Online retail sales growth slowed in May following a fairly strong April

Insight

The markets have switched back to risk-on, helping the Aussie dollar rise faster than any of the majors this morning.

https://soundcloud.com/user-291029717/trade-war-what-trade-war

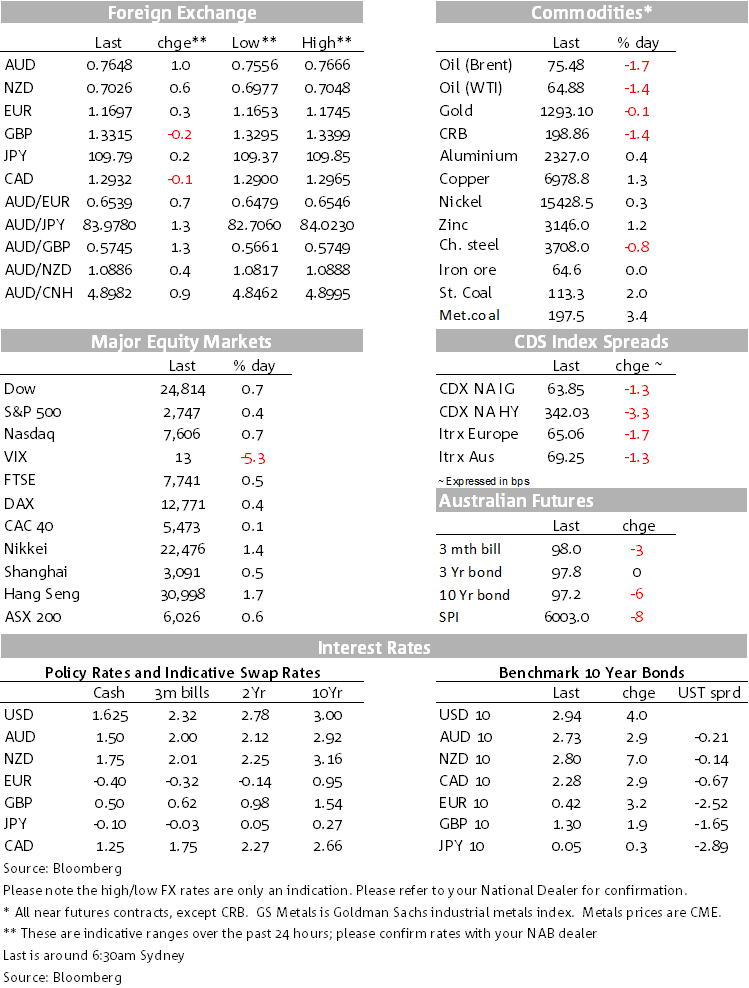

Geopolitics has been put to one side again today with markets re-adopting a risk-on posture, commodity currencies out in front in the FX space, base metals higher, stocks higher (and VIX lower) and bond yields backing up. (Italian yields have eased back further.) After trading toward the mid 0.75s yesterday at the start of the week, an increasing shift in Asian markets toward a more risk-on posture provided support, the currency unit also getting a double lift from better than expected Retail Sales for April and better than expected Company Profits and Inventories for Q1 ahead of tomorrow’s GDP report, NAB and the market already set on a 0.8%/2¾% pick for growth. Copper was up by 1.15% (as were other base metals), while coal prices enjoyed another leg up, met coal at $197.50/t (+3.40%) and Newcastle steaming coal up by $2.24/t to $113.30/t. The benchmark iron ore cash price was down $0.69/t to $65.47/t. Softs were weaker.

Yesterday’s numbers suggested some upside risk to Q1 GDP, today’s net exports contribution and government spending estimates for Q1 revealing whether 0.8% should be tweaked or not, already within sight of the RBA’s expectation that growth this year will average 3%. The RBA’s May forecast expectation that growth will get to 2¾% by June assumes that this current half will be considerably better than the second half of last year when cumulative growth was 1.1%. Growth was then held back in the December quarter when net exports detracted 0.5% from growth (partly from coal supply-side disruptions), that detraction expected to be partially or fully reversed this quarter. We will be alert to some general reference in this afternoon’s RBA post-Board statement that recent data point are broadly in line with the Bank’s expectation for some pick-up in growth this year. We have also been observing in recent months resilient and elevated coal prices and wonder/question whether the supply-disruptions evident in the latter part of last year have been resolved. NAB’s net exports contribution estimate for Q1 is +0.2% points, under the market’s +0.5% point consensus.

While risk-on prevailed, oil prices pulled back and for once WTI out-performed Brent. Bloomberg estimated that OPEC pumped 31.9mbpd in May, the same as in April and production the lowest for a year. The market overnight seems to have taken to heart that OPEC/Russia might supply more to the market, OPEC recently suggesting that “stable oil supplies (will) be made available to the market in a timely manner to meet growing demand and offset declines in some parts of the world”.

As my BNZ colleague has already remarked this morning, higher risk appetite generally has done JPY no favours this week, with AUD/JPY up 1.3% for the day to almost 84. GBP has also been soft overnight, with a focus back on EU-UK Brexit negotiations. The EU Withdrawal Bill will return to the House of Commons on 12 June, ahead of the next EU summit on 28 June, and the May government is still to decide on the way forward for the thorny Irish border issue. AUD/GBP is also up 1.3%, but against the Euro, the rise in the Aussie has been 0.7%. The BoE’s MPC member Silvana Tenreyro has been on the wires saying that she expects the softness in the economy as likely temporary, seeing little cost in waiting before hiking and only gradual rises expected ahead.

The ECB Governing Council’s Ewald Nowotny (Governor of the Austrian central bank) spoke on trade overnight, warning that “we know from history that even big wars begin with small skirmishes”, but as usual Trump was having none of it Tweeting (mainly on China) “The U.S. has made such bad trade deals over so many years that we can only WIN!” and “China already charges a tax of 16% on soybeans. Canada has all sorts of trade barriers on our Agricultural products. Not acceptable!” If the market needed one, it’s another reminder that geopolitical tensions could easily re-appear at any time, not only from US-China and with media focus on the G7 leaders meeting this weekend. For now however, it’s put to one side.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.