will test whether inflation pressures have moderated as much as they hope. Markets price essentially nothing for October, and about a 50% chance of a hike by year end.

Coming Up

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.