Long-term signal vs. Short-term noise

Insight

The US dollar and equities are on the rise and EM currencies teetering on the edge of a bearish market.

https://soundcloud.com/user-291029717/the-widening-us-v-rest-of-the-world-divide

Overnight the MSCI Emerging Market Equity Index (MXEF) entered bear market territory, down over 20% from its early January highs (see chart). The latest moves have been led by a 6.5% drop in the share price of Tencent after the Chinese e-commerce behemoth reported its first profits drop in over a decade (a freeze on new game approvals in China reportedly one of the reasons). While we‘ve seen a bit of contagion to Developed Markets (the S&P 500 has just closed -0.8%) latest EM ructions serve to further highlight the contrasting fortunes of EM and DM markets this year and which in currency land is one key reason for the weakness in AUD (and NZD).

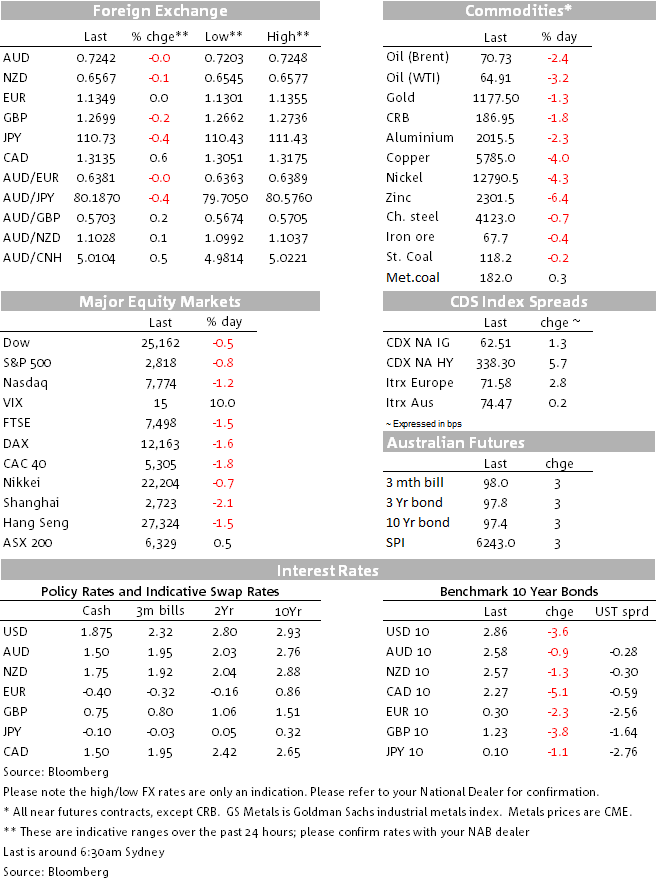

Commodity prices are in a sea of red, including a 4% drop for Dr. Copper and which brings its fall since early June to 22%. In the circumstances, it’s a wonder that AUD/USD is still trading on a 0.72 handle (0.7240) – more below. A generally risk-off tone sees US Treasury yields lower (10s by 4 bps to 2.86%) despite another set of generally good US economic data which to date shows no ill-effects from US tariffs or China’s retaliatory counter-measures.

So while the aforementioned MXEF is off 22% this year, the JPM Emerging Market Currency Index (FXJPEMCS) is off a slightly more sedate 14%. The reason it is marginally higher overnight is because of an 8% rally in the hitherto beleaguered Turkish Lire (8.33% of the index). This is after the Turkish central banks further cranked up restrictions on Turkish banks’ ability to lend out TRY, limiting swap and other derivative transactions to 25% of total equity capital (down from 50% imposed at the start of the week). Alongside, Turkey’s ally Qatar has promised $15bn in inward investment.

Against this, there is no sign of any thaw in US-Turkey relations. Yesterday Turkey imposed retaliatory tariffs against the US on a variety of products. The US has said it would consider lifting sanctions on Turkey if the American pastor Andrew Brunson were released, but not including on steel imports.

In contrast to the forced short covering rally in TRY, the Chinese Yuan is weakening once more. The onshore CNY went out at 6.935 yesterday (from 6.88 at the open) and the offshore CNH is currently at 6.95. Today’s fix will be particularly keenly watched. And yesterday evening, Indonesia somewhat unexpectedly raised rates by another 25bps, the third rise in as many months and fourth since April. Only 7 of 28 analysts were formally forecasting the move, which comes amid fresh pressure on the IDR and which, unlike some of the idiosyncratic reasons for pressure on other EM currencies this year, looks to be a classic example of higher US rates and strengthening USD pressuring capital flows and the currency amid a rising current account deficit (currently -2.4% of GDP). They’ll be more elsewhere where that came from if the Fed proceeds to lift rates twice more in H2 as currently expected and the USD keeps rising.

Elsewhere in EM ZAR, COP, MXN and RUB are all off between 1.4 and 2.2% (ZAR faring worse and after the government yesterday refined its land-expropriation demands to say that white farmers should hand back any land over 12,000 hectares without compensation).

In the G10 FX word, the DXY dollar index has pulled back in afternoon NY trade to be slightly down (-0.06%) with very mixed performances among individual currencies. SEK is again faring worse (still behaving more like an EM than G10 currency), off 0.68%, while the JPY fares best, up 0.38%. GBP, NOK and CAD have all fared worse than AUD and NZD, both of which are off less than 0.1%. WTI crude off over $2 or more than 3% has hurt CAD and NOK, while ‘as expected’ UK CPI data has done nothing to alter the drag on all things GBP from ongoing Brexit uncertainty/fear of a ‘no deal’/hard Brexit.

Given the ongoing pressures on EM currencies, we confess to being a bit surprised AUD is not currently lower, having had a look at the 0.7200 level yesterday afternoon during our time zone (low of 0.7203). Barring an unexpectedly strong upside surprise in today’s labour market data we suspect it’s only a (short) matter of time before AUD/USD trades on a 0.71 handle. Note too AUD/JPY has traded sub-¥80 overnight, further confirming we have moved into a new lower trading range.

With the exception of metallurgical coal (+0.3%) every commodity price we track across oil, precious and base metals and agriculture, are smartly lower. Zinc (-6.3%) and lead (-7.1%) are standouts but it’s the 4% fall in copper that captures a lot of the headlines given its ‘bellwether’ status with regards to the overall strength of global demand. Precious metals are further succumbing to the allure of a rising dollar and the prospect of still-higher US rates and it may not be a dissimilar story for oil where Brent crude is off 2.4% on the night and WTI -3.2%.

US Treasury yields were under mild downward pressure during the Tokyo day yesterday but yield declines accelerated in Europe, UST10s falling from 2.88% to a low of 2.84% (back to 2.86% into the NY close). Shorter-dated US yields are too far behind with the 2-year note off 3bp in the past 24 hours, while in Europe Eurozone peripheral bonds spreads are widening out again (Italy +13.3bps versus a 2.3bp fall for Bunds, Spain and Portugal both +3bps at 10-years).

UK: CPI (y/y%), Jul: 2.5% vs. 2.5% exp.

UK: Core CPI (y/y%), Jul: 1.9% vs. 1.9% exp.

US: Retail sales (m/m%), Jul: 0.5% vs. 0.1% exp. but June revised to 0.2% from 0.5%

US: Retail sales Control group (m/m%), Jul: 0.5% vs. 0.4% exp., June revised to -0.1% from 0.1%

US: Empire manufacturing survey, Aug: 26.6 v 20 exp.

US: Industrial production (m/m%), Jul: 0.1% vs. 0.3% exp.

US: Manufacturing production (m/m%), Jul: 0.3% vs. 0.3% exp.

July AU employment where the consensus looks for 15k new jobs and an unchanged 5.4% jobless rate. NAB looks for 25k new jobs and while we also have an unchanged 5.4% unemployment, another tick down to 5.3% is not out of the question depending on what happens to the participation rate. Were this to happen this week’s wages/jobless combo would be welcome news at the RBA, even if we’re some way from any thoughts of policy changes.

Also in our time zone Japan July trade figures, while offshore its UKL retail sales, US Philly Fed survey and housing starts

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.