Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

US equities closed the week little changed with the S&P 500 in consolidation mode ahead of a new week that includes the FOMC meeting and a busy earnings calendar. UST were little changed and the USD continued its recovery.

Events Round-Up

UK: GfK consumer confidence, Jul -30 vs. -25 exp.

JN: CPI (y/y%), Jun 3.3 vs. 3.2 exp.

JN: CPI ex fr. food, energy (y/y%), Jun: 4.2 vs. 4.2 exp.

UK: Retail sales ex auto fuel (m/m%), Jun: 0.7 vs. 0.2 exp.

CA: Retail sales ex auto (m/m%), May: 0.0 vs. 0.2 exp.

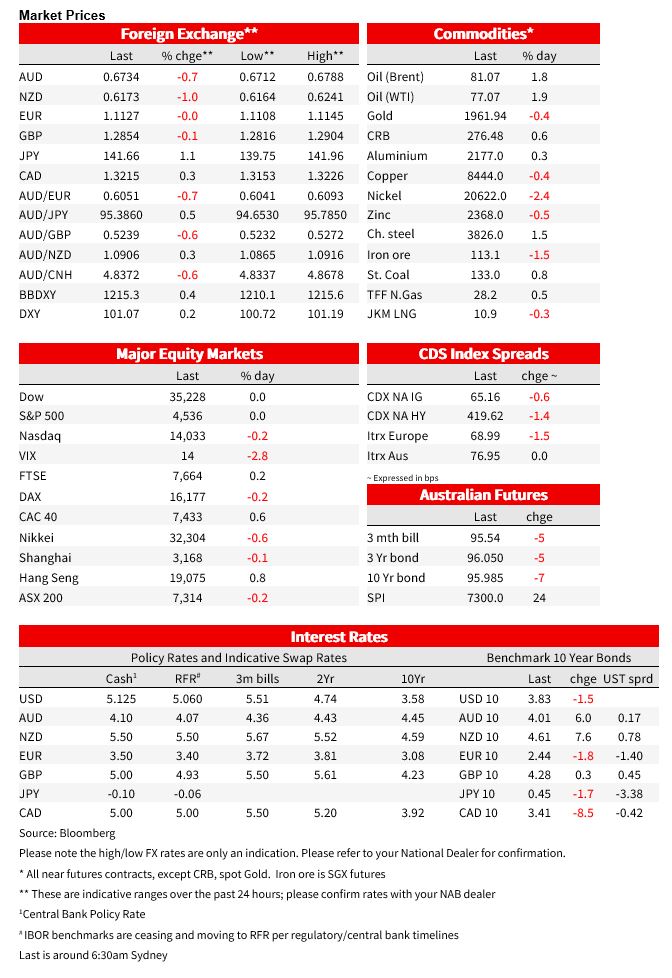

US equities closed the week little changed with the S&P 500 in consolidation mode ahead of a new week that includes the FOMC meeting and a busy earnings calendar. UST were little changed with the curve extending its flattening bias for the week. The USD continued its recovery with JPY and NZD the notable underperformers while in commodities, oil process recorded their 4th weekly gain and wheat prices fell.

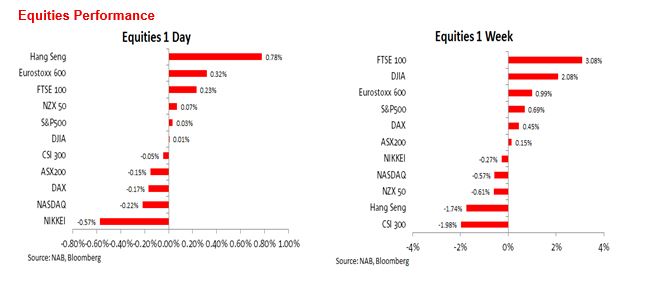

The S&P 500 closed 0.03% higher on Friday while the NASDAQ was -0.22%. On the week the S&P 500 climbed 0.89% and now it is just 260 points below its previous high just above 4800 recorded around 20 months ago. Of note too, gains in the S&P 500 have widened away from megacaps with pro cyclical sectors now taking on a leading role, so far in July Financials ( 4.49%), and Energy (3.44%) have led the gains with Utilities also in the mix ( up 4.51%). While the yield curve continues to highlight the risk of an imminent recession, US equity investors are embracing the prospect of a soft landing.

European stocks closed higher on Friday with the Euro Stoxx 600 +0.32% and up 0.89% on the week. The Hang Seng climbed 0.78% but was down 1.74% over the past 5 days. Meanwhile China’s CSI 300 was -0.05% on Friday and the notable underperformer on the week, down 1.98%.

On Friday, Beijing announced another piecemeal stimulatory measure saying that it will support local governments to increase the purchase of new energy vehicles in public sectors. According to Bloomberg, in recent weeks China has announced 31 measures to improve conditions for private business and are considering easing home buying restrictions in the nation’s biggest cities. Yet the CSI 300 recorded its worst week in four and the Hang Seng China Enterprises Index lost 2.2%. Later this week, China’s politburo meeting is expected to unveil a new round of stimulatory measures, but the equity market is seemingly brazing for underwhelming news.

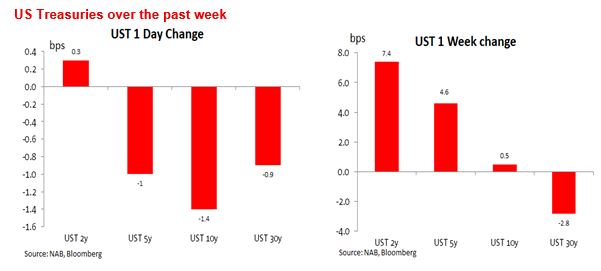

Ahead of the FOMC meeting this week, US Treasuries had a quiet end to the week. Front end yield closed little changed with the 2y Note at 4.844% while the 10y Note eased 1.5bps to 3.835%. The curve extended its flattening bias evident in recent days with the 2s10s curve down 7bps over the previous five days, closing the week at -101bps.

Looking at European yields, UK 10 Gilts were little changed on the Friday, showing little reaction to the better than expected June retail sales figures. Sales volumes in June were 0.7% higher than in May and well above the 0.2% expected by consensus. Going the other way, however, GfK reported that consumer confidence fell in July for the first time since January. Meanwhile ahead the ECB this week, 10y German Bunds eased 3bps to 2.46%.

Over the week, 10y UK Gilts were the big movers, down 16bps to 4.28% with the softer June CPI print halfway through the week, the main driver for the move lower in yields.

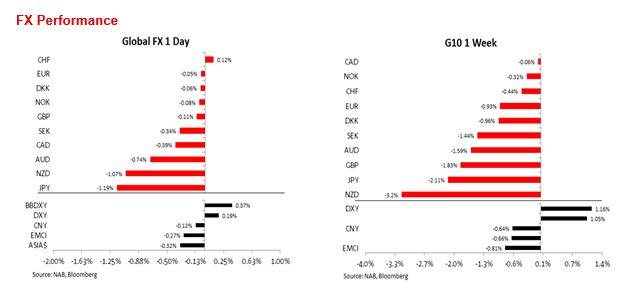

The USD continued its recent recovery on Friday with the DXY index up 0.19% while BBDXY was +0.37%. Both USD indices climbed over 1% during the week with the DXY index now looking more comfortable at 101.09 and above key support levels.

On Friday, the USD was stronger against all G10 pairs, barring CHF wish was little changed with JPY (-1.19% now at 141.73) and NZD ( -1.07% and now at 0.6173) were the big underperformers on the day . JPY weakness was fuelled by media reports suggesting the BoJ will stand pat this week, dampening expectation for a YCC tweak while NZD’s weakness was seemingly driven by flow dynamics given the absence of any fundamental reason to underperform.

On Friday Japan release its CPI figures for June, the headline and core CPI printed one tenth higher than previous month while the important Core Core reading (ex fresh food and energy) came in line with expectations, but at a still very elevated 4.2% yoy, but one tenth below the previous months.

The data tentatively suggests that core inflationary pressures may have picked in Japan , but these are still early days and with the core core reading 2.2% above the Bank’s target, keeping an ultra- easy monetary setting seems difficult to justify. Still, media reports late on Thursday and Friday morning suggested the BoJ was not inclined to tweak its YCC policy with a Bloomberg survey showing 82% of respondents were not expecting any BoJ policy adjustment. A BoJ debate on YCC at this week’s meeting seems very likely give a likely upgrade to the Bank’s inflation forecast, and if there is no tweak as expected, then a tweak in September or October remains a strong possibility.

The euro closed the week little changed and now starts the new week at 1.1124, down 0.93% over the previous five days. The AUD fell 0.74% on Friday and now trades at 0.6733%, down 1.6% over the past week. The AUD continues to show a great deal of sensitivity to risk sentiment, the US equity market has a busy week of earnings reports which could shape its performance over coming weeks, meanwhile China stimulus announcement is also set to be important for CNY and by its inevitable connection, important for the AUD too. In addition to risk sentiment, the FOMC meeting early on our Thursday is also going to be important for the USD.

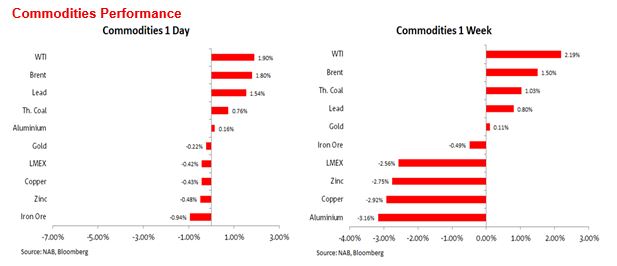

Moving on to the commodity space, oil prices climbed 1.8/90% on Friday and recorded their fourth consecutive weeks of gains, supporting the view that the market is tightening aided by OPEC+ reduction in supply. Elsewhere, gold and metal prices slipped a little on Friday, extending the weekly decline. Copper fell 2.82% on the week while aluminium was -3.16%. China’s stimulus announcement later this week cannot come soon enough. Meanwhile in soft commodities, wheat futures fell 4.1% on Friday to end at $6.975 a bushel as Ukraine made preparations to continue a grain-export deal.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.