NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The Aussie dollar was on the rise overnight, even as all eyes and ears were waiting on an announcement on the next round of tariffs from the White House.

https://soundcloud.com/user-291029717/aussie-on-the-up-as-tariff-intensity-weakens

“Please don’t keep a-me waiting, Cause I’m so tired, Tired of waiting, Tired of waiting for you” –The Kinks-Size

Well, after all this waiting it seems that we are almost there with President Trump confirming a China trade announcement will be made after the US market close today. US equities have started the week with a negative tone, partly reflecting concerns over the likely impact and consequences from a new round of tariffs on Chinese imports.US tech shares decline also reflect problems with specific companies including Amazon. The risk off tone in equities has not been reflected in UST yields with the 10y tenor briefly trading above 3% while in currencies the USD has given back all of Friday’s gains.

Based on weekend reports, President Trump is expected to confirm the imposition of 10% tariffs on $200bn of Chinese goods. But reports overnight suggest there is a chance that the amount could be reduced to $180bn with high-tech imports likely to be spared (smart watches and fitness trackers the likely beneficiaries). Given the starting point a few weeks ago was for tariffs to be as high as 25%, an announcement of 10% is likely to be regarded as good news and if the amount is less than $200bn that is also likely to play with the positive vibe. This outcome would also suggest a degree of sensitivity by President Trump to a consumer backlash ahead of the November mid-term elections. Unlike the initial tariffs, this new round will expand into the consumer goods territory and therefore their inflationary impact is likely to be more visible.

After the tariff announcement focus will inevitably turn towards China’s response and here is where all that initial feel good could come undone. China may be limited in its ability to impose similar tariffs in volume terms, but it can still aim to disrupt the US supply chain with those tech exports an obvious target and the cancelation of trade talks is also likely to dampen the mood. We think US trade spat with China is not just about bringing manufacturing and jobs back to the US, strategically the US is not happy with the approach China has taken in order modernise itself with market access restriction and intellectual property rights one of the key sticking points. Thus if US-China trade tensions are considered from this perspective, then it is difficult to conclude a resolution is likely to be achieved any time soon. We would look to fade a rally on a 10% tariffs announcement and instead focus on China’s next move as a guide for whether things are likely to get worse before they get better.

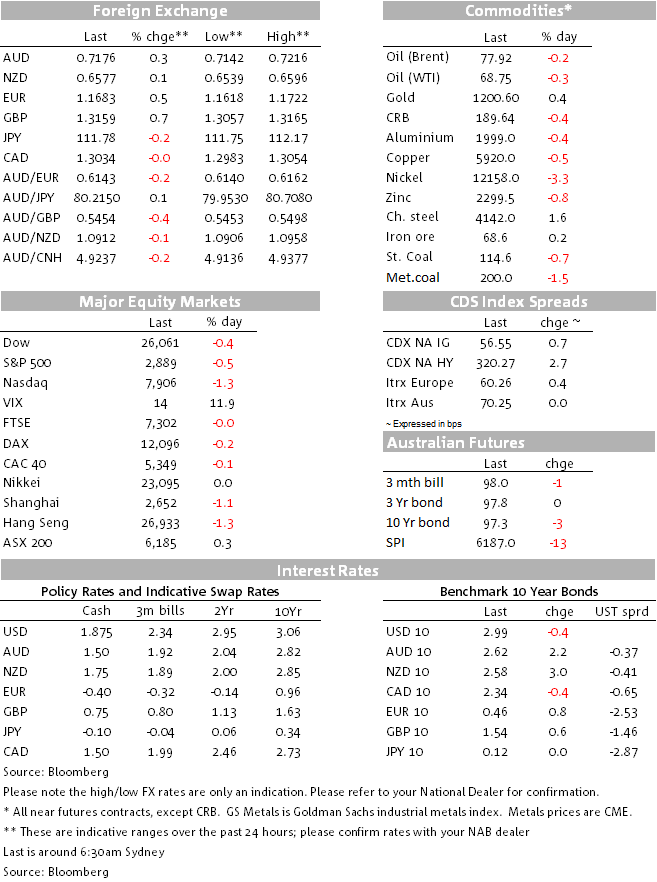

The USD has given back all of its Friday gains with modest gains in EM as well as AUD and NZD suggesting the FX market has watered-down the downside risk scenario given expectations for 10% rather than 25% of US tariffs on Chinese goods. A closer look at G10,however, also shows other factors have played into USD weakness overnight.

SEK is the top performer, up 1.54% after the Riksbank Minutes played to the grain of a rate hike at the December or February meeting. NOK has also benefited from this move (+1.01%) with the market becoming increasingly confident the Norges Bank will lift Norway’s deposit rate this week.

Brexit news have also boosted GBP (+0.70% to 1.3160) and all the above news have also lifted the euro (+0.52% to 1.1684). News flow around Brexit continues to be incrementally positive with the Times reporting yesterday that the EU was prepared to accept a frictionless Irish border post Brexit which increases the probability of a withdrawal agreement deal by the end of the year. Theresa May attends an EU leader summit in Salzburg on Thursday, with Brexit on the agenda.

AUD is up 0.35% relative to levels this time yesterday and the pair now trades at 0.7178. So far in September moves above 72c have been short lived and prospects of 10% tariffs instead of 25% have effectively ease concerns over the potential of an imminent dip below 70c. NZD is little changed over the past 24hrs, the pair now trades at 0.6578 with yesterday’s fall in the PSI to 53.2 offsetting the feel good news from the expectations of lower US tariffs on China.

After five daily consecutive gains the S&P 500 started the new week with a negative tone (-0.56%) amid trade concerns and weakness in tech shares. The NASDAQ index led the decline down 1.43% while the Dow was the best performer down just 0.35%. Impact from tariffs on tech companies’ supply chain has been one factor weighing on the sector, but the 3% fall in Amazon due to reports of an internal investigation on suspected data leaks and bribes of employees didn’t support the sector either while an analyst downgrade on Twitter also didn’t help.

Early in the session European stocks closed with modest mixed returns and late yesterday Asia had a mixed day with the China’s CSI down 1.15% while the HK Hang Seng was -1.30%.

10 year US Treasury yields briefly broke above 3% last night for the first time since the start of August, although it has since reversed back to sit just under the figure (unchanged on the day). For now UST yields appear to be immune to US led trade tensions with the move up in yields attributed to high grade corporate issuance, over $10bn overnight taking September tally to near $100 bn already.

In Europe, Italian fiscal developments continue their positive tone with Corriere reporting the 2019 deficit will be held at 1.6% of GDP (note this is below the 3% deficit cap of the EU). There are also proposals to put tax breaks on for holders of domestic government debt. BTPs continue to rally with 10yr yields down 13.4bps to 2.84%

Barring lead which is up another 1.6%, most commodities have begun the new week on the back foot. Iron ore and gold are unchanged, but metal prices are down around 0.5% and met coal is down 1.48%.

The Empire manufacturing survey, the first of the regional Fed surveys to report on the month, was weaker than expected in September (19 vs. 23 exp.). The detail though shows new orders and employment little changed – ie not as negative as the headline.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.