NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

Trump seems to be offering a lifeline to Chinese telecoms company ZTE, whilst threatening car manufacturers with a 20 percent import tariff.

https://soundcloud.com/user-291029717/trump-blows-hot-and-cold-on-tariffs

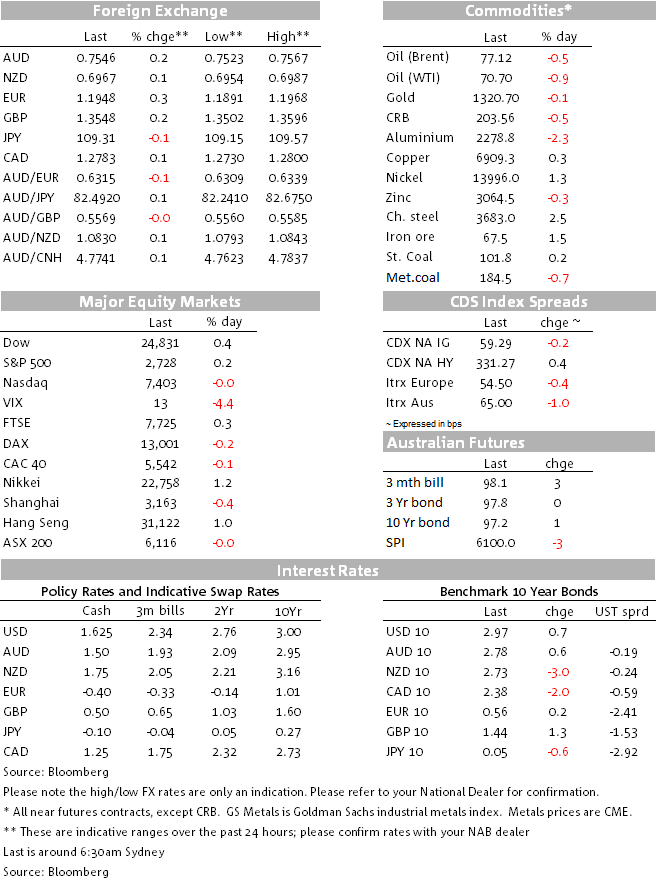

We had a fairly subdued end to what has been a pretty eventful week characterised by additional oil market (and broader commodity price) strength linked to Donald Trump’s decision to pull out of the Iran nuclear deal, a failure of US CPI inflation to accelerate, an abrupt mid-week reversal of earlier USD strength and which meant AUD pulled back up comfortably above 0.75, and a positive week for risk sentiment – Trump’s Iran decision notwithstanding – that saw the VIX closing below 13 for the first time since 26th January. For the AUD, Friday’s close around 0.7540 put it a pip or two above the previous Friday’s close. Few would have bet on it ending the week in the black after making a low of 0.7412 at mid-week.

The USD pulled up from its lows on Friday after a slightly better than expected University of Michigan consumer sentiment reading (unchanged at 98.8 against an expected fall to 98.3) but still ended Friday lower, while CAD suffered on a 1.1k fall in employment against an expected rise of 20k. For equities, after two good ‘up’ days for US stocks and which had fed gains for APAC stocks on Friday, US indices meandered rather aimlessly to all finish little changed (S&P+0.1%). Health care was the best performing sector, on a view that President Trump’s plans to lower drugs prices would be a year or more in the regulatory making and won’t impact pharma profits for a long while yet. On the week, all the main global indices are up, with the US leading the way with gains of between 2.3% and 2.7%, their best weekly showing since March and best closes since mid-March. The VIX ended Friday at 12.65.

US Treasuries also had a relatively quiet session Friday with 10s trading with a 2.95-2.98% range and finishing 2bp up on Thursday’s close at 2.97%. On the week yields are slightly higher bar the ultra-long end which benefited from Thursday’s stellar 30-year auction. In the US money market, we continue to see compression in the spread between Libor and OIS (from around 60bps at its widest in early April to 47bps at 3 months). This has a direct read-through to the BBSW-OIS spread here in Australia. The Libor slippage does somewhat reduce the attraction of long-USD ‘carry’ trades, but whether this is a factor beyond the fall-back in the USD from the middle of last week is debatable.

In FX, most currencies were slightly higher against the dollar, SEK in particular which continues to recover from its April/early May pasting. The exception was the CAD which suffered on the weaker than expected employment reading; the bigger influence this week will be the progress or otherwise on NAFTA negotiations ahead of what US House speaker Paul Ryan said late last week is an end-of-week deadline for a deal if Congress is going to legislate something before the November mid-term elections.

The DXY USD index was down 0.1% on Friday and unchanged on the week. Friday’s latest CFTC/IMM data on futures positioning showed that net speculative short positions in the USD against other currencies are now barely a third of what they were at their recent peak, suggesting that the USD no longer has the tailwind from position unwinding that was almost certainly a factor behind recent strengthening (and related AUD weakness). CFTC AUD positioning data shows speculative net short positioning up to 17k contracts out from 6k the week before.

In commodities, it was a very mixed performance Friday, with iron ore (+1.5%) the standout winner while oil gave back a little of its mid-week gains linked to Trump’s decision to pull out of the Iran deal. Most other commodities were also slightly lower. On the week, oil and all hard commodities are all up with Brent oil the standout, save for metallurgical coal, off 1%:

In other economic news China April lending and money supply data published on Friday evening was a bit stronger than expected on the lending numbers (New Yuan Loans ¥1180.0bn and Aggregate Social Financing ¥1,560bn, both up on March) but M2 money supply growth only lifted to 8.3% from 8.2% against 8.5% expected. We’ll get April’s activity data tomorrow.

The preliminary weekend auction clearance rate across the combined Australian capital cities was 61.0% down from last weekend’s final 62.1% (preliminary was 62.5%) on very slightly reduced auction volumes (2,245 vs. 2,311). Sydney cleared a preliminary 62.5% vs. last weekend’s final 63.1% and Melbourne a preliminary 61.2% down from the final 63.7% last week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

Hybrid issuance is becoming an ever more relevant funding instrument and capital management tool for corporate issuers today, attracting strong investor demand, write Tabitha Chang and Stefan Visser from the NAB Capital Markets Origination team.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.