Confidence and Conditions Lift

Insight

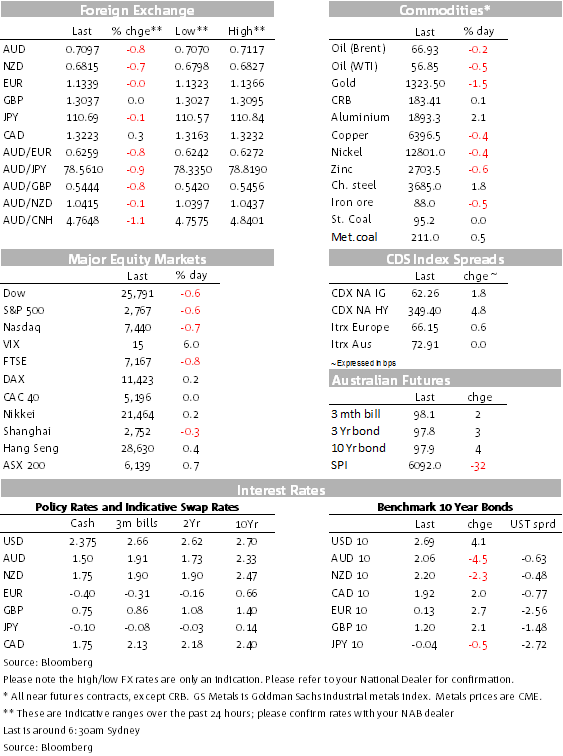

Reports China is blocking the import of Australian coal into its Dalian port hit the Aussie dollar hard with no sign of recovery just yet.

https://soundcloud.com/user-291029717/coal-blockade-pushes-aussie-down

Trade remains the central theme both in terms of news and data reports overnight, with the AUD right at the centre of attention, yesterday seeing violent moves in both directions. The AUD sits lower this morning than where it was this time yesterday. It was initially buoyed on the sticker shock from high January headline employment growth of 39K, more than double the 165K consensus. The AUD spiked higher, testing 0.72 after the number, but within the hour, an announcement from another house that they’d changed their rate call to two cuts this year took the heat out of the AUD, the AUD smartly back to pre-employment data levels.

Then, later in the afternoon, a Reuters “exclusive” report hit the wires saying that China’s Dalian port had banned Australian coal imports, setting a 2019 quota. This followed reports earlier this week that Australian coal ships have been experiencing delays in being able to unload coal this month.

This had the market understandably thinking and reacting to the idea that this was literally a “canary in the coal mine” moment as far as trade was concerned. Reuters reported a spokesman for Chinese Foreign Ministry that customs were inspecting and testing coal imports for safety and quality, ostensibly sending mixed messages. “The goals are to better safeguard the legal rights and interests of Chinese importers and to protect the environment,” Geng said, adding that the move was “completely normal”. There was another report from a Commerce Ministry spokesman who knew nothing of it.

Coal last year overtook iron ore as Australia’s number one export ($66bn cf $63bn for iron ore), though Australian coal unloaded through Dalian is only 1.8% of total coal exports to China, Dalian major port servicing local Chinese steel mills. Australia is not only number one in the global seaborne Met coal market (higher quality coal used in steel production), but the largest such supplier (<50%) to China, reliant on such product. Most Chinese coal produced is thermal, thermal an equally large component of Australian coal exports.

Interestingly, met coal prices are a dollar higher overnight, spot futures at $US211/t, thermal prices steady at $US95.20/t, seemingly not factoring in any pull-back in Chinese demand.

Travelling to NZ today for the annual Leaders’ meeting, PM Morrison will be no doubt sharing mutual economic and security concerns, further integration of the two economies and of course the dependence of both on trade with China.

The two sets of key reports overnight were the preliminary Eurozone PMIs for February (they’re usually not revised much, if at all) and in the US the Philly Fed survey for Feb, jobless claims, durable goods orders, and the Leading Index.

The Eurozone PMIs were mixed. The German Manufacturing PMI was weaker still in February to 47.6, down from an already contractionary 49.7, Services better at 55.1 up from 53. France’s Manufacturing index was up from 51.2 to 51.4, though the Zone’s Manufacturing index was weighed down by Germany’s. The German survey reported weaker orders, highlighting Asia and China in particular, including in the troubled auto sector. The French Services sector remained in contractionary territory, though at 49.8, less worse than January’s 47.8. Overall, the reports still fail to give a clean bill of health, overshadowed by trade concerns.

There was a welcome pull-back in weekly Jobless claims in the payroll survey week to 216K from last week’s higher than expected 239K, but the Philly Fed survey was particularly weak at -4, down from +17, the weakest level since 2016. Core durable goods orders in December (when equities were very brittle) again were uninspiring, down 0.7% after a 1.0% dip in November, signs of uneasy business confidence. The composite Leading was down 0.1% after being flat in December, that reading revised up from an initially reported -0.1%. That (and other indicators) are still not signalling recession.

BoC Governor Poloz was speaking overnight, saying that the path toward higher interest rates is “highly uncertain” due to lingering questions around housing and investment, even as he stuck to his message that borrowing costs eventually need to head higher. He said that “the path back to that neutral range is highly uncertain. We will watch the data as they come in, and use judgement”.

The less analysed Japanese Manufacturing PMI slipped into contractionary territory to 48.5 in February from 50.3, the lowest since 2016, likely feeling trade strains.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.