Coming in for landing in a heavy cross wind

Insight

Fed Chair Jay Powell’s comments at the Economic Club in Washington supports risk sentiment.

| I reckon Jack Johnson’s “Sitting Waiting Wishing” must have been at the top of Fed Chair Jay Powell’s playlist this week. Certainly that’s the sentiment expressed in his latest utterances, where he told the Economic Club in Washington overnight that, “You should anticipate that we’re going to be patient, and watching, and waiting, and seeing”, reiterating his soothing comments made at the end of last week that have helped support risk sentiment. As for “wishing”, Powell noted that the current Fed median (‘dot’) projections are conditioned on a very strong 2019 outlook.

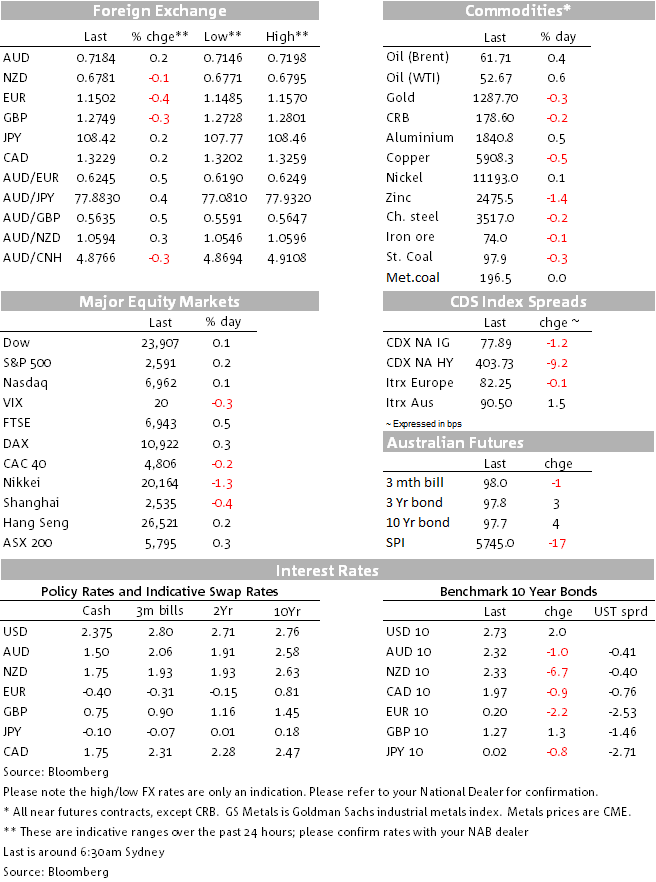

Chicago Fed president Charles Evans – of late much less dovish than the moniker traditionally ascribed to him – has just been out saying that the Fed can ‘easily’ look at the data for six months (before considering another rate hike). Feb uber-dove James Bullard meanwhile has repeated his view that he’s concerned the Fed is on the “precipice of a policy mistake” and that in his view the December rate hike was “a bit of an overreach” (in which respect we know from yesterday’s FOMC minutes that some around the table opposed a rate rise – he will have been one and, for sure, Neel Kashkari another. The net result of this week’s Fed speak together with increased optimism towards a Sino-US trade deal and other developments has been to see the US money market price out earlier thoughts of Fed easing before 2019 is out (implied odds of about 30% this time last week for the December meeting, to now an implied Fed Funds rate of 2.42% at year-end versus the current Effective rate of 2.40%). This is showing up in a slightly better performance for the US dollar in the last 24 hours and slightly higher bond yields across the US curve, while the S&P has put on just over 2% so far this week. FXThe Aussie dollar is the best performing G10 currency in the past 24 hours and only one to be up against an otherwise firmer US dollar (overnight high of 0.7198, 0.7185 now). Instrumental to the gains has been the appreciation of the Chinese Yuan yesterday afternoon and which has also dragged most of EM Asia FX up in its slipstream. USD/CNY fell from around 6.82 to 6.78 yesterday, a gain of over 0.5%. Incidentally, whether we look at our ‘alternative’ AUD fair value model that just references EM assets prices (including FX) or our traditional models utilising rates differentials, commodity prices and the VIX, both are spitting out short term value at 0.7050 this morning. Reason perhaps not to get too excited about prospects for a further rapid run higher just yet, but nor too risk of a revisit to last week’s ‘flash crash’ lows nearer 0.67. The DXY index is currently about 0.3% higher on the day, unusually large weakness in the Swiss franc (-1%) and a 0.4% drop in EUR/USD making the biggest contributions. GBP is about 0.3% lower as we head toward next week’s currently planned vote on UK PM May’s Brexit Withdrawal Agreement, with some impact from negative UK news in the form of Jaguar Land Rover announcing 4,500 jobs cuts and media headlines that “UK retailers endure worst Christmas since 2008”. Weighing on the Euro somewhat was an outsized drop in French industrial production (-2.1% against just -0.2% expected) and which comes on the heels of Wednesday’s similar sized fall in German production (-1.9%). One precondition for a sizable fall in the US dollar this year, viz a better showing by the Eurozone economy, is patently not yet falling into place, albeit both sets of numbers may have been depressed by the impact of the ‘yellow vest’ protests in France and retooling in the German auto industry. On the latter though, there is a yet no sign from German orders data this is now reversing. EquitiesWith an hour of trade still to go, US equity indices are just in the green, the S&P500 by 0.2% but the Dow and NASDAQ closer to flat. It’s a very mixed picture across sectors, industrials, utilities and real estate all up about 1% but consumer discretionaries down by 0.7% and the worse performing sector. BondsUS Treasury yields have continued to edge higher, 10s currently +2bps to 2.73% and 2s by 1bp to 2.56%. Aussie 10yr futures are 1.5 ticks down in the offshore session, so matching US moves. CommoditiesOil has continued its advance, albeit only slightly, both benchmark blends up about 25 cents heading into the NY close. Base metals are mostly weaker though, e.g. copper -0.5%, with aluminium the outlier, up by about 0.5%. Gold has been mirroring the dollar this week, hence it’s off $6 or about 0.5%. Iron ore is little changed. |

As such, markets will likely interpret any strong November Retail Sales outcome with a degree of caution – a solid result could easily be offset by a weaker December result due to these shifting seasonal spending patterns. However, if Retail Sales are weak in the month, this will likely be taken as a sign of another weak print for Consumption in Q4. Note Retail Sales are only around a third of household consumption (which makes up around 60% of GDP), and the monthly data isn’t adjusted for prices. That said we expect a relatively modest 0.2% m/m outcome (market consensus 0.3%).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.