Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

A first Brexit milestone could mean a volatile 24 hours or so for Sterling.

https://soundcloud.com/user-291029717/pound-soars-as-brexit-draft-deal-done-now-for-the-politics

I feel so close to you right now, And there’s no stopping us right now – Calvin Harris

Following her dancing lesson on Saturday, my daughter is one of Calvin Harris new fans and thanks to Spotify we went through his top hits over the weekend. If PM May is a fan, no doubt she would be singing “I feel so close to you right now..” GBP is the top G10 performer following news that the UK and EU have agreed on a provisional Brexit deal, but there are still lots of hurdles to overcome, UK Cabinet members now need to decide to back the deal or resign. Positive US-China sound bites have continued, but they have not been enough to lift US equities back into positive territory, the huge slump in oil prices weighing heavily on the energy sector. UST Yields are lower with the 5y tenor leading the declines, AUD has retained most yesterday’s US-China news gains and Italy is said to stick with its deficit plan ahead of the EU deadline.

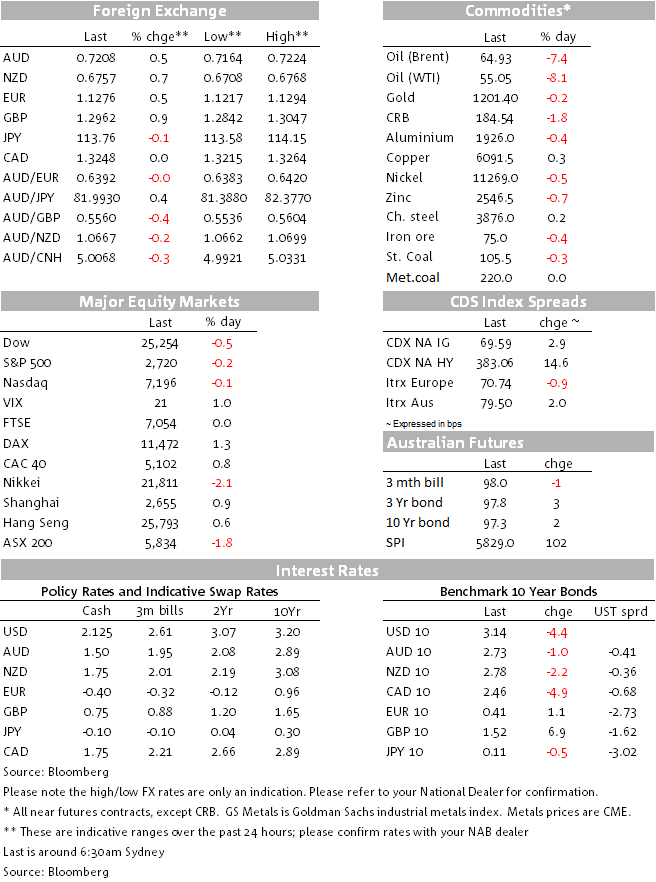

The British pound is the best G10 performer over the past 24 hours following news that the UK and EU governments have agreed on a draft divorce deal. Following three consecutive days of decline, GBP has pared some of its recent losses gaining 0.83% over the past 24hrs and after trading to an overnight high of 1.3047, the pair now trades at 1.2954. UK Ministers have now been invited to read the agreement and the PM is meeting with all her top ministers individually ahead of a Cabinet meeting on Wednesday at 2 p.m. So although the news are positive, there is no certainty the Cabinet will approve the deal. Many ministers have reservations believing PM May could be giving too much away in a betrayal of the referendum in 2016. Plus the Irish border remains a thorn and it is not yet clear what the provisional deal is proposing in this regard. As PM May said recently we are now at the “Endgame” and the first hurdle is to get the deal approved by Cabinet, this could take a couple of days of negotiations and the EU is also likely to be involved assuming the PM is forced to make some concessions with her Cabinet. Failure to pass the deal will raise the prospects of a disorderly Brexit, a general election and also a second referendum. By the end of the week with some certainty GBP won’t be trading near current levels, it could be significantly higher or massively lower.

Early this morning , Italian government confirmed that it plans to keep its deficit and growth targets effectively challenging the European Commission with an offcial reply due by the end of Tuesday (European time). The euro traded higher during the overnight session boosted by the Brexit news above, but in the pass hour the pair has traded sideways following the Italian headlines. After breaking below 1.13, the euro looks vulnerable to the downside and from technical perspective a break below 1.1250 would open the door to an easy passage towards 1.10. Hard to say which way the pair is going to swing, but Brexit and Italian news are going to be pivotal this week. Lurking on the sidelines we could also get some news on US auto tariffs on EU cars, the US administration has been making some noise of an imminent announcement looking to increase the pressure on the EU to make a deal, so a perfect storm could be looming for the euro.

As noted in previous dailies, USD indices are effectively trading on the opposite side to UK and EU political news. If the Euro and the pound go up, then USD indices are likely to be down. So based on overnight news DXY is down 0.14% to 97.218 and BBDX is off 0.21% to 1211. The slight improvement in risk sentiment sees USD/JPY as the only USD pair recording some gains. After trading to and overnight high of ¥114.13, USD/JPY now trades at ¥113.77, still reflecting a bit of cautioners in the air.

In a similar vein, the AUD trades just above 72c, retaining most of the gains from yesterday’s news that that China’s Vice Premier Liu was expected to visit Washington shortly, while he had also spoken to Treasury Secretary Mnuchin at the end of last week. Overnight Trump’s Economic Advisor Kudlow confirmed that contact has resumed “at all levels”, there’s no certainty that China will cede to U.S. demands in trade negotiations, but “it’s better to talk than to not talk,” Kudlow said in an interview on CNBC. Kudlow added that he won’t make a prediction on the outcome of discussions.

So although an improvement US-China relationship is positive for the AUD, the pair remains unable to move back above 73c, reflecting the high degree of market uncertainty at the moment. From a technical perspective AUD remains confined to its recent 0.7021 to 0.7302 range with offshore events the big determinants. That said wage data today (see more below) could bring back a domestic focus ahead of the labour market report tomorrow.

US equities rebounded at the open after the positive US-China news, but those gains were not sustained with the energy sector coming under pressure following a huge decline in oil prices (more below). The S&P 500 now trades at -0.27% and NASDAQ is -0.14%. Early in Europe, Stoxx Europe 600 Index rose for the first time in three days, with telecom firms leading the way after Vodafone Group Plc’s results.

UST 5 years have led a decline in UST yields with the tenor falling 5.6 bps to 2.98%. The move lower in oil prices one big driver for the move, 10y UST now trade at 3.136%, 4.6bps lower relative to yesterday’s levels. 10y UK Gilts are up 6.9bps to 1.52% and 10y Bunds are 1bps higher at 0.4099%

Oil prices slump more than 6% amid ongoing concern over an ease in demand and still suffering from yesterday’s Trump tweet. The move lower also appears to have been exacerbated by a break of key technical levels. WTI now trades at $55.09 and Brent is at $64.99. Moves in other commodities have been relatively subdued with copper down -0.16%, iron ore -0.39% and gold -0.16%.

UK wages data came in hot with Earnings ex-bonus at 3.2% 3m y/y against expectations of 3.1%. The annual growth rate is now the highest since October 2008 and it’s worth noting here that wages are starting to accelerate in the lower-skilled industries – perhaps indicating labour shortages – “wholesaling, retailing, hotels & restaurants” wages were +4.4% y/y. Other components were largely as expected, employment of 23k (25k expected) and unemployment ticked one-tenth higher to 4.1% from 4.0%. With Brexit uncertainty hard to see the BoE reacting to the data, but in the event of a deal it could cause the BoE to become more aggressive given strong wages growth.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.