NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The BoE is the latest to put rates on hold. But are they done? JBWere’s Sally Auld says its not safe to assume it’s over for any central bank.

UK: Bank of England Bank Rate (%), Sep: 5.25 vs. 5.50 exp.

US: Initial jobless claims (k), Sep-16: 201 vs. 225 exp.

US: Philly Fed business outlook, Sep: -13.5 vs. -1.0 exp.

US: Existing home sales (m/m%), Aug: -0.7 vs. 0.7 exp.

EC: Consumer confidence, Sep: -17.8 vs. -16.5 exp.

NZ: GDP (q/q%), Q2: 0.9 vs. 0.4 exp.

“I’m a rocket man; Rocket man, burning out his fuse up here alone; And I think it’s gonna be a long, long time; ‘Til touchdown brings me ’round again to find” Rocket Man, Elton John 1972

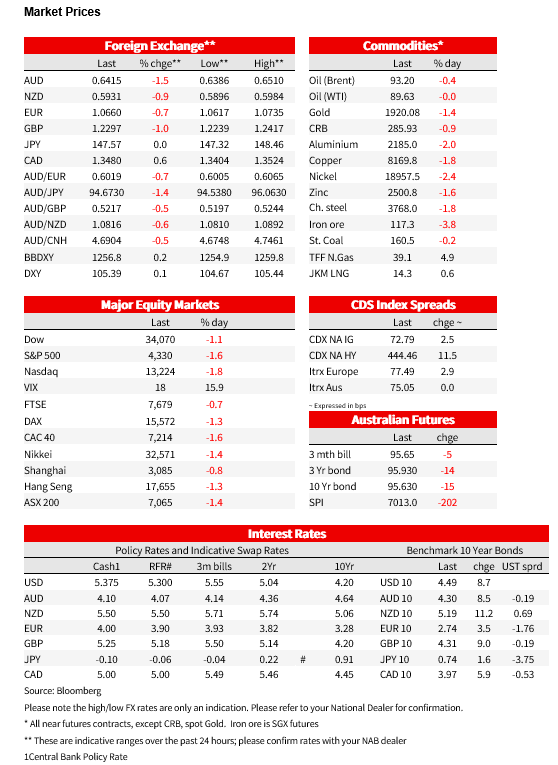

Yields continued to rocket higher post Wednesday’s FOMC with the US 10yr yield now 4.49%. The higher for longer mantra has seen curves steepen (2/10s +11bps to –65.4bps) and long-term yields hitting fresh cycle highs across several regions including the US (4.49%), Germany (2.74%), and Japan (0.74%). Equities have sold off with the S&P500 -1.6%, now trading below its 50day and 100day moving averages at 4,330. A prospective US government shutdown may also be starting to weigh on equities with GOP speaker McCarthy unable to call his own party’s defence spending bill to the floor (see Politico: House GOP erupts as McCarthy fails to move Pentagon bill). The DXY was flat overnight, but over a 24hr period it has risen 0.2% near six month highs. Data was mostly second-tier, but one big surprise was US Jobless Claims which fell back to 201k vs. 225 expected, and is now at its lowest since January. Across the pond the BoE kept rates on hold in a close 5 vs. 4 decision. BoE Governor Bailley, who cast his vote to hold rates steady, said that he won’t predict what happens next on interest rates. Market pricing is consistent with about a 70% chance of another hike by early next year.

US economic data was mostly second-tier, but importantly playing to the grain of higher for longer was Initial Jobless Claims which unexpectedly fell 20k last week to 201k vs. 225k expected and 221k previously, and back to its lowest level since January. That downward trend is defying expectations that a looser labour market would drive applications for unemployment benefits higher. Following the data the US 10-year yield trading up to 4.49%, a level not seen since 2007. Moves have been mostly reflected in TIPs with the 10yr real yield up 6.4bps to 2.11%, with implied inflation breakevens broadly steady at 2.38%. The 2-year yield is down 3bps to 5.14%, after reaching almost as high as 5.20% overnight, though is still higher than the 5.06% rate prevailing before the Fed meeting.

Meanwhile, US Existing Home Sales unexpectedly fell 0.7%, having now fallen five of the past six months and consistent with a renewed downturn in the housing market as rising mortgage rates increasingly bite. Also on the soft side of the ledger, the Philly Fed Manufacturing Index fell by much more than expected to -13.5, following its brief excursion in positive territory in August. On the positive side price indicators within the survey were in line with historical averages.

As well as the market needing to fully digest the message from the Fed yesterday, other central banks have been in the spotlight. Expectations for the BoE’s policy meeting were evenly balanced between a hike and a hold, and in the event a 5-4 vote split on the MPC resulted in leaving the policy rate at 5.25%, breaking a run of tightening at every meeting since the end of 2021. Instead of a hike, the Bank upscaled the rate of quantitative tightening from £80b to £100b per annum to accommodate a larger bond maturity profile next year. A tightening bias was maintained with the MPC repeating the message that “further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures”. BoE Governor, who cast his vote to hold rates steady, said that he won’t predict what happens next on interest rates. Market pricing is consistent with about a 70% chance of another hike by early next year.

In other central bank meetings, the Swiss National Bank defied widely-held expectations for a 25bps hike and left its policy rate unchanged, while Sweden and Norway’s central banks both hiked the expected 25bps. Brazil’s central bank cut rates by the expected 50bps, its first easing this cycle, following recent rate cuts by Poland and Chile. Emerging markets led the rate hike cycle and are now leading the rate cut cycle, giving a possible taste of what to expect for developed markets next year. Next up will be the BoJ later today, but the central bank is widely expected to do nothing, putting it further behind the curve against a backdrop of strong inflation and solid economic growth. Japan’s 10-year rate hit a ten-year high of 0.75% yesterday while the yen real effective exchange rate fell to a record low in data dating back to 1970 – this as USD/JPY almost rose to as high as 148.50, but since falling back down to 147.50.

USD dollar strength post yesterday’s Fed meeting extended after the initial jobless claims report, but after the DXY index reached a fresh six month high, it has reversed course. It has been a bit of a rollercoaster ride for both the AUD and NZD. The AUD at one point traded as low as 0.6386, before reversing to nudge above 0.64 at 0.6415. The NZD spiked higher in the wake of the positive Q2 GDP beat (0.9% q/q vs. 0.4% expected), but USD strength did see it fall below 0.59 and currently trades at 0.5931. GBP (-1.0%) and CHF (USD/CHF +0.7%) have been the weakest majors overnight following the policy decisions.

Finally in Australia, and highlighting how different Australia is on the budget front, the AFR writes the Australian Budget was in surplus for 2022-23 by $22.1bn according to the Final Budget Outcome which is set to be published today. It is widely expected another surplus will be achieved for 2023-24. A surplus of $22.1bn is the largest ever in dollar terms, thanks to surging personal and company tax payments. Incredibly, federal government net debt of about $516 billion or about 21 per cent of GDP, was already back to pre-COVID levels as a share of the economy despite the huge spending stimulus during the pandemic (see AFR: Tax bounty delivers record $22b budget surplus).

US: Fed Speak & Preliminary PMIs: Hot out of the post-FOMC blocks is Daly, Kashkari and Cook. Also out is the PMIs for the US, but they do not tend to be overly market moving

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.