Total spending grew 0.9% in June.

A boost for the pound and mixed data from the US.

https://soundcloud.com/user-291029717/powells-adjustments-mays-delays

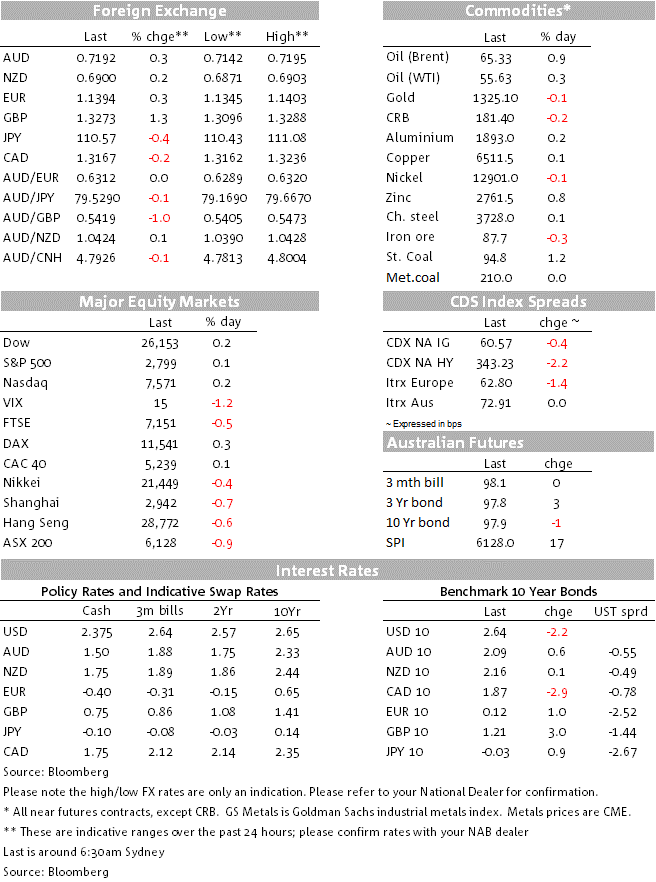

The only price action of particular note since we went home yesterday has been in GBP, which jumped by over a cent against the US dollar after UK PM May told parliament that if they rejected her Withdrawal Agreement on March 12th, they would in the subsequent days have the option of voting to leave the EU on March 29th without a deal, or vote for an extension of Article 50.

May has though only suggested that the latter should be for only a short while (no later than June). We suspect events will over-take this ‘extend and pretend’ approach by the Prime Minster than seems designed to head off the immediate threat of more Cabinet resignations. But what it means for the time being is that it is still not possible to definitely rule out a hard/no deal Brexit either on March 29th or sometime not much later. Indeed, as we write, France’s Finance Minister is out saying that if there is no clarity on the purpose of an (Article 50) extension “I don’t see the necessity of that extension”. Remember all 27 EU (ex-UK) nations need to approve any such request from Britain.

So while GBP is up on the further thinning of the March 29th hard-Brexit tail risk, AUD/GBP it has still not been able to definitely break a key support level at 0.54 (o/n low of 0.5405). We think it will, but perhaps not at least until we see what unfolds on March 12th and in the days thereafter.

Not too much else to note in FX, save that the EUR (+0.3%) has managed to catch a bid in the slipstream of the stronger GBP, confirming its current ‘low beta GBP’ characteristic, such that gains for the two currencies that together comprise over 70% of the DXY dollar index means that the latter is currently 0.4% weaker. There has also been a contribution from a stronger JPY, USD/JPY -0.4% at ¥110.59 and thus moving further back down after having rejected a test of both the 100 and 200 day moving averages on Monday.

US interest rate markets have seen yields move modestly lower, in the wake of a (mixed) set of incoming US economic data and the first day of Fed chair Jay Powell’s semi-annual Congressional testimony, before the Senate Banking Committee. Given the move to hold press conference after each FOMC meeting, we should now have learned not to expect any ground breaking insights from these affair, which will be repeated tonight in front of the House Financial Services Committee.

As our BNZ colleagues have already noted, Powell reiterated that the Fed would be “patient” with interest rates. He said the US economy remained healthy, although it faced “crosscurrents” from more volatile financial markets, slowing growth in China and Europe, and uncertainty around US-China trade negotiations and Brexit. The implicit message would appear to be that if the US and China can achieve a trade deal and global growth and markets rebound, then the Fed might again consider rate hikes.

On the more dovish side, Powell noted that people were being pulled back into the labour market, which had created more room for the US economy to grow without overheating. Powell reiterated that the inflation pressures were “muted”. US rates were little moved through the Q&A, and the market continues to price little from the Fed this year, and a rate cut by the end of 2020.

Powell also highlighted the Fed’s review of monetary policy that it is undertaking (the conclusions are expected next year). Powell said “We’re trying to think of ways of making that inflation 2 percent target highly credible, so that inflation averages around 2 percent, rather than only averaging 2 percent in good times and then averaging way less than that in bad times.”

On the economic data front, US Consumer Confidence rebounded strongly in February from the January fall, to 131.4 from 121.7, unsurprisingly given the ending of the government shutdown and subsequent rally in US stock markets, the latter historically the biggest driver of swings in consumer sentiment. The current level does though still sit below the August-November 2018 highs.

In contrast housing-related data was weak, December Housing starts slumping to 1078k from 1253k expected (-11.2%) albeit Building permits were up by 0.3%, while the S&P Case-Schiller Core Logic house price series for December shoed 20city index up 0.19% on the month (versus +4.5% expected) and seeing the annual pace of growth slip to 4.18% from 4.58% previously.

Equity markets are entering the last hour of NY trade showing small gains for the main indices (0.1-0.2%) with the IT and Telecommunications sectors showing the biggest sub-sector gains in the S&P 500. In commodities oil has enjoyed a small rebound after Monday’s big fall, Brent crude currently 56 cents or 0.86% stronger, while most base metals, as well as iron ore, are firmer (see table below).

AU Q4 Construction Work Done will be important in so far as the both the (private) residential and non-residential work done numbers feed into next week’s GDP figures. NAB expects residential work done declined 2.2% in Q4, following the 1% decline in Q3. For private engineering work, we are forecasting a 3% decline (linked to the ongoing completion of major LNG projects), more than offsetting an expected 2.5% quarterly rise in public engineering work.

Before this, NZ trade numbers are due at 8:45 AEDT (consensus -$300mn, versus BNZ’s bottom-of-the market forecast of BNZ -$936mn, latter driven by a view of much stronger import growth than the consensus).

Offshore tonight, we get the various EC confidence surveys, Canada CPI, US Advance December goods trade, US Pending Homes Sales, US Core Logic/Case-Schiller House Prices and US Factory Goods Orders. Fed Chair Jay Powell will be repeating his semi-annual testimony to Congress, this time to the House Financial services Committee.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.