Online retail sales growth slowed in May following a fairly strong April

Insight

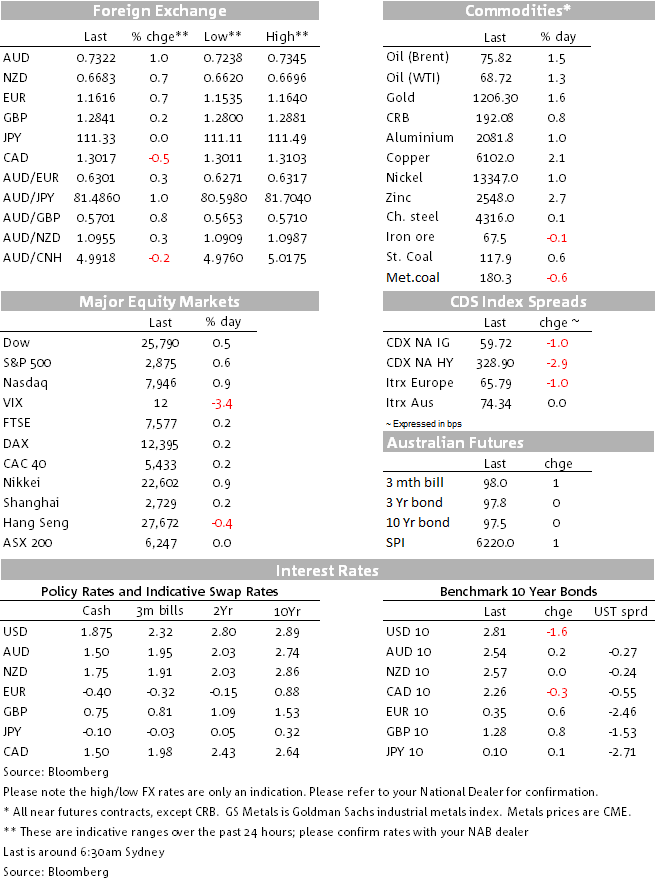

US equities hit record highs on Friday.

https://soundcloud.com/user-291029717/us-equities-like-gradual-pboc-goes-counter-cyclical-aussie-spill-wash-up

Two things moved the dials on global markets after Australian went home on Friday: Fed chair Jay Powell’s Jackson Hole speech, and a couple of hours before that, confirmation from the PBoC that it would resume using the “counter-cyclical” factor when calculating the yuan’s daily reference rate, so restraining the influence of market forces that have been driving the currency lower. The PBoC news produced a nearly nine big figure (1.4%) drop in USD/CNH and sparked an across the board decline in the USD. in the wake of the Powell speech, the US dollar then fell further, commodities rallied, intermediate and longer-dated Treasury yields fell and the S&P closed at a new all-time high.

This, plus the earlier influence of a third factor – Scott Morrison’s success in defeating Peter Dutton for the Liberal Party leadership – ensured that the AUD was the best performing G10 currency on Friday – up over 1% to 0.7329. Its gains across all major currencies were only exceeded by the South African Rand. The latter was up 1.8% so recovering most of its mid-week losses sparked by President Trump’s tweet referencing the ‘large scale killing of farmers’.

This morning’s Newspoll in The Australian showing Labor head of the Coalition by 56-44 (and Bill Shorten ahead of Scott Morrison in the ‘preferred prime minister’ stakes) threatens to undermine as little of Friday’s Morrison-win inspired AUD gains, though we’d judge that the combined impact of USD weakness post-Powell and CNY strength post the PBoC news will be the dominant – and AUD supportive – early week influences.

Fed chair Jay Powell delivered a very philosophical speech at Jackson Hole on Friday (with none of the crypticism for which one of his predecessors, Alan Greenspan was famous for, but who received a huge rap from Powell for his ‘hunch’ that the economy could grow faster than commonly thought in the 1990s without generating inflation). It was replete with references to the challenge of navigating by the ‘stars’ (*) namely pi* (the inflation objective) u* (the natural rate of unemployment) and r* (the neutral real rate of interest) in an environment where the assessment of the location of these stars have shifted significantly over time. The Fed, Powell opined, was navigating – and through ‘hazy’ skies’ – between two risks, “moving too fast and needlessly shortening the expansion, versus moving too slowly and risking a destabilizing overheating”.

“I see the current path of gradually raising interest rates as the FOMC approach to taking seriously both of these risks,” Powell said. “While inflation has recently moved up near 2 per cent, we have seen no clear sign of acceleration above 2 per cent, and there does not seem to be an elevated risk of overheating.”

It was this latter remark that market’s latched onto, interpreted as meaning that the FOMC perceives the chances of having to deviate in a hawkish direction from the current policy of gradual tightening as slim.

The US dollar was already weakening ahead of the Powell speech, the earlier PBoC announcement a significant factor here, supporting EM as well as DM currencies, then fell away more sharply after Powell’s address was seen to limit risk of an accelerated pace of Fed tightening as well as ultra-caution on the Fed’s part as and when it sees Fed Funds as close to the neutral rate.

Though oil softened post Powell, it was still up on the day as were almost all hard commodities, though the EUR still fared better than either NZD or CAD, the latter undermined somewhat by BoC Governor Poloz’s comments to CNBC in which he expressed no concern about the recent rise in inflation to 3%, stressing instead the 2% core rates. ADXY made an impressive 0.78% led by the PBoC news’ impact on CNH, while USD indices ended with losses of just over 0.5%:

On the week, the EUR has claimed top spot despite the absence of any particularly EUR-specific positive news (more a case of no bad news and the weaker USD trend) with AUD last but one in the G10 pack only spared the wooden spoon by a weaker JPY. DXY is off 1% on the week and so now 2% back from its August 15th highs near 97.

US stocks opened higher and were then propelled further on the Powell speech, SPX ending the day +0.6% and closing at a new record high of 2,865.32, as too the NASDAQ. On the week though, it was the Shanghai Composite fared best (+2.3%) and the ASX 200 the worse (1.5%).

Confidence in a continued gradual approach to Fed tightening inspired by Powell’s speech produced a bit more curve flattening, 2s 0.3bp higher to 2.62% and 10s 1.6bps lower to 2.81% – so the spread now in to a new cycle low of 19bps. On the week the 2/10s curve is in by 6.5bps, while the US spread to both 10yr Bunds and Gilts has come in by almost 10bps.

Zinc and copper were the star performers Friday (+2.7% and 1.7% respectively) while USD weakness seems to be finally offering gold a bit of support. Iron ore struggled, metallurgical coal more so. On the week it’s also coal (both types) and iron ore than are down but all else up, with the LMEX index over 3% higher, albeit still some 15% down on its June highs.

US July durable goods orders fell by 1.7% against -1.0% expected, though the less volatile orders ex transport rose by 0.2% and the even less volatile orders ex-defence ex-aircraft rise by 1.4%, above the 0.5% expected with June revised up to 0.6% from 0.2%.

CoreLogic reported a preliminary all capital cities weekend auction clearance rate of 57.9% versus last weekend’s final 53.3% with Melbourne at 58.6% versus last weekend’s final 54.0% and Sydney 59.1% versus 51.9%. Final rates should end up not far from last weekend. Auction volumes were 1,909, up on last weekend’s 1,684 but down on 2,270 in the same weekend last year.

In other weekend news US and Mexican officials are reportedly close to ending a months-long stalemate on thorny bilateral trade issues ranging from cars to agriculture to energy, which could pave the way for a broader agreement – including Canada – to renegotiate NAFTA. US President Donald Trump said the country’s relationship with Mexico was “getting closer by the hour”. “Some really good people within both the new and old government and all working closely together…a big trade agreement with Mexico could be happening soon!” Trump wrote in a tweet.

Once the US-Mexico bilateral issues get resolved, Canada will be joining the talks to work on both bilateral and our trilateral issues, Chrystia Freeland, Canada’s foreign minister, told reporters on Friday. “And we will be happy to do that”, she added. Mexico’s economy minister has just been crossing the wires saying we are in the ‘final hours’ of discussion, but suggests the need for at least another week of negotiations and that we can’t yet declare victory.

Locally, data of interest this week is Q2 Capex and Building approvals (both Thursday) and RBA credit of Friday. In NZ, August’s ANZ business survey is on Thursday and consumer confidence on Friday

Internationally, China official PMIs on Friday and US PCE inflation data on Wednesday are the highlights

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.