Total spending grew 0.9% in June.

The pound has fallen sharply as the currency markets opened on the news that a Brexit deal this week is looking very unlikely.

https://soundcloud.com/user-291029717/running-to-the-brexit-cliff

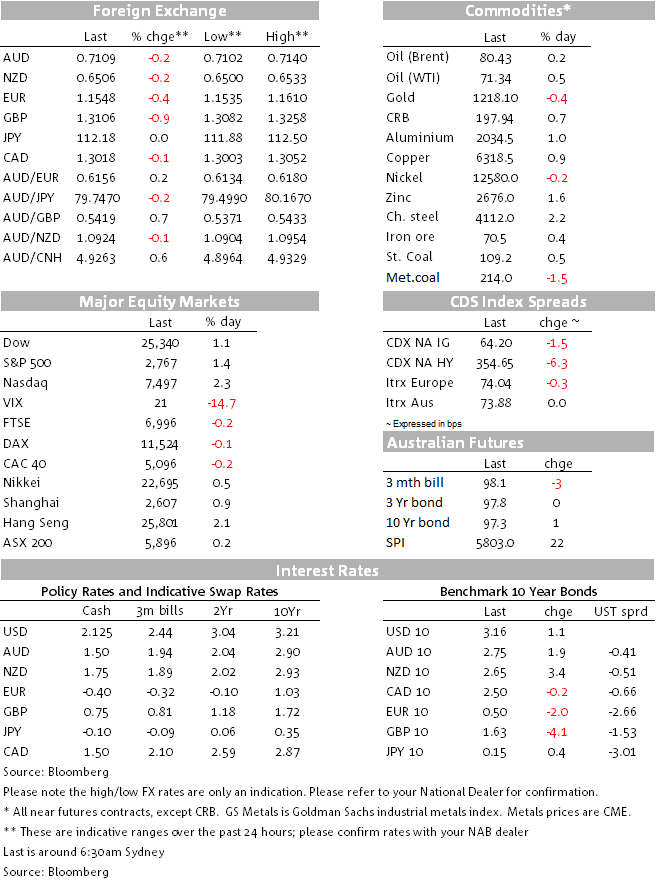

US equities rallied at the New York open on Friday, aided by JP Morgan’s’ pre-open earnings beat, but never really managed to build on opening gains. It turned out to be a ‘up, down, up’ session’ with the S&P 50 ending 1.4% higher, so recovering a little of Wednesday and Thursday’s sharp losses but to still be 4.1% lower on the week. The VIX gave back 3.7 points from its 25.0 Thursday closing level but at 21.3 remains above its long term average.

Despite JP Morgan as well as CitiiGroup beating the street consensus estimates for their Q3 earnings, the S&P 500 Financial sub-sector was one of the worst performers Friday, up just 0.1%, with the IT sector – that has led the charge lower this month – predictably leading the 1.4% rebound in the overall index with a 3.2% rally.

Shanghai turned out to be the worst performing major stock market on the week, but its 7.6% loss contained an element of catch-up to the prior week’s loses in other market’s during the Golden week holiday.

Having – unusually – failed to draw much safe-haven support during the Wed/Thu equity sell-offs, the USD was a bit firmer on Friday amid a mini-revival in risk appetite. GBP weakness was the main contributor to the 0.2% rise in the DXY along with a 0.3 fall in EUR/USD. This was amid no signs as yet of a Brexit agreement, or reconciliation between the EU and Italy on the latter’s budget ambitions and where all EU countries are this week supposed to be submitting their FY19 plans for EU Commission approval. AUD and NZD were both slightly softer, by 0.14% and 0.18% respectively.

GBP was by far the worst performing G10 currency on Frida (-0.6%) with no confirmation that a Brexit Withdrawal agreement was any closer ahead of Thursday’s EU Summit at which the hope was/is to be able to agree the outline of a UK Withdrawal Agreement to then be inked at a special EU Summit in November.

Talks on Sunday in Brussels to this end have reportedly ended with no breakthrough with the Irish border question still the sticking point. According to the UK Guardian newspaper on Saturday, Northern Ireland’s DUP is now “ready” to trigger a no-deal Brexit and which the DUP now see as the “likeliest outcome” following a “hostile and difficult” exchange with EU’s chief negotiator, an explosive set of leaked government emails reveal.

At the same time, we have reports of potential Cabinet rebellions against UK PM May’s latest proposals to extend the Brexit transition agreement beyond its currently proposed end-2020 deadline, in order to allow more time to sort out future trade relationships in a manner that would solve the Irish border conundrum.

There remains a huge amount to play for this week and Sterling will likely be significantly higher or lower than it is now by the end of the week (it has started trade Monday losing about 0.4% on top of Friday’s 0.6% drop).

In EM FX, USD/TRY fell to as low as 5.83 on news that the Turkish courts had limited US pastor Andrew Brunson’s sentence to time served, allowing for his immediate release, but there was actually something of a ‘sell the news’ response given that USD/TRY had fallen from about 6.08 to sub-5.85 in anticipation of his release. It ended in NY at 5.8732.

On the week it’s USD slippage – despite the spike in risk aversion – that stands out. JPY confirms its pre-eminent safe haven status (in particular when DM rather than EM markets are selling off) while the CHF no longer seems to have any. AUD and NZD are both the best part of 1% stronger, confirming just how much bad news looks to be already priced in and confirming their abilities go key off better EM FX performance (the global EMCI currency index rose by about 0.8% last week largely thanks to big moves up in ZAR, BRL and TRY.

Also to note is just how short speculative positioning in the AUD and NZD appears to be, at least judging from the weekly Chicago futures market positioning data (where shorts in the NZD extended to a new record extreme in the week through last Tuesday, with AUD now not too far behind). On the flip side, this market is very long US dollars.

A small–scale sell off across the Treasury curve saw yields +1bp on average, consistent with the modest recovery in risk appetite. The prior couple of weeks’ bear-steepening theme predictably gave way to bull flattening last week with the 2/10s curve about 4bps flatter.

Most industrial metals were stronger Friday, Thursday night comments suggesting a Trump-Xi meeting was possible next month offering a glimmer of (probably false) hope for an early easing of Sino-US trade frictions. Gold failed to maintain all of Thursday’s sharp, short-covering driven, gains while coking coal finally showed signs of losing a bit of its earlier invincibility to be the weakest commodity on Friday. On the week, it’s the 4% losses for both Brent and WTI crudes that stands out and which is certainly consistent with the general theme of ‘risk reduction’ across all asset markets last week, augmented by the big build in crude stock reported on Thursday:

University of Michigan preliminary consumer sentiment 99.0 (100.5E, 1001.P). 5-10 year inflation expectations were down to 2.3% from 2.5%

CoreLogic reported a preliminary all capital cities weekend auction clearance rate of 50.9% on auction volumes of 1,850 (1,817 previously) versus last weekend’s final 49.5, which visually guarantees that the final rate will be below 50% for the third week in succession. Melbourne cleared a preliminary 52.1% against a final 51.8% last weekend (preliminary was 54.4%) and Sydney 532.0% vs. a 46.1% final rate last week (preliminary was 53.6%).

A busy week is in prospect, with the fate of Brexit negotiations, US corporate earnings and at the end of the week China’s Q3 GDP and monthly September activity readings, among the highlights. In Australia, Thursday brings the latest Labour Force Survey where NAB sees the unemployment rate ticking down to 5.2% from 5.3% and Guy Debelle speaks on Wednesday. NZ has Q3 CPI on Tuesday.

Today, US retail sales tops the calendar, expected to show a 0.6% monthly rise in the headline reading and 0.4% for the various core measures, numbers which would confirm the absence of any negative impacts from trade tariffs to date and consistent with Friday’s still very buoyant reading for US consumer sentiment.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.