On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

The US has imposed extra tariffs on Chinese imports. Gavin Friend discusses the market reaction.

https://soundcloud.com/user-291029717/stocks-and-oil-tumble-on-trade-turmoil

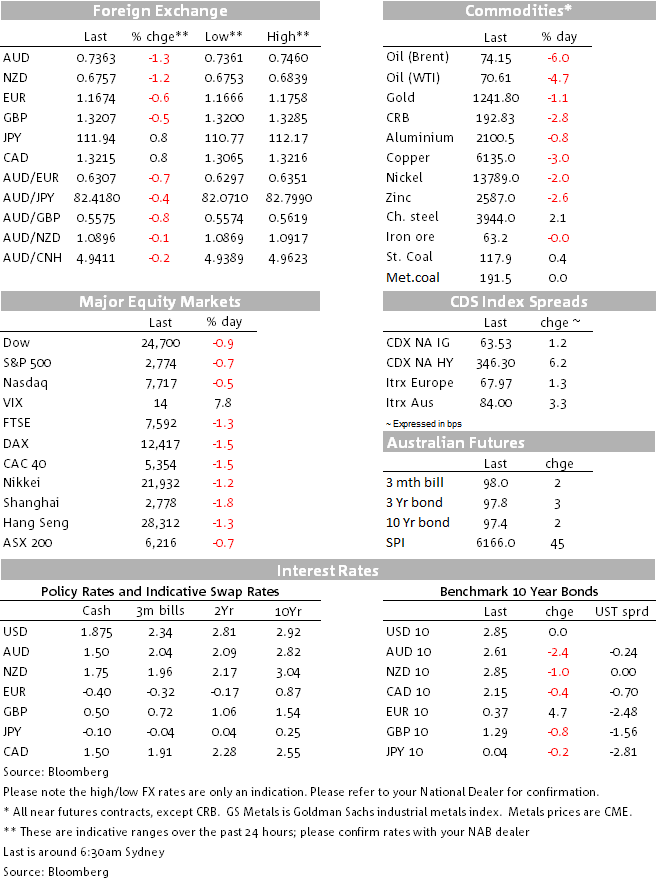

Unsurprisingly reaction to the US plans to impose tariffs on an additional $200bn of Chinese goods (announced early yesterday), has triggered a sell off across risk assets overnight. European and US equities are down 0.5% and 1.6% and the commodity complex is also a sea of red with Brent oil down over 6% following reports that Libya will resume export activities (not quite at midnight, but I hope you get my drift). The UST curve is slightly flatter whilst the USD is stronger across the board with AUD the big G10 loser amid the risk off and softer commodity environment.

Asian equities came under pressure yesterday following news that the US administration had begun plans to impose tariffs on an additional $200bn of Chinese goods. This announcement was made after the New York close and late yesterday, China said that it intended to retaliate if tariffs are enacted adding that they won’t give into “threats and blackmail”. The US Trade Representative’s office said the 10% tariffs could take effect after consultations end on 30 August, so plenty of time before rhetoric becomes reality. Yesterday the Shanghai Composite closed at -1.76% and Nikkei ended at -1.19%

So against this backdrop risk assets remained under pressure during the overnight session. Major European equity indices fell around 1.5% on average and main US indices closed down between 0.55% and 0.88%. In the US, Industrials and Energy sectors led the declines reflecting the softness within the commodity complex with Brent oil leading the way (down over 7% at one stage, now – 6.18%), following news that Lybia would resume export activities at its eastern ports, easing concerns of a global supply shortage.

US equities have outperformed in the sell off and the USD index terms has had its best daily gain in ten days ( DXY +0.61% at 94.711). Price action over the past 24hrs suggests that at least for now, the market thinks that in an environment of heightened US led trade tensions, the US economy will hurt less than others and the USD will find more buyers than sellers, not only from EM FX, but also within the majors.

Looking at G10 currencies, it is not surprising to see the AUD as the big loser, down 1.22% and currently trading at 0.7366. In previous reports we have noted the aussie vulnerability to EM fortunes, the AUD is often seen as a liquid proxy option for EM exposure given the strong Australian economic links with China and thus it is not surprising to see the AUD declining amid the current trade-driven global growth concerns. Add to that a small spike in the VIX index ( up 1p to 13.63) along with commodity declines from oil to copper (-3.20%), LMEX(-2.52%) and gold (-1%), and you have the perfect recipe for a soft AUD. We remain of the view that trade tensions are likely to get worse before they get better and as such we still see more downside risk for the AUD.

Amongst the other G10 decliners it is interesting to note the CAD is -0.74% despite the fact that the BoC lifted the cash rate by a quarter point to 1.5% while the statement reiterated the Bank’s intentions to continue with its gradual tightening plan, brushing aside trade tensions concerns. To be fair, looking at the overnight chart, USD/CAD did fall post the BoC statement, dropping to an overnight low of 1.3066 from 1.3136 prior, but in the end the sharp decline in oil prices dominated proceedings with USD/CAD now trading at 1.3208.

A word on USD/JPY also deserves a bit of space on the daily. Traditionally in a risk off environment, JPY enjoys a safe haven bid, but the recent trade tensions has seen USD/JPY well supported above the ¥110 area and overnight USD/JPY made a move above ¥112 ( now just above the figure). Last week we learned that buying of overseas equities by Japanese investors reached an all-time high, so for now it seems that Japanese investors are treating the selloff in equities as a buying opportunity. USD/JPY has now broken through an important resistance level, so technically it has room to move higher, but caution is required given the risk off environment.

Reports that some ECB policy makers see an increase in interest rates as early as July next year saw Bund yields edge higher. EUR/USD pushed up toward 1.1760 at one point before the single currency gave way to broad USD strength. EUR/USD opens this morning around 1.1675, down around 0.6% on this time yesterday.

GBP was relatively subdued compared to other major currencies with no new news on Brexit machinations. pound is around 0.5% lower, now at 1.3205.

US Treasury yields fell immediately yesterday after the new China tariff list was revealed. From around 2.865%, the 10 year Treasury yield fell around 4bps before stabilising. Overnight, yields did push back above 2.86% supported by higher inflation data, before pulling back to around 2.84% as oil prices slumped.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.