Total spending grew 0.9% in June.

Not the quietest start to the week.

https://soundcloud.com/user-291029717/pump-up-the-volume-and-protect-the-borders

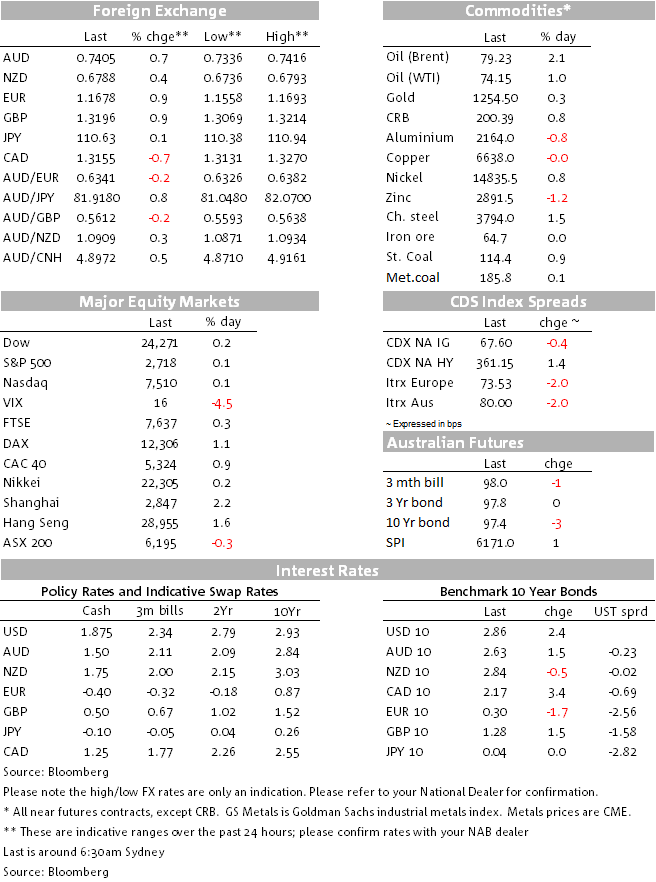

The bounce in all things EUR during Friday’s APAC session on news of European Council agreement on dealing with migration issues carried into the offshore session and proved to be a rising tide that floated all boats, in G10 currencies at least where the USD fell against everything bar JPY (-0.25%) to be 0.9% down in DXY terms. NZD again underperformed, rising by just 0.1 (versus over 0.7% for the AUD) to be the weakest G10 currency on the week by far (down over 2%).

Initially this morning, EUR/USD gave back 40% of Friday’s 1% rise, after Horst Seehofer, the chairman of the CSU (the Bavarian sister party for Angela Merkel’s CDU) came out Sunday saying that the EU’s migration plan is not in line with the party’s demands. But in the last half hour, Seehofer has quit both as interior minister and CSU party chairman, news that has seen EUR/USD fully retrace the early-day losses.

A 2% rebound in the Shanghai Composite index Friday and a small-pull back in both USD/CNH and USD/CNY from intra-day highs above 6.65 and 6.64 respectively, allowed for a small pull up in ADXY and this plus the suction from the stronger EUR saw AUD/USD lift back onto a handle (closing in NY at 0.7405).

AUD initially struggled to maintain a foothold on the 0.74 level first thing this morning, thanks both to the earlier give-back in the EUR and perhaps also in reaction to Saturday’s China PMI data, where the official manufacturing version came in at 51.5 down from 51.9 in May and just beneath the 51.6 expected. The services PMI was slightly better than expected at 55.0 up from 54.9 but the overall Composite PMI was still down 0.2 to 54.4. But the bigger influence is evidently EUR/USD, hence the jump in the latter has pulled AUD back up to (just above) Friday’s night’s highs.

We’re struggling to keep up here this morning!

US stocks underperformed relative to Shanghai and European bourses on Friday but the three main US indices just managed to close in the black, with the VIX losing three-quarters of a point to close at 16.1. This though didn’t prevent it being a universally down week, with the DAX and NASDAQ both off more than 2%, underperforming what turned out to be a loss of just 1.5% overall for the Shanghai Campsite.

In bonds, Treasury yields were fairly uniformly higher on the day (up about 2bps) in conjunction with a risk positive response to the European news and with nothing in terms of the US data flow as yet to suggest tangible negative impact from the trade concerns the Fed has been busy articulating. The 2s/10s US curve is nevertheless another 2bps or so flatter on the week.

The US core PCE deflator printed at 0.2% in line with expectations, though rounding meant that the year-on-year rise was 2.0%, above the 1.9% expected and up from 1.8% in April, so now ‘at target’. Personal Spending disappointed at 0.2% versus 0.4% expected, while the final University of Michigan consumer sentiment index slipped to 99.2 from 99.3 (probably reflecting late month equity market wobbles). In contrast the Chicago June PMI lifted to 64.1 from 62.7, well above the 60.0 expected.

In Europe earlier Friday, UK Q1 GDP was revised to 0.2% from 0.,1% – helping GBP – while June EC HICP printed at 2.0% as expected (up from 1.9%) so now also at target, though the core HICP measure slipped to 1.0% from 1.1%.

In commodities, the contrasting fortunes of oil (up) and most base metals (down) continued, with Brent adding another 2% and LMEX down 0.25% while iron ore and coal were little changed. On oil specifically, U.S. President Donald Trump on Friday might claimed he had persuaded Saudi Arabia to effectively boost oil production to its maximum capacity to cool down prices, a move that threatens to blow up a fragile truce agreed by OPEC last week and inflame the Saudi-Iran rivalry.

“Just spoke to King Salman of Saudi Arabia and explained to him that, because of the turmoil & disfunction in Iran and Venezuela, I am asking that Saudi Arabia increase oil production, maybe up to 2,000,000 barrels, to make up the difference…Prices to high! He has agreed!,” Trump tweeted. However, the state-run Saudi Press Agency reported that while the two leaders stressed the importance of maintaining oil-market stability, the agency didn’t say the leaders agreed or make any reference to 2 million barrels. Indeed, the White House is already distancing itself from Trump’s 2 million barrels claim.

A big week ahead on many levels. US trade tariffs on $34bn worth of Chinese goods are due to come into effect on Friday, US ISMs and payrolls are due. UK PM Theresa May is due to meet with her cabinet at Chequers on Friday in an effort to nut out an agreed position on Brexit. There should also be plenty of oil market volatility along the way as too movement in the Chinese Yuan, which of course has major implications for Asia EM currencies and the AUD.

Today, it’s Japan’s Q2 Tankan Survey, Caixin China manufacturing PMI (see unchanged at 51.1) UK manufacturing PMI (seen at 54.0 from 54.4) and the US manufacturing ISM survey (seen slipping to a still very strong 58.5 from 58.7). We also get latest EC unemployment data and US construction spending.

The RBA meets tomorrow.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.