Online retail sales growth slowed in May following a fairly strong April

Insight

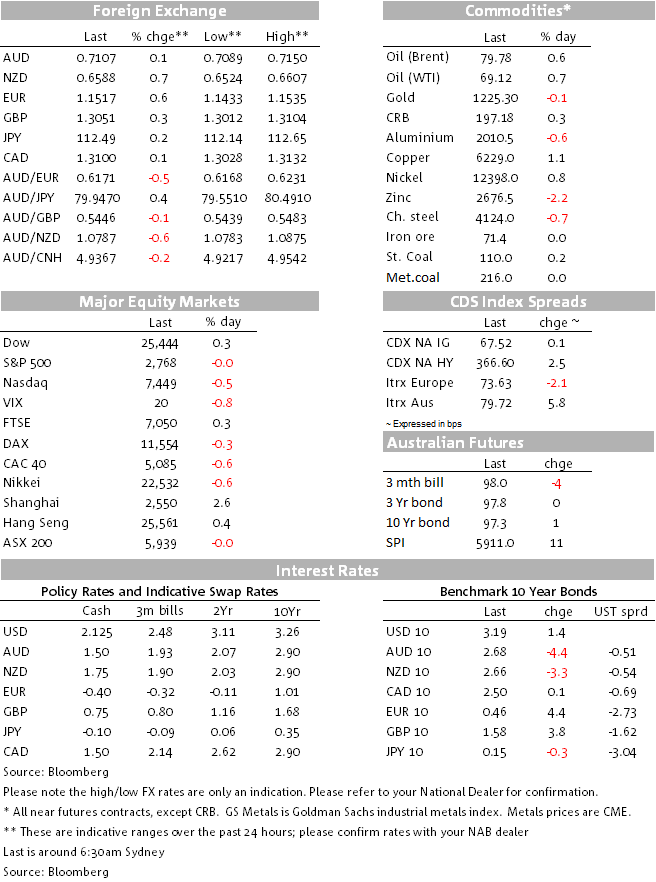

AUD (and NZD) this week look set to remain in the hands of broader USD and Emerging Market (EM) moves.

https://soundcloud.com/user-291029717/wentworth-falls-italy-stands-firm-saudis-confess-trump-cuts-loose

The Liberals’ loss of the of the blue ribbon seat of Wentworth on Saturday to Independent candidate Kerry Phelps – subject to final confirmation of course – doesn’t materially increase the chances of an early election in so far as Phelps had, going into the election (and since over the weekend) indicated her in-principle support for the government on matters of confidence and supply.

As such it hasn’t been a material market factor at this morning’s market re-open (albeit with New Zealand out for Labour Day, it hasn’t really got going yet). That said and as the ABC was noting Sunday, “it is a massive morale blow to the Coalition”. It will increase market conviction that as and when the next election does occur (no later than May 2019) it is likely to produce a change of government – as in any case was being suggested by the polls in the lead up to the Wentworth by-election.

AUD (and NZD) this week look set to remain in the hands of broader USD and Emerging Market (EM) moves amid a sparse local calendar. Broader USD moves in turn are likely to be heavily dependent on whether EUR/USD can build on Friday’s bounce (Italy’s response to last week’s EU’s ‘please explain’ letter, due Monday, will be important here, as will the EU’s subsequent reply) and whether GBP/USD extend Friday’s gains that came from news that UK PM May was considering an ‘indefinite’ stay in a Customs Union in order to break the impasse with respect to the Irish border.

AUD and especially NZD speculative positioning remains extreme (as of last Tuesday at least) and last week’s NZD and to a lesser extend AUD gains should probably be seen in this context –and meaning there should be more to come in the absence of a deeper EM/risk sell-off this week.

A mixed performance from US stocks Friday (Dow up small, S&P flat and NASDAQ -0.5%). The IT sector remained pressured, while it was defensive stocks (consumer staples, utilities) that held up the overall S&P. Honeywell’s warning – after its earnings beat street estimates – that Chinese and US tariffs were set to add ‘hundreds of millions of dollars’ to its costs, weighed on the broader IT sector (down 1.13% within the S&P 500).

Shanghai ended Friday 2.6% Friday in the wake of China’s small Q3 GDP miss (6.5% from 6.7% in Q2 and versus 6.6% expected) and mixed activity readings. Whether it was the presence of the ‘big red hand’ or confidence inspired by official comments that growth targets would be met – something which is corroborated by the acceleration in credit growth reported earlier in the week – we couldn’t say. Shanghai is still down 2.2% on the week even with Friday’s 2.6% gain. The S&P finished flat.

The DXY dollar index was 0.2% softer on Friday thanks largely to rallies in both EUR and GBP, EUR on comments from the EU’s Moscovici that it wouldn’t interfere in Italy’s economic policies and GBP on reports UK PM May was moving toward accepting indefinite participation in the Customs Union in order to solve the Irish border issue. Whether she can sell such a plan to her own parliament is a very open question of course, but GBP/USD initially jumped over half a cent on the news before gains were later pared.

The NZD fared best within G10 on Friday, not on any obvious NZ-positive news so probably more short covering amid record short speculative futures market positioning, while AUD got as high as 0.7150 in London before giving back 30 pips or so in the New York afternoon. CAD lost ground on much weaker than expected CPI, down to 2.2% from 2.8% and weaker than expected retail sales. This didn’t undermine confidence in a quarter point BoC rate hike this coming Wednesday (to 1.75%) but the implied policy rate for the March 2019 meeting date came in to 1.99% from 2.04%:

On the week the USD is up over 0.5% in index terms with NZD the only G10 currency to show any meaningful rise (+1.34%) with CPI and a very short speculative market both doubtless playing a role. Thursday’s sharp drop in the Australian unemployment rate has meant that the AUD at least finishes the week higher, albeit only marginally. EUR and GBP are both lower on the week notwithstanding Friday’s gains; CAD fared worse with lower oil and Friday’s CPI and retail sales both factors here. The ADXY Asia EM FXC index was up 0.2% Friday but virtually unchanged on the week, within which USD/CNY is very marginally higher (6.9290 from 6.9225):

Treasury yields were higher across the curve Friday but not by much, 2s up 2.9bps and 10s a lesser 1.3% in what was a slightly more risk on than off night (e.g. VIX to 19.89 from 20.06). On the week 2s are +5bps and 10s +3bps.

The bigger price/yield action was in Europe where BTPs went as high as 3.81% (highest since May 2014) and the ‘lo spread’ (to Bunds) to 341bps at one point, the widest since April 2013. The rally came on comments from European Commissioner For Economic Affairs, Pierre Moscovici, who said that the bloc wouldn’t interfere in the new government’s economic policies. Italy’s formal response to the EU’s ‘please explain’ letter sent to them last Thursday is due on Monday.

Late in the New York day, Moody’s dropped Italy’s credit ratings by one notch to Baa3 from Baa2, so to now just one notch above junk, but put the outlook at stable from negative. This was probably already in the price of BTPs. Certainly the FX market wasn’t perturbed in late NY trade, with EUR/USD actually rallying slightly, though the market was effectively shut by the time the news came out (about 4.30pm NY time). Note S&P is due to pontificate on Italy by Friday next week, where at a minimum it seems likely to shift the outlook on its BBB rating (two notches above junk) to negative from stable.

A mixed performance for commodities Friday, with copper faring best and zinc the worse. Strong indications from China Friday that it is doing whatever it takes to protect growth in the face of trade tariffs may have helped (China demand was also mentioned in dispatches as behind the firming in oil prices). On the week, it’s metallurgical coal and coking coal that have again done well, as too steaming coal and gold. On the latter, Friday’s CFTC data shows speculative positioning flipping from a net short of 38,175 to a net long of 17,667. As our gold trader tells me, the speculative market never stays short gold for very long. Oil and all exchange traded base metals down on the week:

Atlanta Fed President Raphael Bostic said on Friday. Asked about the risks to the U.S. economic outlook at a community group lunch in Macon, Georgia, Bostic mentioned geopolitical risks generally, the Brexit talks and “the Saudi Arabian situation and the question about whether what happened to that journalist is going to lead to sanctions that could impact oil markets.”

China Sep house prices (out Saturday) 0.9% m/m, 7.9% y/y (vs. 1.4%/7.0% in August)

US Sep existing home sales -3.4% to 5.15mn saar (5.29mn or 09.9% expected, 5.33mn P)

Canada September CPI 2.2% (2.7%E, 2.8%P). 16% fall in air transport line fares (reversing a prior jump) the biggest contributor to the unexpected drop, along with traveller accommodation, autos, gasoline and travel tours.

Average of three core Canada CPI measures 2.0% from 2.1% in August

Canada August retail sales -0.1% (0.3%E, 0.2%P revised from 0.3%)

Retail sales ex-autos -0.4% (0.1%E, 0.8%P revised from 0.9%).

CoreLogic reported a preliminary all capital cities weekend auction clearance rate of 49.8%, the first sub-50% preliminary rate after three weeks of sub-50% final rates. Last week’s final was 47.0% and this week’s will probably be below that. Auction volumes were 2,199 up from 1,851 – a seasonal norm. Melbourne cleared a preliminary 47.5% against a final 50.4% (51.8% preliminary) and Sydney 52.2% versus a final 45.1% (preliminary was 52.0%).

Geopolitics looks like dominating the news flow this week and what that does to risk sentiment and oil prices will obvious be important for markets, most obviously regarding the international outrage over Jamal Khashoggi’s killing and now the US decision to pull out of the 1987 Intermediate Nuclear Forces Treaty ahead of a visit to Moscow by Josh Bolton, President Trump’s hawkish national security adviser.

It’s a quiet start calendar wise, the only thing of note today being ‘remarks’ by RBA Deputy Governor Buy Debelle in Sydney at midday, at the Walkley business journalism awards.

Globally, US earnings season continues and we get Q3 GDP on Friday (and where the Atlanta Fed’s latest ‘GDPNow’ estimates stands at 3.9%). The Bank of Canada meets Wednesday and should lift rates by 25bps and the ECB on Thursday where Draghi’s post meeting press conference will be of interest. EZ flash PMIs on Wednesday are of note and then on Friday Standard & Poor’s will pass judgement on Italy’s (currently BBB) credit rating.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.