Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

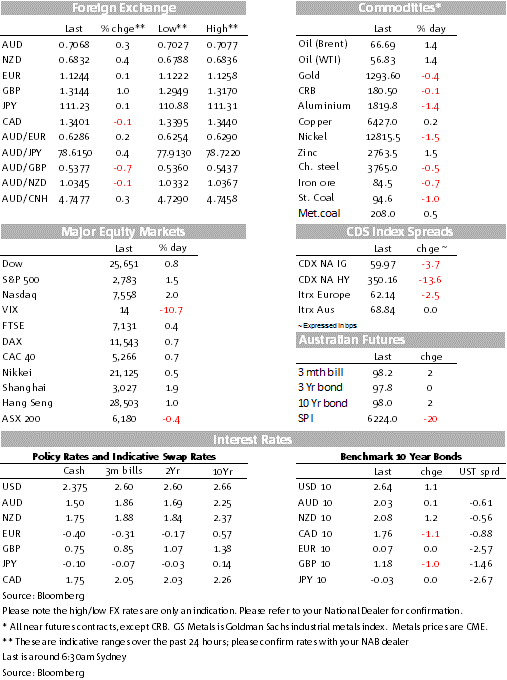

US stocks rose sharply following the release of US retail numbers which showed a bounce back in January.

https://soundcloud.com/user-291029717/risk-on-as-us-retail-sales-bounce-back-and-hopes-of-a-brexit-breakthrough

It has been a risk on night with US equities leading the gains within developed markets equities. A better than expected January US retail sales print has been one supporting factor despite downward revisions to what was already a soft December number. The USD is broadly softer with GBP the big move amid speculation PM May has secured some EU concessions ahead of her Brexit deal vote tonight. UST yields are 1bps higher along the curve and both antipodean currencies have enjoyed a small uplift given the overnight improvement in sentiment.

US equities started the week on a positive tone boosted by a better than expected January US retail sales print ahead of the opening bell. The Core Control reading came at +1.1% m/m against +0.6% expected, nevertheless the December reading was revised lower to -2.3% against an initially reported -1.7% m/m. The data suggest the Q4 GDP print is likely to revised lower and more importantly it suggest subdued US Consumption in Q1 which is likely to weigh on Q1 GDP calculations. So after a tax induced boost in 2018, the US consumer is showing signs of cautiousness in 2019.

That being said, overnight gains in US equities were led by the IT sector with the NASDAQ closing at 2.02% compared to 1.47% by the S&P 500 and 0.7% for the Dow. News that Nvidia agreed to buy a competitor boosted Semiconductors while the lag in the Dow reflected the 5.67% decline in Boeing shares following news of another 737 Max crash on Sunday.

Earlier in the session, European equities closed higher notwithstanding weaker than expected German industrial production figures for January ( -0.8% m/m against +0.5% expected).Worth noting however that Industrial Production did beat expectations for France (+1.3% m/m), Italy (+1.7% m/m) and Spain (2.4%)

The improvement in risk sentiment has seen the USD ease up a little over the course of the night with the DXY and BBDXY indices down 0.07% and 0.12% respectively. The Pound has been the big mover within G10 in what has been a pretty volatile couple of days amid conflicting Brexit news. Yesterday during our session rumours were circling around over the possibility PM May could resigned amid lack of support for her Brexit deal within her Conservative Party and no concessions from the EU. But overnight, the PM fortunes appear to have turned a corner amid speculation she may have managed to secure some concessions from the EU. Importantly as well, after some hearsay that a vote on her deal could be withdrawn, the government confirmed that the vote will go ahead tonight and it also confirmed plans for a vote on avoiding a no-deal Brexit on Wednesday and another on Thursday to decide on whether to extend the Article 50 deadline will still take place.

A few hours ago the BBC reported senior members of the Brexit-supporting European Research Group of MPs had been summoned to see the Chief Whip (although that doesn’t mean a breakthrough has been secured) and later on we also had confirmation PM May was getting on a plane to Strasbourg for last minute talks with the EU’s Juncker, a possible sign that progress had been made in the negotiations ahead of the vote in parliament tonight/early tomorrow morning.

It remains to be seen whether PM May can achieve enough concessions by the EU in order to get her deal over the line. GBP is likely to remain volatile over the next few days, that said we still have a bias for GBP to end higher mainly because we believe Parliament is opposed to a no-deal crash out Brexit which should put a floor under GBP. If PM May gets her deal through (less likely outcome) this would be very positive for the pound, but an extension and avoidance of a hard Brexit should still be good news for GBP.

After toying with a move below 70c on Friday afternoon, AUD has been enjoying a small recovery with the improvement in risk appetite the main supporting factor, AUD now trades at 0.7070, close to its overnight high of 0.7077 . Today the NAB Business survey is the domestic highlight and given the RBA focus on the labour market we will be closely watching the capacity utilisation sub index which leads the unemployment rate by around 6 months. Last month’s survey suggests unemployment could tick higher over the next six months to 5.5% from 5.0%.

In other news, President Trump released the government’s plans for a $4.7tn federal budget in 2020, including an increase in funding for the military and $8.6bn for his US-Mexico border wall. The plans have set up the stage for another battle with Democrats given they have explicitly said that they will not support more further funding for the wall.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.