Coming in for landing in a heavy cross wind

Insight

Equity markets took a hammering overnight. China felt it worst after their Golden Week holiday.

https://soundcloud.com/user-291029717/a-risky-end-to-chinas-golden-week

Welcome to the jungle, Watch it bring you to your knnn knne knees, knees – Guns N’ Roses

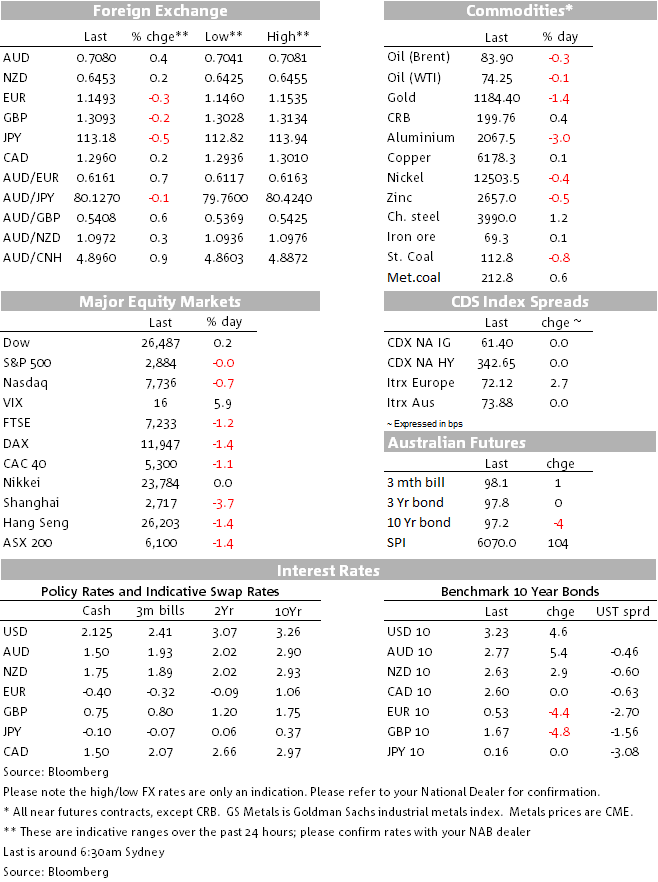

Yesterday China got a rude welcoming after its “Golden week” holiday with a sharp decline in its equity market setting the tone for markets in general at the start of the new week. A tense exchange between US Secretary of State Michael Pompeo and Chinese officials didn’t help sentiment either, Italy’s budget remains a concern in Europe and US Tech shares endured another sharp decline for a third day in a row. In spite of the risk off tone, the AUD and NZD are steady with European currencies the main underperformers against the USD.

All eyes were on the China’s re-open following its “Golden Week” holiday and Sunday’s news of a 1% across-the-board RRR cut. In the event the Shanghai and Shenzhen Composite indices fell around 3.75% on the day, and when compared to the weekly declines of 3.50% for the NASDAQ and 3.60% for the Eurostoxx 50%, one could argue that Monday’s sharp decline in Chinese equities largely reflect a catch- up to the broad decline in global equities over the past week.

Still, the sharp decline in Chinese equities during our day session yesterday set the tone for markets overnight with main European equity indices down more than 1%. A flair up in tensions between Italy’s populist government and the EU (see more below) weighted on Euroepan risk assets with the Milan stock exchange bearing the brunt of it, down 2.43%.

Tech shares led the decline in the US with the NASDAQ index down more than 1.5% at one point, before recovering into the close.

The PBoC weakened the yuan’s daily reference rate by less than expected, but the market continued to put more downward pressure on the currency since the local close. Bloomberg reported that a senior Treasury official said that the Trump administration is concerned about the Chinese Yuan’s depreciation. Treasury Secretary Mnuchin is facing pressure from the White House to name China as a currency manipulator in the semi-annual report on America’s trading partners’ currencies due later this month. This would be ironic as the US policies including trade tariffs have been the key source of downward pressure on CNY this year. USD/CNH and USD/CNY have both blasted up through the 6.93 mark, up 0.6% and 0.9% respectively for the day.

The USD is broadly stronger with European currencies the main underperformers. The Italian government has defiantly stuck to its position on next year’s fiscal budget with Deputy Prime Minister Luigi Di Maio warning that his anti-austerity view will grow stronger across the continent. Di Maio added that the 2019 EU Parliament elections will usher in new lawmakers tired of austerity and looking for a new direction.

The euro traded down to a low of 1.1460 overnight dragging other European currencies lower before recovering a bit of ground latter in the session. The pair now trades at 1.1495, down 0.25% on the day.

JPY has been the main beneficiary from the risk off tone overnight with USD/JPY briefly trading sub ¥113. After peaking at ¥114.54, the pair has been on a steady decline in past couple of days as the market’s ponders equity markets ability to cope with higher UST yields and heightened US led trade tensions.

In spite of the risk off tone the AUD and NZD have actually had a decent night, AUD now trades at 0.7081 up 0.41% over the past 24hours and after trading down to an overnight low of 0.7041. NZD is also a little bit stronger (+0.17%) with the pair now trading at 0.6453. Last week while China was on holidays both antipodean currencies got a hammering falling more than 2.5%, largely pre-empting the likely downward pressure on China’s equity markets and currency once back from holiday. So the fact that both currencies have performed overnight would suggest the market was looking for more China weakens at the start of the new week.

Yesterday US Secretary of State Pompeo was in Beijing with China’s Foreign Minister Wang Yi accusing the U.S. of damaging trust, escalating trade tension and meddling in Taiwan. Just another reminder that US-China trade tensions are now extending into geopolitics and a truce looks unlikely near term. Given this backdrop it is hard to get to optimistic on the AUD and NZD fortunes near term

Amid tensions with Europe, Italy 10-year yields rose up through the 3.5% mark for the first time since 2014, up 14bps for the day to 3.56%. The Italian 2y bond yield is up 20bps overnight and German Bunds have seen a flight-to-quality bid with the 2y closing down 3bps and 10y down 4.4bps. The US Treasury market was closed overnight, but Treasury futures are trading and show the implied 10-year rate down a few basis points.

Copper and Met coal reordered modest gains overnight, oil prices were steady and aluminium fell almost 3% following news that Norsk Hydro said it plans to restart the world’s largest alumina refinery.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.