Confidence and Conditions Lift

Insight

Quite a few moving points to what has been a reasonably volatile night in markets.

https://soundcloud.com/user-291029717/flat-us-cpi-aussie-job-numbers-turkeys-big-hike

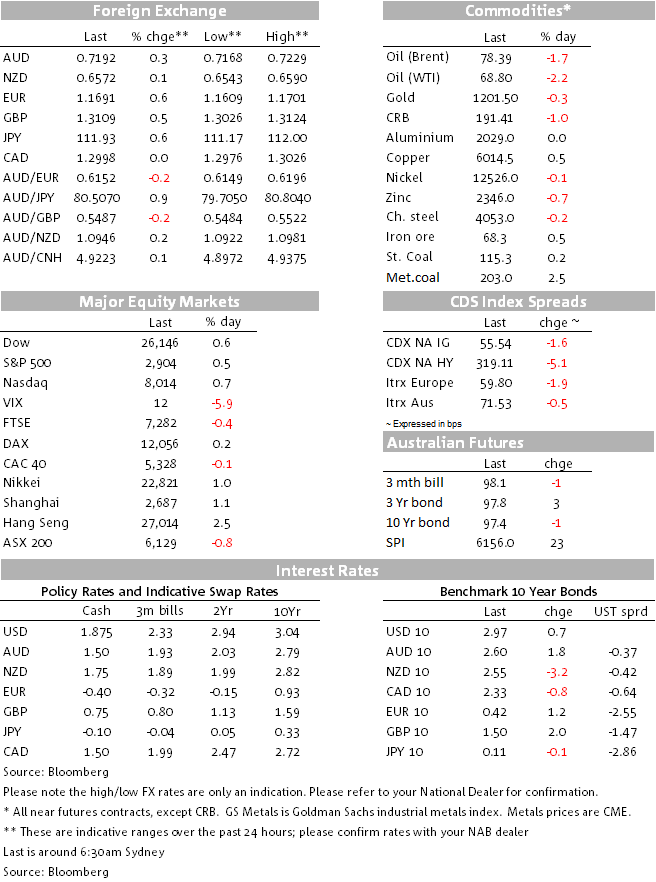

A 625bp rise in rates from Turkey’s central bank ignited a sharp rally in the Lira which in turn has dragged most (but not all) Emerging Market currencies up in its wake as well as boosting the Euro. The latter also benefited from a relatively positive tone to ECB President Draghi’s post Council meeting press conference. The US dollar and Treasury yields have taken a hit from lower than expected US CPI, while President Trump’s latest tweet on trade policy has punctured some of the optimism about a near term trade deal with China following news on Wednesday of a resumption of relatively high level talks. All up, AUD/JPY – of late the whipping boy for rising EM/trade angst in the G10 FX world – is back above ¥80 and now in positive month-to-date territory.

August headline US CPI came in at +0.2% against 0.3% expected while the more important core (ex-food and energy) reading printed 0.1% versus the 0.2% expected. Moreover, it was a ‘low’ 0.1% (0.08%) which had the effect of pulling the yr/yr rate down to 2.2% from 2.4% in July (and 2.4% expected). The miss was largely due to a sharp fall in Apparel prices (clothing to you and me) which fell 1.6% in the month and was the steepest monthly fall since 1949, subtracting some 0.05% points off the monthly core print. Outside of Apparel, other price moves were largely as expected with inflation indicators still pointing to elevated price pressures.

The numbers beg the question whether misses on both Core and Headline CPI signal the topping out of the rate of inflation in the US? In short we think not. Alternative measures of Core Inflation which strip out volatile price moves like Apparel, such as the Cleveland Fed’s Trimmed Mean, were stronger at 0.16% m/m. Inflation indicators such as the ISM Prices Paid and the NFIB Actual Price Charged continue to point to elevated price pressures which historically have correlated to rising inflationary pressures. As such, we think the data overall still supports the Fed continuing along its rate hike path.

The USD (DXY) fell by about 0.5% straight after CPI, to its lowest levels this month and putting it back near the bottom than the top of the mid-June through mid-September range. The policy-sensitive 2-year Treasury yield also fell, by 3.5bps to 2.73% initially, though it has retraced (to 2.75%) on higher German yields from a slightly more positive ECB (see below). As our London analysts note, the market reaction was likely exaggerated by markets looking the other way following the recent crop of stronger US economic data. Markets remain fully priced for a rate hike heading into the September FOMC meeting and are 80% priced for another in December.

Expectations of fireworks at Thursday’s ECB post rate meeting press conference were not exactly elevated and in the event observers didn’t hear anything particularly startling. But markets proved to be in a reasonably upbeat mood as Draghi toed a relatively upbeat message despite new quarterly staff forecasts that shaved a tenth off 2018 and 2019 economic growth as risks relating to protectionism gain more prominence. Draghi said, “We are observing an underlying strength of the economy that makes us think the downside risks are going to be mitigated by the improvement in the labour market and rising wages”.

This saw Bund yields rise from 0.41% to 0.44% and in the process helped stem the post-US CPI decline in US Treasury yields. Draghi confirmed a tapering of the Asset Purchase Programme (QE) from €30bn to €15bn per month from October 1st and a complete end by December, as per prior guidance, with rates not expected to rise until after the summer of 2019.

The BoE meeting was even less eventful. The Bank saw recent data as indicating that growth and wages were tracking a little stronger than it had anticipated in August, but not to such an extent as to change its broader outlook, which is for a very gradual path of rate hikes over the coming few years.

Just ahead of the Turkish central bank’s latest policy decision, President Erdogan was out saying that while he respected the central bank’s independence, “we should cut this high interest rate”. As if to underscore the former comment, the central bank then raised its one week repo rate by 625bps, to 24%, almost double the +325bps median expectation. This set the stage for a 4% appreciation in the Lira, a move which helped support EM currencies more broadly (already enjoying tailwinds from Wednesday’s news that Sino-US trade talks were set to resume). ZAR, CLP, COP, RUB and MXN all up by more than 1% and ARS and BRL the only EM currencies weaker on the day. The JPM EMCI index is 0.75% higher on the day (albeit TRY has an 8.33% weight in the index).

In the immediate wake of yesterday’s better than expected Australia employment print (+44k) AUD/USD had jumped from 0.7175 to 0.7200 but failed to hold on to the 0.72 handle. Immediately post the US CPI print, AUD lifted to a high of 0.7229 from 0.7180. Together with the risk positive tone emanating from the late week improvement in EM sentiment, the highly risk sensitive AUD/JPY rallied from around ¥80 prior to the Turkish central bank news to a high of ¥80.84 post US CPI – its best levels since August 31st.

Taking some of the heat out of the EM (and AUD) rallies since Wednesday night has been President Trump’s latest tweet on trade where he said the US felt “no pressure to make a deal…..Our markets are surging, theirs are collapsing. We will soon be taking in Billions in Tariffs and making products at home. If we meet, we meet?” (Sic).

The set-back from AUD has brought it down to the middle from near the top of the G10 pack with the EUR and (curiously) the CHF topping the leader board with gains of just over half a percent, EUR/USD touching 1.17 post ECB and US CPI (1.1690 now). USD/JPY briefly kissed the ¥112 level – its best since the start of August (¥111.95 now).

US stocks jumped at the open on the weaker US CPI data which have gone some way to dousing any concerns the Fed might need to step up the pace of tightening. The S&P 500 has subsequently flat-lined for most of the night to end +0.5% (Dow +0.6%, NASDAQ +0.75%). This follows a somewhat mixed session for European equities but where the Eurostoxx 50 finished up 0.2%. Healthcare and IT were the two best performing S&P sectors.

Oil prices are +/- $1.50 lower overnight, reportedly on some easing of supply concerns (not for any tangible reason I can see) and after Trump’s latest trade tweets. Industrial metals are mixed but copper is up 0.6% and iron ore up 50 cents. A two-day rally in gold has partly reversed,-$5 to $1,201.

In our time zone, we’ll get first the New Zealand manufacturing PMI at 08:30 AEST (last at 51.2) then at 12:00 the slug of China August activity readings covering Industrial Production (last 6.6%, 6.5% expected) Retail Sales (last 8.8%, 8.8% expected) and Fixed Asset Investment (last 6.6% YTD, 6.5% expected).

Offshore tonight, US retail sales is the main draw where gains of 0.4-0.5% are expected for the headline and various core measures. We also get industrial production (expected +0.3%) and – of interest in the context of China tariffs – imports and export prices. The first estimate of consumer sentiment – from the University of Michigan – is forecast at 96.6 from 96.2 in August. Eric Rosengren is the designated Fed speaker.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.