Robust growth for online retail sales observed in June

Insight

Markets are treading water as we await the outcome from the Biden-McCarthy debt ceiling meeting and the US CPI data release tonight. US and EU equities have ended the day lower while core yields have edged a little bit higher. Fiscal updates revealed contrasting AU and NZ fortunes while cautiousness in the air has favoured the USD.

NZ: Card spending total (m/m%), Apr: 1.0 vs. 2.3 prev.

AU: Real retail sales (q/q%), Q1: -0.6 vs. -0.6 exp.

CH: Exports (USD, y/y%), Apr: 8.5 vs. 8.0 exp.

CH: Imports (USD, y/y%), Apr: -7.9 vs. -0.2 exp.

US: NFIB small bus. optimism, Apr: 89.0 vs. 89.8 exp.

De La Soul can help you breathe when you tread water – De la Soul

Markets are treading water as we await the outcome from the Biden-McCarthy debt ceiling and the US CPI data release tonight. No major outcomes should be expected from the Biden-McCarthy with both sides expressing no interest for a short term solution nor any willingness to compromise. US and EU equities have ended the day lower while core yields edging a little bit higher. US and China data releases have come on the softer side of expectations and there has been an overarching hawkish tone from ECB speakers. Fiscal updates revealed contrasting AU and NZ fortunes while cautiousness in the air has favoured the USD.

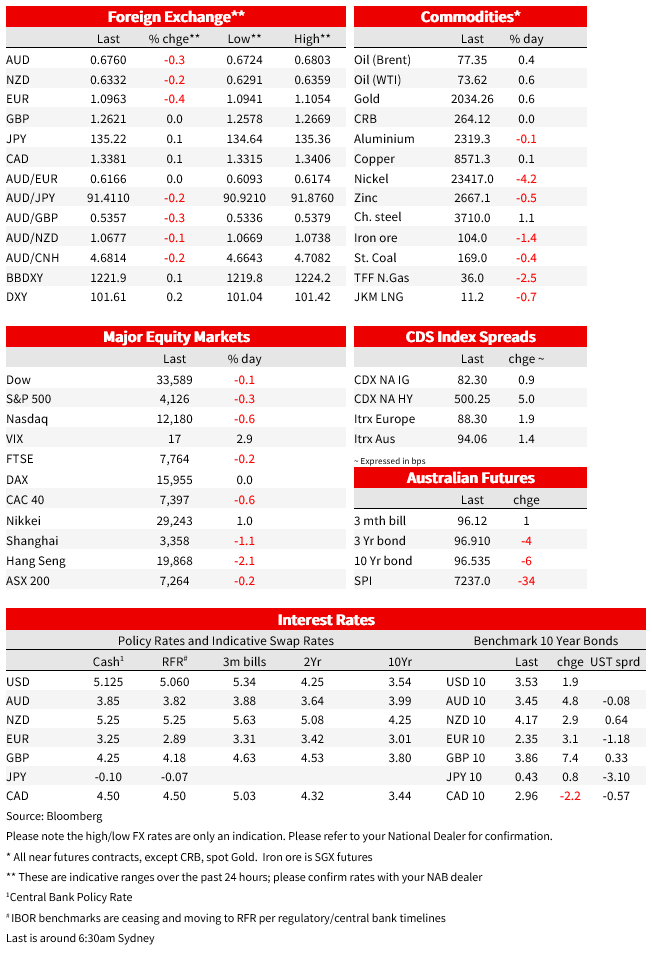

US equities have ended the day marginally lower. The S&P 500 is down 0.46% while the NASDAQ closed -0.63%. Debt ceiling negotiations and upcoming US CPI data releases are keeping investors cautious. On company news PayPal has been a notable underperformer, down close to 13% after a reporting disappointing outlook. Meanwhile, Airbnb fell post market after second quarter sales outlook fell short of estimates. One conclusion has been that rising prices may be curbing enthusiasm for travel. Earlier in the day the Eurostoxx 600 closed 0.33% lower with most regional indices also closing in the red.

President Biden and House Speaker McCarthy are meeting to discuss the US debt ceiling but heading into the meeting both sides made it clear that they had no appetite to consider a short-term debt-limit extension. These are early days in the negotiations and at this stage neither side is showing any interest to compromise, indeed from a political perspective it seems both parties are more interested in using the airtime to criticise the other side’s position with the hope of scoring some political points. Thus from a market’s perspective, it seems that we will need to get closer to the X date alongside some market volatility before a compromise is reach or a technical default is triggered. Treasury Secretary Yellen has been warning that the nation could exhaust its ability to meet all payment obligations by 1 June without action.

Data releases have also come on the softer side of expectation adding another layer for the cautiousness in the air. Yesterday China’s trade data release was underwhelming. China’s export growth slowed in April while imports slumped. Exports expanded 8.5% from a year earlier to $295 billion vs 8% expected. Exports got a boost from still-resilient demand from places such as Southeast Asia, though April’s figures were also aided by a favourable comparison with last year. That said, month on month estimate suggests exports fell compared to the previous month and provide further evidence of a slowdown in global demand. Meanwhile the larger than expected decline in imports -7.9% yoy vs. -0.2 expected were a disappointment too and are a concern to China’s demand recovery story.

US NFIB small business optimism index also fell short of expectations, sliding to 89 in April from 90.1 in March and vs 89.7 consensus f/c. That takes the headline to its lowest level since early 2013. In the details the encouraging news was the decline in selling prices at 33%, down from 37% with weaker sales expectations, economic outlook, and capex intentions also part of the subdued highlights.

Core yields edged a little bit higher overnight with 10y bunds in Europe climbing 2.5bps to 2.345%. UST yields ticked up in an almost parallel fashion with 2y, 5y and 10y rates up around 2bps. 10y UST Note now trades at 3.52%. UST yields traded higher earlier in the session, but strong demand in the $40bn 3-year note auction helped yields dropped from session highs. Bloomberg noted the auction traded 2.8bp through the WI level while 13% primary dealer award was lowest on record as indirect award increased to a record high 73.3%.

NY Fed President Williams kept the door open to further rate hikes and he noted that there will be a lot of data between now and the June FOMC meeting – he will be particularly focused on assessing the evolution of credit conditions and their effects on the outlook for growth, employment and inflation. He forecast a need to keep the restrictive stance of policy in place “for quite some time” and his baseline forecast does not see any reason to cut interest rates this year, against current market pricing which shows 2-3 rate cuts in the second half.

Overnight there was no shortage of ECB commentary, and the over-arching message was that there is a need to tighten monetary policy further . ECB Kazaks pushed back against market pricing that sees the ECB done somewhere between 3.5% and 3.75% and then cuts in 2024, saying such expectations are, ‘significantly premature. Importantly too, reflecting the ECB commitment to its inflation targeting mandate, Kazaks said the risk of doing too little is still the greater danger, adding that “persistently high inflation is a bigger problem than a relatively short recession.”. ECB Kazimir said the battle with inflation is, “far from won,” that, “slowing hikes allows the ECB to go higher for longer” and that ‘there is plenty of ground left to cover.’. Meanwhile, ECB’s Vasle played down economic growth risks saying Q1 growth was very good and the current period looks good as well. ECB Vujcic said the ‘job isn’t done until the there’s a change of trend in core inflation’ adding that baseline scenario suggests further rate hikes will be needed, but decisions will be taken based on data. This latter point was also repeated by Chief economist Philip Lane. For all the hawkish talk, markets remain wary by the ECB’s language and findings from its latest Bank Lending Survey that “past rate increases are being transmitted forcefully to euro area financing and monetary conditions.”

Moving on to domestic news, The Australian Federal Budget came in line with figures reported by the press in recent days with little market reaction. There is a surplus this year ($4bn) but returning to small deficits thereafter ($35-$50bn). Medium-term projections of debt are substantially reduced thanks to improvement in deficits this year and next few years (just over $100bn over the four years). The budget also has a strong focus on spending for those that need support, for instance, JobKeeper up $40 a fortnight, assistance for rent, substantial lift in aged car workers wages (+15%). Major cost of living package to assist 5m households and 1m small businesses with their energy bills, though these will still rise next year, but much less than before.

Our economists note a key talking point is whether the budget will add to inflation . In a specific sense it lowers some costs (energy prices will rise less than otherwise, pharmaceuticals, rents – and these can have flow on second round benefits in reduced indexation and a lower minimum wage increase next year) but added support, will add to aggregate demand. Australian inflation is likely to be slower to fall than other countries, and wages forecasts of both the RBA and Government look a little light, leaving risk that the RBA, while close to a peak, may not be quite there yet. Bottom line is that strong budgets and surpluses always coincide with a very strong economy and rising rates! Growth forecasts, like NAB’s envisage a decent slowdown in growth next year and the unemployment rate to head up to 4.5% mid 2024.

My colleague, Ken Crompton, also notes the Budget improvement has implications on the government’s funding intentions with big cuts to net (ACGBs) issuance in the next few years, but the refinance load picks up pretty quickly. Baseline issuance for FY24 is probably $70-75bn gross but they may choose to round up a bit and do some prefunding. Also worth noting green bonds will start next year and will “displace issuance of normal bonds”. Ken Crompton notes whether a green bond will have comparable depth/liquidity and can enter the futures basket will be very important questions.

For a comprehensive Budget analysis and interesting charts please see link to our economists and rate strategist note here.

Meanwhile on the other side of the Tasman, my BNZ colleague Jason Wong notes, the NZ government’s financial statements for the nine months ended March showed a deteriorating fiscal position and tracking much worse than projected – a shortfall in tax revenue reflecting a weaker economy and driving a core operating deficit of $3.4b, running $2.5b higher than projected. Gross debt of $143b was 37.7% of GDP, up $27b over the past year, or nearly 5 percentage points of GDP.

While contrasting fortunes between NZ and Australia’s external and fiscal accounts are on the radar, we think the currency market doesn’t yet reflect NZ’s poor relative position. This is a headwind for NZD and favours our view for higher AUD/NZD levels over coming quarters.

Cautiousness in the air has favoured the USD over the past 24 hours with USD indices up in the order of 0.15% (BBDXY) and 0.25% (DXY). The euro and other European currencies are at the bottom of the pile down between 0.5% and 0.3% and of note the euro didn’t get much support from ECB hawkish rhetoric, the pair starts the new day at 1.0962. USD/JPY is little changed at ¥135.22 while the AUD and NZD are a tad softer (-0.3%) at 0.6762 and 0.6335. Ahead of the BoE meeting tomorrow, GBP has been one of the better performers, holding its ground above 1.26.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.