Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Markets moved sharply during Jerome Powell’s press conference.

https://soundcloud.com/user-291029717/powells-tightrope-walk-on-inflation?in=user-291029717/sets/the-morning-call

In contrast to the tradition established since Jerome Powell assumed the Fed chair in 2017, it was comments in the post-meeting Powell press conference rather than the Statement itself that caused the biggest stir in markets overnight. The US dollar and Treasury yields are higher than they were post the Statement while the S&P 500 has finished a full 1% down on its post-Statement highs. This all because the Fed chair says he sees the factors that have recently held down core US inflation as “transitory”.

In leaving the Fed Funds target range unchanged at 2.25-2.50% but making what was described as a purely ‘technical’ 5bp adjustment to the Interest On Excess Reserves (IOER) the Statement language was largely unchanged, with a moderate upgrade to the description of activity and the labour market since the March meeting to “the labor market remains strong and that economic activity rose at a solid rate”, largely offset by the acknowledgement that inflation was running below target (“inflation for items other than food and energy have declined and are running below 2%”). There was no change to the Fed’s description of being “patient” in determining the course of future policy.

Markets initially slightly extended the USD sell-off and rally in US bonds markets that had followed the earlier manufacturing ISM release, which significantly undershot expectations at 52.8 from 55.3 (consensus 55.0 – and so a hat tip to our resident ISM whisperer Tapas Strickland’s call for 53.5). This was the lowest reading since October 2016 and leaves the index sitting a smidgen below its long-run average of 52.9. The decline in the month was broad based, with declines in New Orders (-5.7 to 51.7), Employment (-5.1 to 52.4) and Production (-3.5 to 52.3).

Concerns about an economic slowdown driven in part by US trade/tariff polices and with Mexico coming back onto the radar in this respect not just China, figured in the narrative accompanying the ISM report (in which respect the USMCA has not yet been ratified, and President Trump has in recent weeks been threatening to close the United States’ southern border).

In mitigation, we would note that the headline manufacturing ISM has in recent years moved in lagged response to the Import sub-index of China’s manufacturing PMI and that the latter has in the last two months rebounded from below 45 to almost 50. It therefore offers some reason to think the ISM index will improve somewhat in coming months.

Back to Powell, where the Fed chair played down the recent slowdown in core inflation, he cited the Dallas Fed Trimmed Mean Measure which has been broadly stable at around 1.9%, compared to Core-PCE inflation of 1.6%. Powell noted that the Fed “suspect that some transitory factors may be at work. Thus, our baseline view remains that with a strong job market and continued growth, inflation will return to 2% over time”. And thus the FOMC “don’t see a strong case for moving in either direction”.

Chair Powell was asked at least a half a dozen times on his views of inflation given Core-PCE inflation is running at 1.6%. While Powell downplayed below target inflation, citing transitory factors, he did note that the Fed will be watching inflation closely in the months ahead to see whether the factors weighing on inflation are indeed transitory. Those transitory factors are cited as apparel, airfares and portfolio management and investment advice services. If low inflation were to be more persistent then Powell did say the Committee would take this into account in setting policy – but was unwilling to go any further on the prospect of the Fed cutting on inflation alone or even the length of time considered to be persistent.

The other notable release overnight was the 275k gain in ADP Employment, a notoriously unreliable indicator of non-farm payrolls but hinting at upside risks to the current 190k market consensus for Friday’s release.

In bonds, US 10-year Treasuries had slipped from 2.50% to 2.475% post-ISM and then by another 2bp or so to 2.455% on the Fed Statement, seemingly helped by confirmation of the IOER cut, before swiftly rebounding to almost 2.52% during the Powell presser. We’ve ended NY trade at 2.50%, so exactly where we were before the data and the Fed. In the money market, expectations of a rate cut by the end of the year have been shaved to 82% from 106% just after the FOMC Statement.

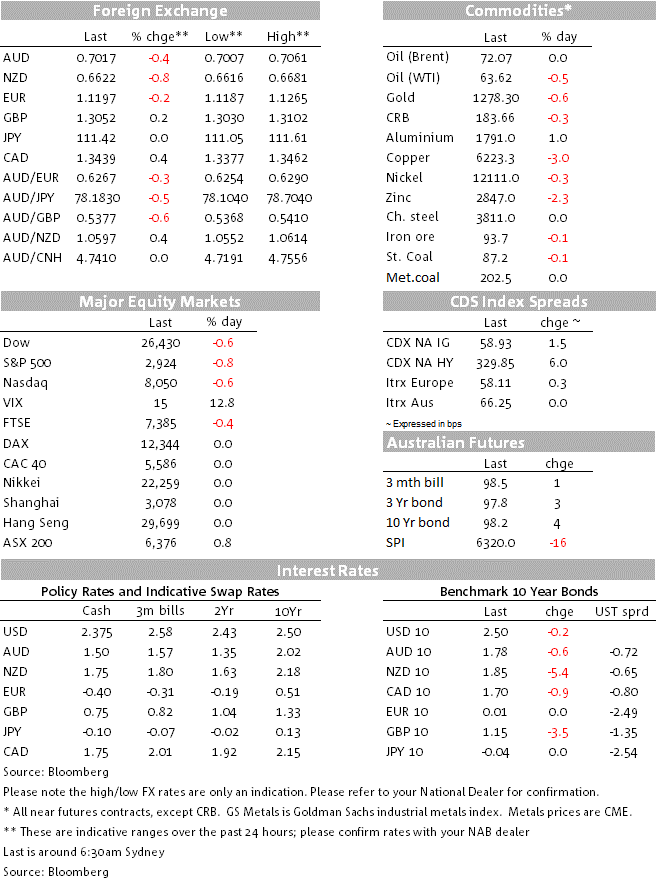

In FX, the USD in index terms rebounded by half a percent (DXY to 97.7 from 97.2) but which still leaves it about half a percent below the last week’s new current cycle highs. This has had the effect of pulling AUD/USD back down to near 0.70 (low of 0.7015) and in doing so highlighting its vulnerability to a re-test an potential break of the post-CPI low of 0.6988 were the RBA to cut rates next week. The NZD finished in New York as the worse performing G10 currency, -0.78% to around 0.6620, so extending the loses chalked up after yesterday’s Q1 labour market data where the fall in employment growth carried the day over the drop in the unemployment rate.

The CAD, also a victim of post-Fed USD strength, has come back a little above the testimony by BoC Governor Stephen Poloz in which he says that while given headwinds the policy rates now is appropriate, he does believe the economy will accelerate in the second half of the year. GBP has been the next best performing currency overnight and is up slightly against an otherwise stronger dollar, with suggestion that a Labour/Conservative Brexit agreement is not our of the question in coming days.

US Equities, earlier buoyed by a 7% jump in Apple’s shares after its strong earnings report after Tuesday’s close, fell away sharply post the Powell press conference to see the S&P 500 finish down 0.75% and the Dow and NASDAQ both by about 0.6%. Testament perhaps to just how much the recent rally has been dependent on the expectations of lower Fed rates before 2019 is out.

Nothing of note during the APAC session

In Europe this evening, France/Germany/Eurozone final April PMIs and the Bank of England. The Old Lady would probably be imparting a somewhat hawkish message given recent data, were it not for the ongoing fog of Brexit uncertainty.

The US calendar is second tier, with weekly jobless claims, Q1 Productivity and Unit Labor Costs, Factory Goods Orders

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.