We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Is the bear market in oil about to turn?

https://soundcloud.com/user-291029717/an-oil-pact-and-boris-bro-a-blow-for-brexit

The (repeat) lessons from Friday is that the USD can’t go down if the EUR and GBP aren’t going up and that the USD goes up when risk sentiment goes down.

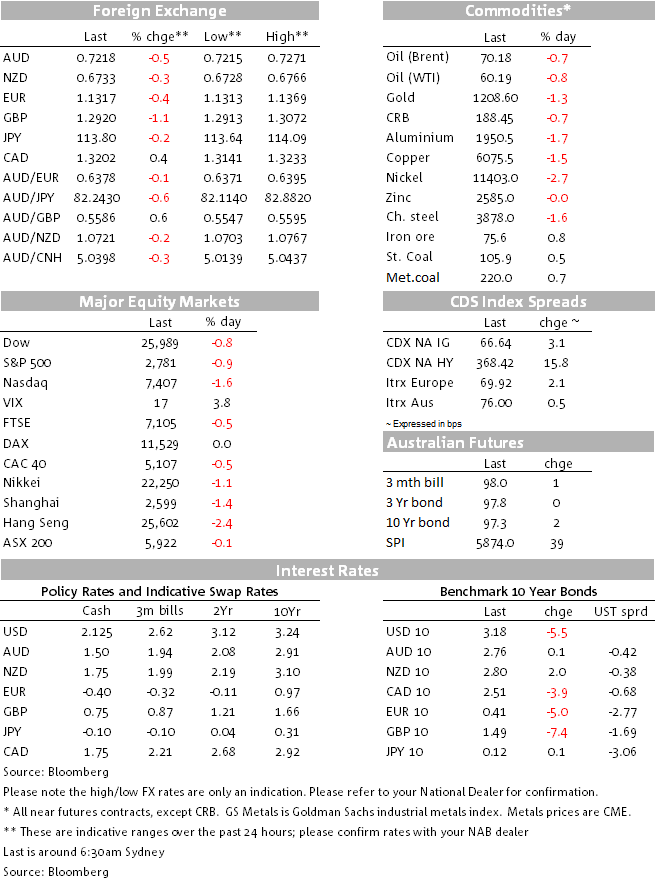

Thus a give-back of much of the recent Brexit Withdrawal Agreement-related optimism on GBP, related EUR slippage (currently a low beta GBP, but compounded by wider Italian BTP-German Bund spreads) and a renewed sell-off in US stocks (again IT-led) saw DXY briefly back on a 97 handle, so back close to its 97.20 November 1st high. It closed Friday at 96.90. AUD pulled back to 0.7226 at Friday’s New York close have briefly touched 0.73 last Thursday and is slightly weaker again at Monday’s open (just sub-0.7220 as I write).

GBP, NOK and SEK fared worse, JPY and CHF both exhibited safe haven characteristics to be up on the USD while NZD was the least worse performing G10 commodity currency.

On the week, NZD is the clear winner, in large part due to Wednesday’s stellar labour market data, followed by AUD, both currencies higher despite an overall stronger USD and weaker EM FX. CAD fares worse in G10, a product of sharply lower oil and the emergence of some doubt as to whether the USMCA can necessarily get through Congress in current form.

Friday’s positioning data from the Chicago futures market (IMM) shows a pullback in net speculative positioning in AUD and NZD for the first time, more so in NZD than AUD, though the outstanding net short in both currencies remains significant.

GBP – and with that EUR – has opened almost half a percent lower this morning amid reports of potentially more Cabinet resignations, as yet no ‘breakthrough’ on the Irish border backstop question that would satisfy the 10 Northern Irish DUP MPs who prop up the government, or whether the deal that looked to be getting closer to ‘done’ last week (before Cabinet minister Jo Johnson’s resignation – he’s a ’Remainer’ by the way in contrast to his brother Boris – will be able to win parliamentary support). One thing’s for sure; GBP won’t be where it is now at the end of this week.

The poor showing for APAC stocks (led by Chinese bank names after reports that they were being instructed to meet targets for expand lending to China’s SME sector) fed into Europe and then the US, the latter hurt at the open by an big upside surprise on US Producer prices, 0.6% headline, 0.5% ex-food and energy, versus 0.2% expected for both, though the ‘core-core’ measure, excluding trade service prices (i.e. profit margins) as well as food and energy, was 0.2% as expected.

The IT sector was once again under pressure, Apple losing another 1.9% (its admission of hardware problems in some iPhone X and MacBook Pro models one of the factors cited here). So the NASDAQ (-1.65%) again underperformed the S&P and Dow in a falling market.

It was notable though was that the US staged a decent rally in the last ‘hour of power’, and Friday’s losses haven’t sufficed to fully offset gains from earlier in the week, all bar Shanghai posting positive weekly returns, both the Dow and S&P up by over 2%.

In conjunction with weaker stocks and notwithstanding the unwelcome PPI surprise, Treasury yields were lower across the curve Friday, 2s by 4bps and 10s down 5.5bps. Helpful to the cause of lower nominals yields was a fall in break-evens (-2.3bps at 10 years) presumably linked at least in part to the further decline in oil prices.

On the week US curve flattening was the theme, 2s +2bps and 10s -3bps, while in Europe the BTP-Bund spread was 10bps wider, linked to the EU rejecting the growth assumptions behind Italy’s budget plans and Italy showing as yet no signs of backing down on its spending proposals and implied budget deficits:

According to press reports this morning (Reuters) citing government sources, Italy’s economy minister is looking to revise down the budget’s growth forecast for next year to try to reach a deal with the European Commission over fiscal policy. The Commission has given Rome until Tuesday to present a new budget and could start disciplinary steps against Rome later this month.

Steel making commodities continue to buck the trend of weakening oil and base metals, suggesting Chinese demand remains robust. Oil was weaker again in front of the weekend OPEC gathering which was to have the cartel contemplating scaling back output having earlier increased it in the face of rising prices. At $60.19 (-$0.50), WTI closed at its lowest since early March and in (-20%) bar market territory, Brent at $70.18 to its lowest since late March. Base metals were all lower, aluminium and copper leading the way, both off more than 1.8%. It’s a similar picture on the week, coking coal and iron ore both up (steaming coal too) while both oil benchmarks and copper are all down by more than 4%:

In the last few hours, Saudi Arabia has indicated it will reduce its December output by 500,000 barrels, though agreement to a formal OPEC+Russia production cut for 2019 is currently being described by Saudi Arabia as ‘premature’. Whether Iraq and Russia would come on side here is crucial. Certainly the technical committee of the cartel that met on Saturday determined that on current production levels, the oil market was likely to be oversupplied in 2019.

US PPI +0.6% (0.2%E, 0.2%P); yr/yr 2.9% from 2.6%

US PPI ex-food and energy 0.5% (0.2%E, 0.2%P); yr/yr 2.6% from 2.5%

US PPI ex-food, energy, trade services (‘core core’) 0.2% (0.2%E, 0.4%P); yr/yr 2.8% from 2.9%

University of Michigan October prelim. Consumer sentiment 98.3 (98.0E, 98.6P)

UoM 5-10yr inflation expectations 2.6% from 2.4%; 1-yr 2.8% from 2.9%

UK Q3 GDP 0.6% (0.6%E, 0.4%P)

The details reveal substantial weakness in business investment at -1.2% (0.2%E). This was offset by a strong net export contribution at 0.8%, but which was driven by weak imports.

UK September industrial production 0.0% (-0.1%E, 0.0%P revised from +0.2%); yr/yr 0.0% from 1.0%

UK manufacturing production 0.2% (0.1%E, -0.1%P revised from -0.2%); yr/yr 0.5% from 1.3%

UK September visible trade –£9.731bn (-£11.395bn E)

UK September total trade –£27mn (-£1.5bn E)

CoreLogic reported a preliminary all capital cities weekend auction clearance rate of 46.8% versus last week’s final 42.7.0% (latter lowest since June 2012) on increased auction volumes – 2,384 vs the prior weekend’s Melbourne Cup week reduced 1,541. Melbourne cleared a preliminary 48.3% versus a final 45.7%, Sydney 48.4% versus a final 42.6%. Final rates will be likely be in the low 40 percents.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.