Online retail sales growth slowed in May following a fairly strong April

Insight

Trump’s walkout of the meeting with Kim Jong Un dominated had little interest to the markets.

https://soundcloud.com/user-291029717/mixed-data-and-high-hopes-for-china-and-brexit-deals

“You’re simply the best, better than all the rest” – Tina Turner

The working title for today’s missive when I was heading out the door last night was another Tina Turner classic, “What’s Love Got to Do with it?. This following the evident failure of The Trump-Kim bromance and the US President’s previous declaration that he had fallen in love with the North Korean dictator, to yield progress in the US’s efforts to get N. Korea to denuclearise and N. Korea’s evident desire to have US sanctions lifted. Market impact of the Summit failure was limited – and why not given the limited impact last year’s Summit and which marked the start of the Trump-Kim love affair had on global markets?

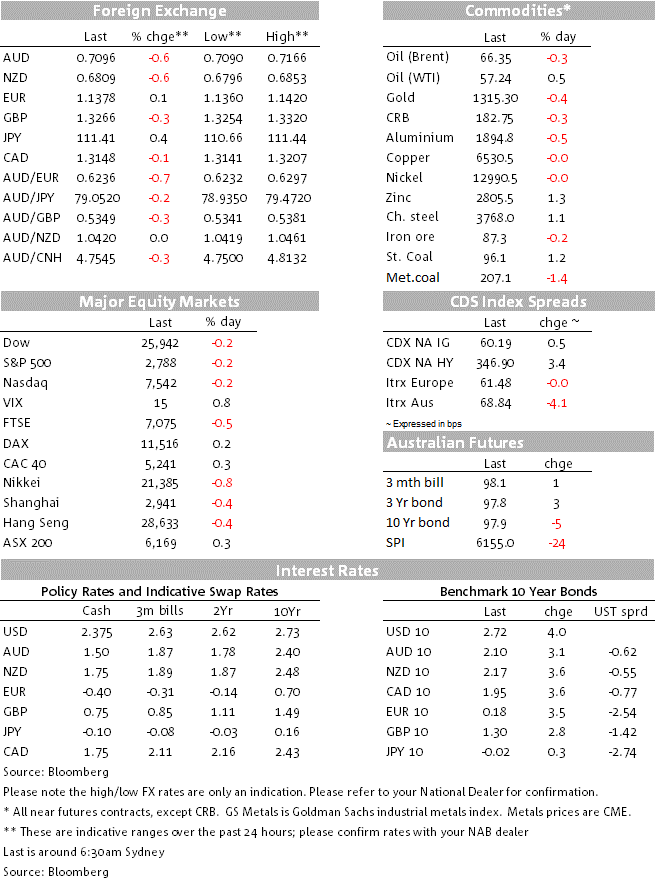

In contrast, last night’s better than expected Q4 US GDP outcome of 2.6% annualised growth couldn’t be ignored. It is almost wholly responsible for the re-strengthening in the US dollar after an earlier fall and higher US Treasury yields, averaging 2-3bps.

US stocks though are not finding much comfort in the GDP figures, the main indices currently down about 0.2% heading into the last hour of trade, weighed down in particular by weakness in the Energy and Materials sub-sectors. This is even though we aren’t seeing any extreme weakness in commodity prices, crude oil prices narrowly mixed, as too industrial metals.

Iron Ore futures however are up another $1.50 or nearly 2% (not quite sure why). It is worth a reminder here that direct read-through from iron ore prices to the AUD in our fair value model is extremely limited – almost non-existent in fact. Indeed, latest gains have evidently failed to support a USD-driven fall in AUD, to be sitting back below 0.7100 this morning (0.7096 now).

The US GDP outcome of 0.65% in Q/Q terms – 0.1% better than expected – contrasts with equivalent outcome for other major developed economies of 0.2% for both the Eurozone and UK and 0.3% for Japan, once again confirming the US as the least ugly duckling in the global growth pecking order. The breakdown shows some support from inventories (0.1%) but a 0.2% drag from net exports. In annualised terms, consumption was a respectable if relatively subdued 2.8%, business investment a strong 6.2% led by a 13.1% gain for ‘intellectual property’ while residential investment contracted by 3.5%.

The PCE deflators were 1.8% in headline terms and 1.7% for core, the latter up from 1.6% in Q3 and above the 1.6% expected, but still nothing to write home about save that it further validates the Fed’s new found ‘patient’ approach to policy.

On the latter, Dallas Fed President Robert Kaplan has just been out saying he was an advocate for the Fed’s current pause and patience (at least through June, he says) and that the inversion of the 2yr/5yr part of the US Treasury curve is a cautionary signal. Kaplan says he does not want Fed policy to invert the curve.

The other main news event worth noting overnight has been commentary from President Trump’s chief economic adviser Larry Kudlow, which has gone some way to reversing the creeping pessimism about the likelihood of a comprehensive Sino-US trade deal being ready to sign by the two countries’ Presidents later this month.

“The progress has been terrific,” Kudlow told CNBC. “We have to hear from President Xi and the Politburo of course, but I think we’re headed toward a remarkable historic deal.” The Chinese have pledged to “significantly” reduce subsidies to state-owned firms as part of a potential deal, as well as to disclose when the nation’s central bank buys and sells foreign currency, Kudlow said (though as my colleague Gavin Friend quips, “good luck with that”). China has also pledged to “de-emphasize” its plans to dominate in emerging technologies, outlined in its Made-in-China 2025 plan, he added. Kudlow cautioned that the U.S.-China accord still needs to be approved at the highest levels of the Chinese government.

In currencies it’s been a mixed last 24 hours but with AUD and NZD currently sitting at the bottom of the G10 scoreboard, both 0.6% lower at 0.7095 and 0.6809 respectively. GBP and JPY are both 0.3% lower, with no fresh Brexit related news sufficient to allow this week’s strong Sterling rally to extend and the Yen softer on higher US Treasury yields. All up the DXY dollar index is flat versus Wednesday’s NY close at 96.1, but back up from a pre-GDP data low of 95.8.

AUD was hurt yesterday by the combination of a weaker than expected reading for the Equipment, Plant and Machinery component of the Q4 Capex report ((just 0.7% against the 3% we had pencilled) and then the further falls in the official China PMIs for both manufacturing and services. USD gains have added to the pressure overnight, ahead of what will be the next big local test for the Aussie next week with the remaining GDP partials (in particular Inventories on Monday, Net Exports on Tuesday) then the RBA (Tuesday) followed by GDP itself on Wednesday. NAB is currently at 0.4% on GDP but with clear downside risk from the Business Investment side.

JN: Industrial production, Jan: -3.7 vs. -2.5 exp.

NZ: ANZ Activity Outlook, Feb: 10.5 vs. 13.6 prev.

AU: Private Capital Expend. (q/q%), Q4: 2.0 vs. 1.0 exp.

CH: Non-manufacturing PMI, Feb: 54.3 vs. 54.5 exp.

CH: Manufacturing PMI, Feb: 49.2 vs. 49.5 exp.

GE: CPI (y/y%), Feb: 1.7 vs. 1.7 exp.

US: GDP (Annualised q/q%), Q4: 2.6 vs. 2.2 exp.

US: Core PCE deflator (Ann. q/q%), Q4: 1.7 vs. 1.6 exp.

US: Chicago Purchasing Manager, Feb: 64.7 vs. 57.5 exp.

An extensive economic and events calendar Friday across all time zones. In ours, we’d highlight the Caixin version of manufacturing PMI (12:45 AEDT) following further slippage in the official version reported yesterday, to 49.2 from 49.5

Also up is NZ’s ANZ Consumer Confidence, Building Permits and the Q4 Terms of Trade

Australia has the AiG Performance of Manufacturing Index for February (last at 52.5)

Cleveland Fed President Loretta Mester is speaking on Women in Economics at 11:00 AEDT at the St. Louis Fed

Japan has February Tokyo CPI, Market, January labour market figures and the Q4 Capital Spending numbers which feed potential revisions to Q4 GDP

Offshore the main event will be the US Manufacturing ISM (expected 55.7 from 56.6). December personal income, spending and deflators are less interesting given we had Q4 data. Also final UoM Consumer Sentiment. Canada has monthly (Dec) and 2018 annual GDP

In Europe, the UK Manufacturing PMI gets top billing; also up is EZ Feb CPI, EZ January Unemployment and German January Retail Sales

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.