Confidence and Conditions Lift

Insight

After the excitement of Parmageddon last week, followed by the sudden enforcement of steel and aluminium tariffs on Trump’s supposed allies, the markets can at last look forward to a more traditional week where data and central bank policy drives the agenda.

https://soundcloud.com/user-291029717/and-now-for-something-completely-normal

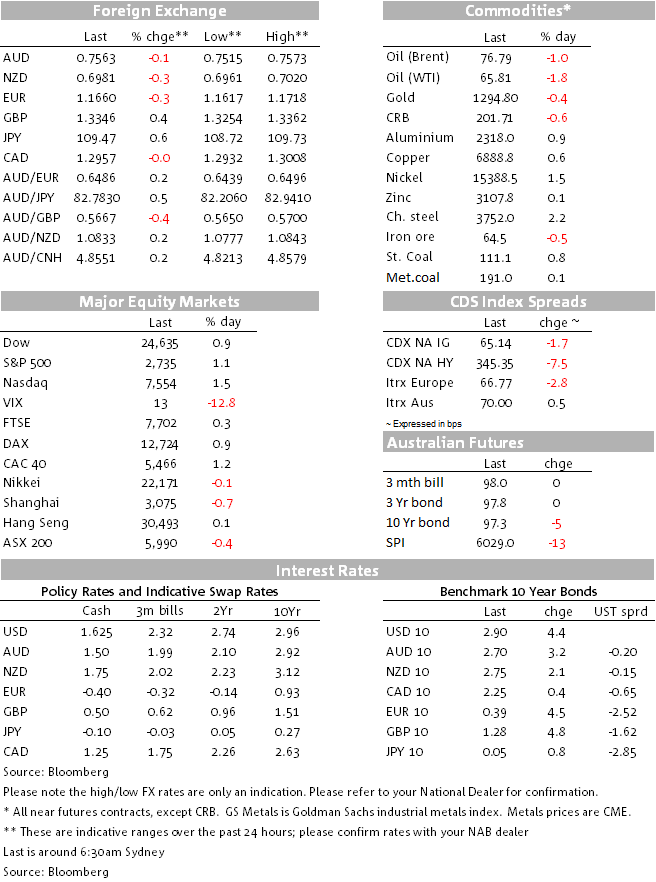

An all-round strong US payrolls report backed up by a better than expected manufacturing ISM drove Friday’s offshore market moves, with some of the payrolls impact coming an hour before the release, courtesy of a 7:21am Trump tweet that he was ‘Looking forward to seeing the employment numbers at 8:30 this morning’. US stocks, Treasury yields and the dollar were all higher, USD/JPY leading the way in FX with a gain of the 0.66%. Sterling bucked the stronger USD trend, aided by a better than expected manufacturing PMI (54.4 from 53.9). AUD/USD finished Friday almost exactly where it started around 0.7570. It’s opened the week slightly lower, seemingly a response to the apparent lack of positive progress in the weekend Sino-US trade talks in Beijing.

US May payrolls rose by a better than expected 233k with 15k worth of upwards revisions; unemployment unexpectedly fell to 3.8% (3.755% unrounded so very close to recording a two-tenths drop); and average hourly earnings lifted by 0.3% even though the seasonal risk was for 0.1% versus the 0.2% consensus. This pulled annual growth up to 2.7% from 2.6%. The Manufacturing ISM released 90 minutes later printed 58.7 up from 57.3 with strong orders, output and employment sub-readings (price paid were also higher).

Speaking to Reuters on Friday, San Francisco Fed President John Williams said that the Fed should continue with gradual rate increases over the next two years. He says the Fed is about three rate hikes away from reaching a “neutral” level and that he sees less need for forward guidance from the Fed as rates near neutral. The Fed does not necessarily need to pause on rate hikes once rates reach neutral, but could drive rates still higher if the economy remains strong and inflation is at or above the Fed’s 2% target, Williams reportedly said. This echoes similar comments from Fed Governor Lael Brainard last week (traditionally regarded as a dove) who also spoke of the potential need for Fed policy to become restrictive. This is the real debate markets will be having in coming months, not whether the Fed will deliver three or four hikes this year. At the moment, there is nothing standing in the way of it being four, but the year still has a long way to run and ‘events’ could yet intervene.

The NASDAQ led the post-payrolls stock rally to be up 1.5% vs. ~1% for the S&P and the Dow. Markets weren’t fazed by the announcements from Canada, Mexico and the EU of their intention to take retaliatory measures against President Trump’s decision to go ahead with tariffs on steel and aluminium imports from these areas. The EU and Canada are taking their grievances to the WTO (a process likely to take a year or more). Canada has said it would impose tariffs on US$12.8 billion worth of US imports, including whiskey, orange juice, steel, aluminium and other products. Mexico said it would retaliate with “equivalent” measures against US products, including pork legs, apples, grapes, cheese, steel and other goods. The EU has yet announced its list, pending agreement by all 28 EU members.

In bonds, Treasury yields out to 10 years rose a fairly uniform 4-5bps with the 2s/10s curve unchanged on the day. On the week, yields are still lower due to the mid-week Italy-related swoon on safe- haven buying, with the 2s/10s curve over 2bps flatter. The 10yr UST-Bund spread ended little changed on the week as Bunds pared back the mid-week, Italy-related yield slump, while 10 year Australian government bond yields ended 6.5bps down on the week even with the 2.5bps rise in Friday’s offshore futures market session.

In FX, USD index gains were a little under 0.2%, having been as much as 0.5% higher immediately post-payrolls. With Italy-related downward pressure on EUR/USD over for now at least, this plays to our view that last week’s high on the DXY of 95 will not be easily recaptured or exceeded near term. USD/JPY led the rally on the perfect combo of positive risk sentiment combining with higher US yields. Sterling built on its post-manufacturing PMI gains to be the best performer on the day (and recovering well from an immediate post-NFP dip). Also supportive were comments from UK Chancellor Philip Hammond who told Bloomberg TV that “there is clearly scope for the Bank of England to gradually and carefully normalize interest rates over time” AUD ended Friday night pretty much where it started while the NZD was nearly 0.3% lower. On the week, USD overall performance is narrowly mixed (DXY down 0.1% but the broader BBDXY dollar index +0.1%). NZD was the best performing G10 pair and SEK the worse. AUD ended the week 0.3% higher and some 1.2% up from its intra-week low of 0.7476.

In commodities, ‘Dr Copper’ led the pack with gains of just over 1% (no fear here of trade tariffs hitting global growth hard) with the LMEX index +0.6%. Iron ore softened as did oil and gold. On the week, it’s a great story for coal (gains of 5% and 4% for steaming and mett. coal respectively) and industrial metals in general. Steaming coal is now some 20% up on its early April 2018 lows.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.