We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Markets revert to trade focus as China announces specific tariff rises on $60bn goods should the US $200bn threat come into force.

https://soundcloud.com/user-291029717/china-steps-in-to-stop-currency-slide-the-aussie-impact

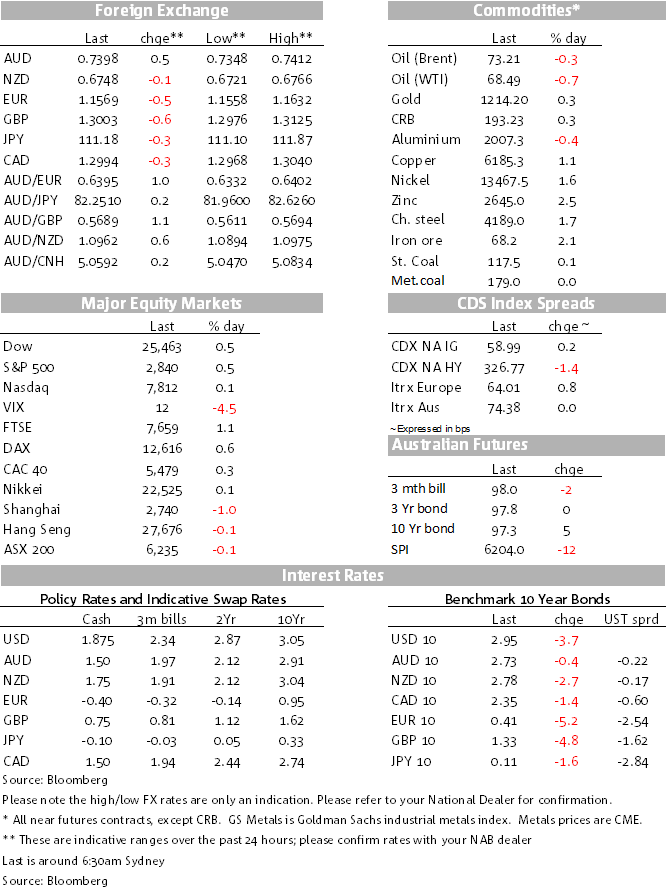

The initial focus Friday was payrolls and it was an all-too familiar theme. A still solid reflection of the overall job market – as the market is continuing to see from the likes of higher frequency jobless claims – but no pick up in the rate of earnings. Payrolls missed consensus, rising 157K in July (consensus +193K) but revisions added 59K. Moreover the unemployment rate dipped back down to 3.9% from 4.0% (it was 3.8% in May), with the broader U6 underemployment rate down to 7.5%, the lowest rate in this cycle and the lowest for nearly two decades. Average hourly earnings growth was rock steady at 2.7% y/y. This was in line with expectations, but saw a bid tone for Treasuries, yields easing by 3 bps to 2.95% by the close.

Also released on Friday was the US ISM Non-manufacturing index for July and that missed expectations, coming in at 55.7, down from 59.1, still strong in terms of growth if the lowest level for a year, a softer sign of growth into the second half. The Atlanta Fed’s GDPNow estimate is still pegged at 4.4% for Q3, though it was wound back from 5.0% after Friday’s releases.

With those two releases out of the way, it was back to the tariff and trade wars for the market. After signalling a threat of $200bn (but without product and timing specifics), China’s State Council released a list of 5,207 products totalling $60b of US goods to be hit with tariffs ranging from 5% to 25%. The implementation though would be “subject to the actions of the US”. (China imports from the US are $154bn; US imports from China are $505bn.)

Within hours, Trump’s economic adviser Kudlow promised Trump wouldn’t back down until China changed its trade practices. In a TV interview he said “Don’t underestimate President Trump’s determination to follow through”. And through the weekend, Trump has tweeted about the virtues of imposing tariffs and how well the recent tariffs imposed have worked so far. Over the weekend, China’s top diplomat Yi Wang described the measures as necessary and legitimate.

On Friday, the CNY had weakened to its lowest level in nearly 15 months, with USD/CNY up through 6.89. But a few hours later the PBoC raised the reserve requirement on FX forwards trading to 20%, a signal that it was getting uncomfortable with speculators seeing the currency as a one-way bet, the increased reserve requirement making it more expensive to bet against the currency. It was not surprising then that the AUD recovered back up through 0.74 (around where it sits this morning), seeing AUD/NZD back up to 1.0964.

The announcement triggered an immediate appreciation of the yuan, seeing USD/CNY end the week just under the 6.83 level. Barring new announcements on the tariff and trade front – a possibility that the market is alert to – this is likely to limit the downside of the Aussie for now, ahead of the RBA tomorrow, a speech from Lowe on Wednesday and also Chinese trade figures on Wednesday, the next set of known event risks.

The other major currency development of note on Friday was the under-performance of the Pound that was the weakest performing currency at the end of last week. Sterling fell to within sight of 1.30 and AUD/GBP rose to just under 57 pence.

BoE Governor Mark Carney warned that Britain faced an “uncomfortably high” risk of a “no deal” Brexit, which he said would lead to higher prices. But what caught attention was what one commentator described as a “doomsday scenario”, saying the banks had “done the stockpiling” and could survive a recession that meant property prices falling by a third, rates jumping four percentage points and unemployment up to 9%! The comments were made just after PM May was having talks with President Macron over Brexit, political and press reaction coming thick and fast in addition to the fall in the Pound. Eurosceptic MP Jacob Rees-Mogg described him as having long been the “high priest of fear” for his “inaccurate and politically-motivated forecasting” that “has damaged the reputation of the Bank of England”.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.