Online retail sales growth slowed in May following a fairly strong April

Insight

Markets turned on their head a little today, as the possibility emerges of trade talks between the US and China before the end of the month.

https://soundcloud.com/user-291029717/trade-talks-offer-glimmer-of-hope

Ah please talk to me, Won’t you please talk to me, We can unlock this misery – Peter Gabriel

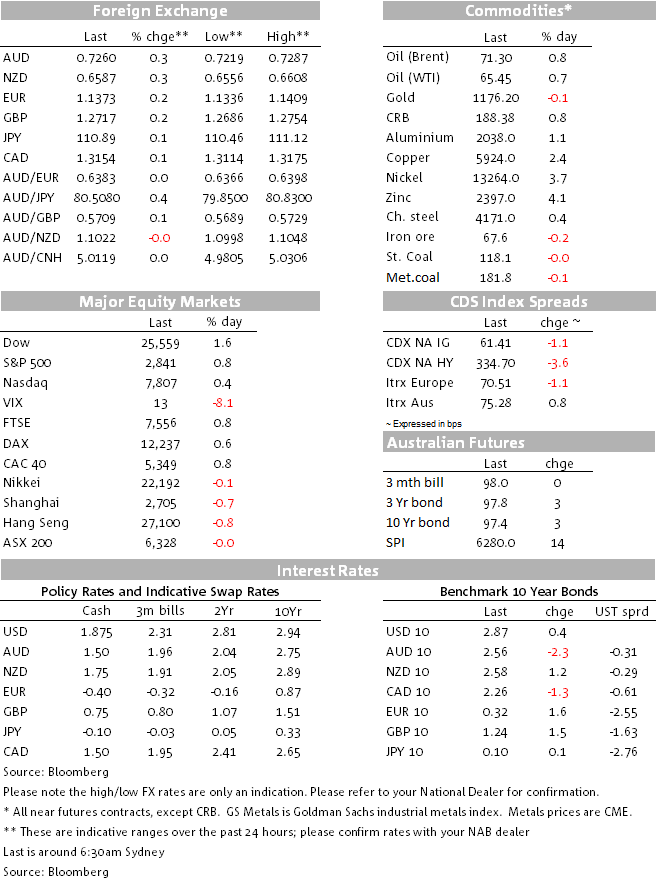

News of US-China trade talks revival, albeit at low levels, boosted risk sentiment during our session yesterday and overnight the positive mood was further enhanced by solid US earnings reports. The US has led the gains in equities and the improvement in risk sentiment along with gains in commodities helped the AUD and NZD outperform with EM FX also mostly stronger against the USD. The Turkish lira recovery stalled overnight after the US threatened to impose more sanctions if Turkey continues to refuse the release of US Pastor Brunson.

China confirmed yesterday that Vice Commerce Minister Wang will lead a delegation to the US late in August in order to revive trade talks between the two countries. The initiative is reported to come from the US Treasury Undersecretary and would be ahead of the early September public consultation deadline on Trump’s plan for an additional $200bn of Chinese tariffs. The relatively low rank of the negotiators suggests the prospects of a quick resolution are low and accordingly markets’ reaction has been cautiously optimistic. Overnight, Trump’s economic advisor welcomed the news, but again reminded everyone that the president’s “toughness and willingness to continue this battle” shouldn’t be underestimated.

News of the meeting boosted risk assets during our session and at the same time a weaker than expected CNY fixing also helped EM FX performed. Then a volatile session ensued following reports that Chinese authorities were taking steps to lean against further currency weakness. The news of banks in the Shanghai Free Trade Zone being banned from lending money to offshore saw fears of a funding squeeze, USD/CNY fell around 0.75% from 6.9348 to 6.8853 yesterday while the offshore renminbi (CNH) experienced its largest one day rise in more than a year (over 1%), the rest of USD/Asia followed China’s lead throughout the day with the USD softer across the board.

So against a backdrop of improved sentiment ,stronger EM FX and higher commodities NZD and AUD are the top G10 performer over the past 24hrs, gaining about 0.3% against the USD and currently trading at 0.6589 and 0.7261 respectively. The mixed AU employment report didn’t elicit a big AUD reaction, the decline in the unemployment rate by one tenth to 5.3% was enough to offset the disappointment in the employment growth of -3.9k (Mkt: +15k, NAB: +25k). Looking through recent volatility, employment growth remains strong at +27k (in trend terms), well above the ~17k needed to keep the unemployment rate steady (assuming unchanged participation).

Although it was a good night for the AUD and NZD boosted by risk sentiment, it is difficult to get too excited over the prospect for both antipodean currencies. AUD is still trading sub 73c and NZD sub 66c, as noted above the prospects for swift US-China trade resolution remain low and the lack of any concrete development suggest caution is still required.

As a sign of cautiousness, USDJPY is still finding it difficult to trade above the ¥111 mark and despite the rebound in US equities, longer date UST yields are essentially unchanged to lower. Soft US data releases went unnoticed overnight (see more below).

After threating to break sib 1.13, the euro looks to have stabilised just under 1.14. The rebound in TRY probably helping the cause, but is probably worth highlighting that simmering in the background Italian deputy PMs increased the pressure on the EU over fiscal room for infrastructure spending following the Genoa bridge tragedy. Italy’s fiscal budget battle is a story for September and October and that uncertainty makes it difficult to get too excited on the prospect for the euro to trade back above 1.15 any time soon.

The USD indices are marginally weaker on the day, although both the Bloomberg dollar index and DXY remain close to their highest levels since mid-2017. After lambasting the USD’s strength in recent times, Trump hinted at a more positive attitude to the currency over Twitter, saying “Money is pouring into our cherished DOLLAR like rarely before, companies’ earnings are higher than ever, inflation is low & business optimism is higher than it has ever been.” A weaker than expected Philly Fed survey and slower housing starts data had little impact on the USD or US rates, which were slightly higher on the day (US 10 year Treasury +1bp to 2.87%).

US equities are the outperformers overnight with the Dow Jones adding just under 400 points and the S&P 500 gaining about 0.8% overnight. Walmart jumped ~ 10% after posting the strongest sales in more than a decade prompting the company to raise its full-year outlook. The results boosted food retailers to their best gain since November. European equities also closed mostly higher, after a bad day in Asia mostly weighted down by technology shares.

Rates are sideways to slightly lower – US 10s are around 2.87% and Aussie 10yr futures are at 97.44- 3bp off the year-to-date highs reached yesterday. The Aus-US 10y spread is a touch wider.

Zinc (+4.0%) and Lead (5.86%) led the rebound in commodities with copper up 1.80% and aluminium (1.14%) also having a good night. Oil prices edged up just under 1%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.