A private sector improvement to support growth

Insight

Markets seem less concerned about the troubles in Turkey.

https://soundcloud.com/user-291029717/turkey-concerns-ease-the-lowdown-on-the-nab-business-survey

Breathe the pressure, Come play my game I’ll test ya – The Prodigy

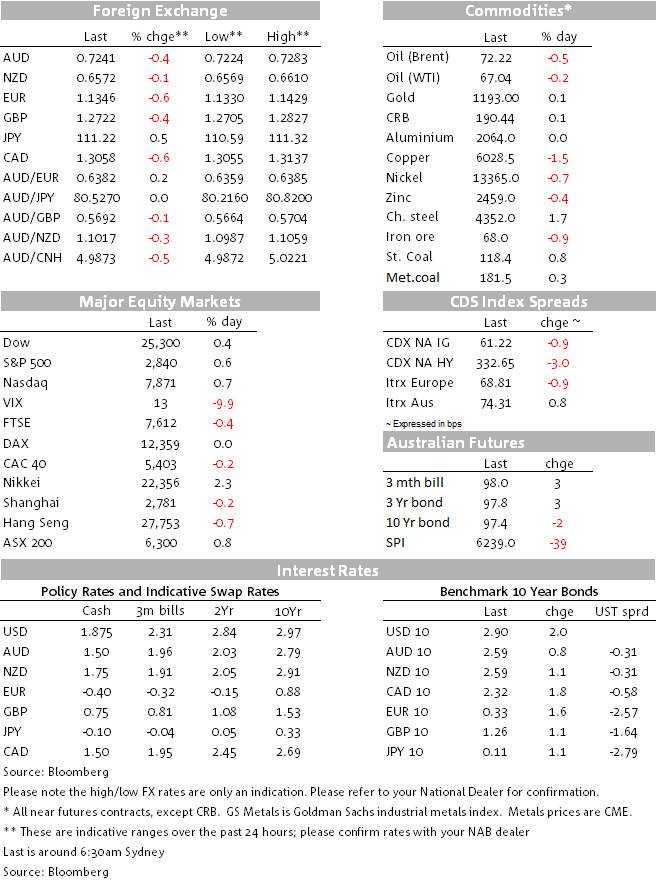

The stabilisation in the Turkish lira has helped risk sentiment overnight with the S&P500 recording its first positive day in five, but European equities have remained under pressure with the Bloomberg EU banks index closing at a new 18 month low. The USD is broadly stronger with EUR, AUD and GBP still under pressure while CAD is the outperformer. Higher UST yields have supported the USD while softer commodities have not helped the AUD.

TRY is up over 7% in the past 24 hours providing a bit of a breather to EM markets and easing concerns of contagion risk. News that the Turkish central bank had been making liquidity available to banks at 19.25% over the past two days, higher than the benchmark 17.75% repo rate supported the recovery in the lira overnight, but President Erdogan on the other hand has kept up the antagonism against the US calling for a consumer boycott iPhones and other US consumer electronics and blaming what he called an “explicit economic attack” for the lira currency crisis. Meanwhile the White House said “At the Turkish ambassador’s request, Ambassador John Bolton met with Ambassador Serdar Kilic of Turkey in the White House, feedback from the meeting has been that that there will be no negotiations or ease in pressure from the US, until Pastor Brunson is released.

So overall we see the overnight TRY price action as a temporary reprieve and it is hard not to see the lira remaining under pressure until we see a material fiscal restraint to cool down the economy , along with a measurable lift in rates by the central bank and a diplomatic resolution to US tensions.

It has been a solid night for the USD with major USD indices edging higher over the past 24 hours. The narrower DXY index has been the stand out, up 0.32%, the index currently trades at 96.682, a level not seen since late June last year. Looking at the main index component, the euro and GBP and JPY have all come under pressure for difference reasons with CAD the only pair that has been able to outperform the USD.

The union currency initially rose from 1.14 to 1.1420 after German Q2 GDP beat expectations and the Turkish lira rallied, but with EU banks under pressure amid concerns over some banks exposure to Turkey, the Euro traded to an overnight low of 1.130 overnight, before settling at 1.3444.Techincals have also not helped the Euro, with the break below the 1.15 opening the door for a move below 1.13 before any material support can be found.

GBP is down 0.45% and now trades at 1.2723. The GBP reacted negatively to a mixed UK labour market report that showed a surprise fall in the unemployment rate but lower than expected job growth. Wage growth excluding bonuses was in line with expectations. Meanwhile Brexit news remain a thorn on the side for the pound, British foreign minister Jeremy Hunt saying on Tuesday that Risk of no-deal Brexit rising, ‘everyone needs to prepare’. British politician have increased the scare tactic, but for now this strategy has had little effect on the EU negotiation stand.

The improvement in sentiment and move higher in UST yields has seen JPY climb back above the ¥111 mark with CHF also easing a little bit, down 0.10% over the past 24hrs. The lift in risk appetite however didn’t help the AUD, yesterday’s soft Chinese activity data didn’t really elicit a negative reaction, however the softness in commodities overnight along with lingering EM concerns, in spite of a temporary TRY reprieve, has seemingly been the overriding negative force. AUD now trades at 0.7242, after trading to an overnight low of 0.7225 ( a level not seen since January 2017). Similar to the euro, technicals are not helping the AUD either, the break below the support area of 0.7320/50 now means the aussie has a fair bit of room to move sub 72c before some material support is found.

Breaks in the AUD crosses are also a negative factor for the AUD. AUDNZD has continued to drift lower, after rejecting a move above 1.11 ( now trading at 1.1014), AUDJPY still looks like it wants to move sub the ¥80 mark and now we can add AUDCAD to the mix with a break sub 0.95 overnight, a level not seen since June 2016. AUDCAD has now broken below the downward channel evident since the start of June, chartist will probably start eyeing the 0.9326 low of in May 16 as the next key support for the pair.

The S&P 500 Index rose for the first time in five days, closing the day at 0.69%, financial and consumer discretionary shares where the winner in the session. Asia closed broadly higher , although Chinese indices ended the day flat and European indices were flat to lower with bank shares still under pressure.

Core bond yields drifted a bit higher overnight and the UST curve flattened a smidgen with the 2y rate leading the rise in the UST curve. the 10y UST yield now trades at 2.8985% and the 2y rate is at 2.631%

Despite improvement in risk appetite overnight, commodities have come under pressure against a stronger USD environment and global growth concerns amid a slowdown in Chinese economic activity. Copper is one of the big movers overnight down 1.61% and is threatening to make a break below the year to date lows of $266.95.

The US NFIB Small Business Optimism Index rose 0.7 to 107.9 for July, just 0.1 short of the July 1983’s highest reading in the survey’s 45-year history. The report included record highs in percentages of owners reporting job creation plans (23%) and job openings (37%), but 52% cited few or no qualified applicants for their positions. The availability of workers was cited by 37% as their number one business problem, one point under the record high.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.